Healthcare Logistics Product Market Share, Driving Trends, and Industry Forecast by 2033

Other |

2026-07-08 12:28:51

PW Consulting’s new market research preview outlines the strategic contours of the At-Home Hair Removal Devices market as firms prepare decisions for 2026. The market has demonstrated steady expansion through the 2020–2025 base period and enters the 2026–2032 forecast window with robust momentum: global revenues rise from approximately USD 725.5 Million in 2025 and are projected to reach roughly USD 1,180.3 Million by 2032, representing a compound annual growth rate (CAGR) of 7.2% over the forecast horizon. This preview highlights the practical, decision-grade outputs embedded in the full report and summarizes the competitive, regulatory and supply-side dynamics that will shape near-term strategy.

At Home Hair Removal Devices Market

Precision for capital allocation: The report translates market-scale growth into actionable investment priorities — R&D spend benchmarks, go-to-market budgets, and M&A thresholds — calibrated to realistic revenue trajectories through 2032.

At Home Hair Removal Devices Market

Regulatory and clinical risk mitigation: With light-based devices commonly regulated as Class II medical devices requiring U.S. FDA 510(k) clearance, our analysis identifies the evidence generation and submission strategies that meaningfully reduce time-to-market and downside regulatory risk.

At Home Hair Removal Devices Market

Channel optimization: The analysis provides an operational playbook for hybrid distribution models, balancing direct-to-consumer digital strategies with traditional retail and specialty channels to maximize reach and margin.

Competitive positioning: Rather than generalities, the report provides tailored strategic options for market entrants, challenger brands, and incumbent OEMs, derived from granular competitor benchmarking and concentration analysis.

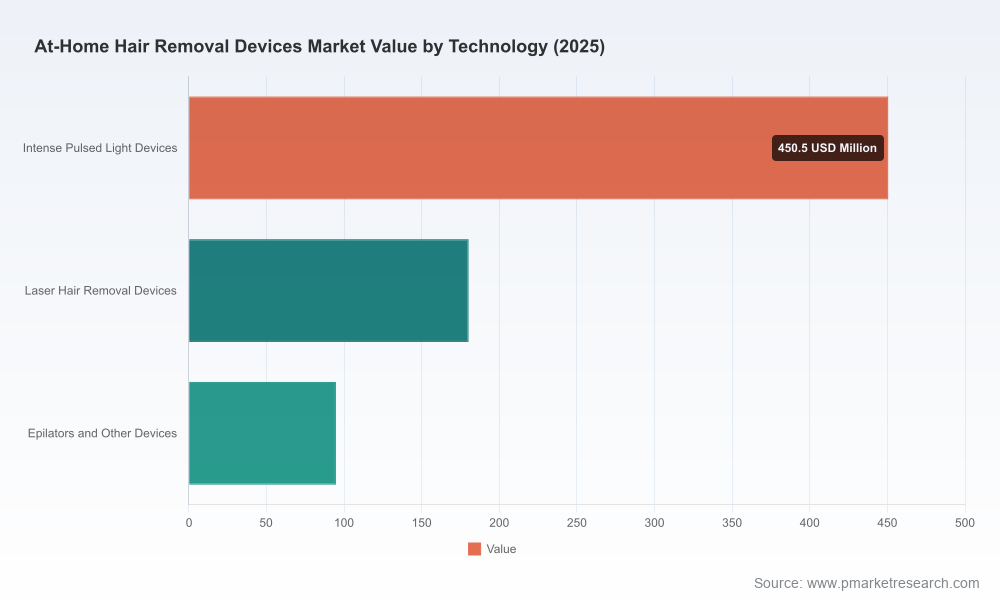

The at-home hair removal category has transitioned from a niche wellness accessory into a scaled consumer device segment. Following several years of steady expansion, the market recorded roughly USD 632–676 million through the early 2020s and reached USD 725.5 Million in 2025. Momentum continues into the forecast period with an expected CAGR of 7.2% to 2032. This trajectory reflects improving technology fidelity (home-safe IPL and diode lasers), accelerating adoption in e-commerce-led channels, and broader consumer willingness to substitute occasional salon sessions with ongoing at-home regimens.

