Medical Equipment Rental Market: Insights, Key Players, and Growth Analysis

Other |

2026-06-18 06:28:48

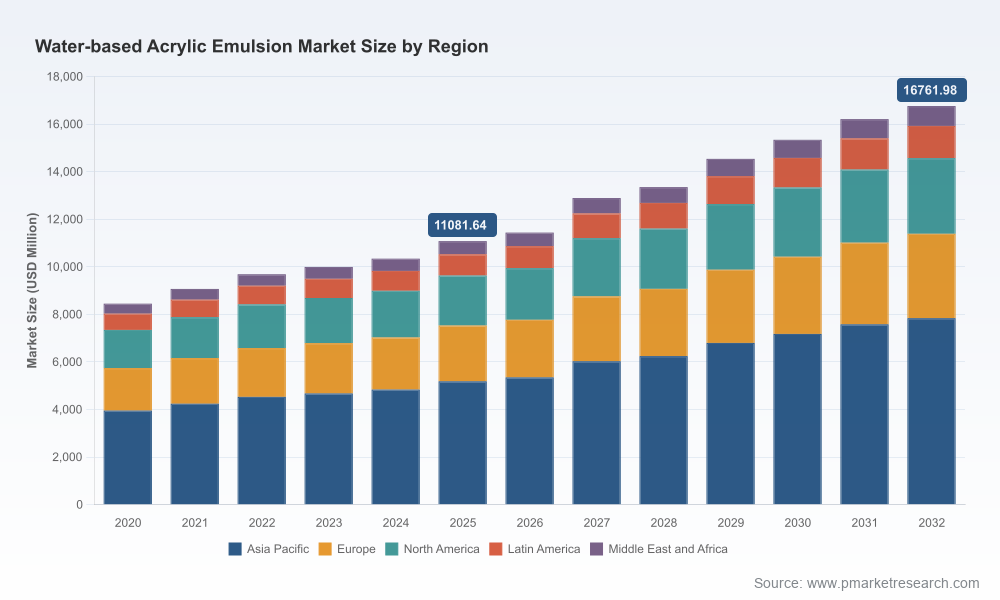

PW Consulting’s new market study on the Water-Based Acrylic Emulsion market frames a near-term action agenda for industrial and specialty chemical leaders making decisions in 2026. The market expanded from an estimated USD 8.45 billion in 2020 to about USD 11.08 billion in 2025; our forecast through 2032 models a steady compound annual growth rate of roughly 6.09%, bringing the market into the mid‑teens of billions by the end of the decade. That macro trajectory masks important inflection points — regulatory tightening, raw-material volatility, and a rapid product shift toward low‑VOC, PFAS‑free and bio‑based grades — which together create both risk and differentiated upside for decisive players.

Water Based Acrylic Emulsion Market

Capital allocation: our report translates market growth and price-sensitivity scenarios into CAPEX sizing options and payback intervals so executives can choose between brownfield debottlenecking, modular brownfield capacity, or targeted greenfield investments.

Water Based Acrylic Emulsion Market

M&A and partnership screening: the study identifies M&A baskets and JV archetypes (technology access, regional footprint, formulation capability) with prioritization criteria calibrated to a 6%+ growth environment.

Water Based Acrylic Emulsion Market

Commercial repositioning: we provide go‑to‑market playbooks for coating formulators, adhesive manufacturers, and paper/board customers to capture premium pricing for low‑VOC and PFAS‑free grades.

Risk management: procurement and hedging options for acrylic acid and co‑monomers are modelled under multiple demand and pricing scenarios so procurement teams can stress‑test supplier contracts in 2026 negotiations.

Comprehensive market sizing and demand forecast (2026–2032) with top‑line and scenario outputs for strategic planning.

Supply‑chain mapping: plant-level footprint analysis, logistics chokepoints, and supplier scorecards to inform sourcing and footprint decisions.

Raw material sensitivity models: acrylic acid price pass‑through, margin impact, and alternative feedstock scenarios (including bio‑derived routes).

Regulatory impact assessment: practical compliance roadmaps for VOC, PFAS/APEO restrictions, and state-level U.S. regimes.

Commercial playbooks and pricing strategies for premium, mid‑market and cost‑focused product tiers.

M&A heatmaps and a prioritized list of technology partners and bolt‑on targets for strategic buyers.

Operational tools: modular capex budgeting templates, KPI dashboards, and time‑to‑market checklists for new grades.

Three dynamics will dominate strategic outcomes in 2026:

Regulation as a demand lever. U.S. federal and key state VOC limits have already accelerated adoption of water‑based, low‑VOC emulsions; regulatory enforcement and labeling requirements continue to push formulators away from solventborne chemistries and toward verified PFAS‑free, APE‑free solutions. Compliance timelines and product validation windows are now central determinants of commercial success.

Raw‑material volatility. Acrylic acid — the primary upstream feedstock — is exhibiting regional price divergence and periodic dislocations. Recent market signals show price increases in select Asian hubs while North America experienced sequential softening in late 2025. These movements make short‑term margin preservation and longer‑term feedstock diversification critical boardroom topics.

Product innovation and differentiation. Buyers increasingly pay for demonstrable sustainability (bio‑based content, low embodied carbon) and functional performance (durability, dirt pickup resistance, adhesion). New chemistries and surfactant innovations are shifting value capture toward formulators who can certify environmental claims and shorten customer qualification cycles.

The market displays moderate concentration: the top three players account for roughly 38% of market volume, while the top five capture a little over half of the market. That structure rewards scale in feedstock sourcing and R&D, but leaves pockets of attractive opportunity for agile specialty players and regional champions.

BASF SE (Ludwigshafen, Germany): broad portfolio and capacity investments in Asia position BASF to lead on regional availability and bio‑based/low‑VOC grades. Strategic implication: BASF’s global scale raises the bar on integrated supply and sustainability claims — competitors should prioritize niche functional performance or faster local qualification as counter‑measures.

Dow Inc. (Midland, Michigan, USA): product innovation (next‑generation low‑VOC emulsions) and North American capacity expansions reflect a bet on construction and automotive recovery. Strategic implication: their move underscores the importance of application‑specific performance and collaboration with OEMs for specification wins.

Arkema SA (Colombes, France): active in low‑carbon formulations and recently announced a partnership to scale bio‑based acrylics. Strategic implication: technology partnerships can accelerate credible low‑carbon product launches, making early access to fermentation or feedstock IP a competitive advantage.

The Lubrizol Corporation (Wickliffe, Ohio, USA): targeted U.S. capacity investment highlights premiumization opportunities in performance emulsions. Strategic implication: specialty performance claims and localized supply can secure faster trials and premium pricing.

Celanese, Synthomer, Mallard Creek Polymers, Gellner, MCTRON, ALV Kimya, Toyochem, Wacker — smaller and mid‑sized players remain influential in regional markets and application niches such as adhesives, paper and textiles. Strategic implication: agile formulators with configurable chemistries can win share by offering custom, fluorosurfactant‑free solutions and faster time to qualification.

Recent industry moves — product launches for reduced‑VOC grades, capacity additions in North America and Asia, and partnerships to develop bio‑based feedstocks — underline that competitive advantage will increasingly be shaped by a combination of performance, sustainability credentials, and supply resilience.

Reformulation roadmap: accelerate 18–24 month programs to convert core product lines to PFAS‑free, APE‑free and low‑VOC formulations, focusing first on high‑value applications with rapid payback (architectural and industrial coatings segments).

Feedstock strategy: develop a two‑track procurement plan — short‑term hedges and contract enhancements with major acrylic acid suppliers, plus medium‑term investments in alternative feedstocks or partnerships for bio‑based monomers.

Selective capacity investments: prioritize modular brownfield debottlenecks and co‑located production near major customers to shorten logistics, reduce carbon intensity and enable faster product qualification.

M&A and partnerships: target bolt‑on acquisitions that provide formulation IP or regional distribution, and pursue JV structures to secure bio‑based feedstock volumes without full upstream integration.

Commercial and pricing playbook: deploy value‑based pricing for verified sustainability credentials and performance benchmarks; align sales incentives with specification wins at key OEMs and coatings formulators.

Data and verification: implement third‑party carbon and chemical safety verification early in product development to remove buyer uncertainty and shorten procurement cycles.

Market penetration of low‑VOC/PFAS‑free grades versus total product mix (monthly cadence).

Effective gross margin by product tier under three acrylic acid price scenarios.

Time‑to‑qualification for new grades in top three customer accounts.

Share of sales from bio‑based claims and certified low‑carbon products (quarterly ramp).

ROIC on incremental capacity and R&D investments (36–60 month horizon).

Our market forecast and strategic recommendations are built from a blended evidence base: primary interviews with manufacturers, formulators and procurement leads; plant‑level production data; proprietary pricing models for key monomers; and regulatory timelines validated against public agency filings. We stress‑tested outcomes across multiple regulatory and feedstock scenarios to provide board‑level confidence for 2026 planning.

This release is a strategic preview designed to inform executive decision making ahead of the full report publication. The comprehensive report includes detailed regional and application segmentation tables, plant‑by‑plant capacity maps, company profiles with recent financial indicators, pricing curves, and downloadable CAPEX and procurement models. These detailed datasets and appendices are intentionally gated to preserve client value; please visit the PW Consulting reports page or contact our advisory desk to download the full Water‑Based Acrylic Emulsion Market report and to schedule a bespoke strategy briefing tailored to your company’s position in the value chain.

— PW Consulting, Strategic Markets & Chemicals Practice

For detailed analysis of this topic, please visit the official page:Water Based Acrylic Emulsion Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com