Market concentration is moderate: the top three players account for a meaningful share of industry revenue and the top five approach parity with market-leading segments, reinforcing both the advantages of scale in branding and distribution and persistent opportunities for nimble challengers. (High-level concentration metrics are included in the full report.)

Category leaders emphasize differentiated technology and platformization. Legacy consumer-electronics and personal-care brands prioritize safety features, multi-attachment ergonomics, and brand trust to maintain household penetration.

Specialist brands and smaller innovators pursue clinical-grade claims (higher-powered diode lasers or sustained energy delivery) to target premium segments that value permanence and dermatologist-grade performance.

Regional challengers leverage cost-competitive supply chains and localized R&D to introduce feature-differentiated devices (e.g., advanced cooling systems, skin-adaptive sensors) that lower adoption friction.

Representative competitive profiles (overview):

Philips — Focused on platformized IPL devices with embedded SkinAI and multi-attachment strategies to address face/body use cases while preserving brand familiarity across mature markets.

Braun (Procter & Gamble) — Emphasizes adaptive skin-sensing safety systems to reduce user risk and heighten trust for at-home IPL treatment.

Tria Beauty — Positions through clinical-grade diode laser technology for consumers seeking higher-power, longer-term reduction claims.

Ulike — Pursues differentiated user comfort via active cooling innovations to expand addressable consumer groups sensitive to pain or heat.

SmoothSkin (Cyden Ltd), Remington, Silk’n — Trade on design accessibility, price-performance ratio, and broad channel coverage to defend mass-market volume.

Regulatory posture: At-home IPL and laser devices are widely regulated as Class II medical devices in key markets such as the United States, where 510(k) clearance is typically required for marketing. Recent activity through 2025 includes multiple 510(k) clearances for ice-cooling IPL models by manufacturers based in Asia, and ongoing clearance activity for Class II light-based over-the-counter devices. These trends lower technical entry barriers for compliant entrants that can scale clinical evidence generation.

Reimbursement: Devices are generally considered cosmetic and are not reimbursed by health insurers; however, professional laser treatments may qualify for reimbursement under specific medical indications (e.g., gender-affirming care or certain disease states). Firms should avoid reliance on reimbursement-based demand in their consumer device models unless pursuing clinically indicated use cases supported by payers and CPT guidance.

Implication: A documented clinical strategy — well-designed pivotal studies, robust post-market surveillance, and clear labeling — is now a commercial differentiator, not just a compliance checkbox.

Rising raw-material costs for plastics, metals and electronic components are exerting upward pressure on bill-of-materials and production margins. The full report quantifies sensitivity scenarios to material-cost inflation and explores mitigation levers, including supplier diversification, nearshoring assembly, design-for-cost initiatives, and strategic price-pack architectures that preserve volume while protecting margin.

R&D and product: Prioritize investments in skin-adaptive safety algorithms, pain-minimizing cooling, and power-efficiency improvements for diode laser modules. Embed serviceable design and firmware update paths to extend lifecycles and enable incremental feature monetization.

Regulatory-first commercialization: Treat 510(k)-grade evidence generation as integral to product roadmaps. Consider partnering with clinical research organizations or dermatology centers to accelerate meaningful-use claims and communications.

Channel strategy: Adopt a hybrid go-to-market split that leverages direct-to-consumer e-commerce for rapid customer acquisition and retail partnerships for trust and trial. Specialty medical channels can be used for premium-priced, clinically positioned devices.

Service and retention: Develop subscription models for consumables (e.g., replacement cartridges, cooling accessories) and clinical-adjacent services (tele-dermatology consults) to convert single-unit purchases into higher-LTV relationships.

M&A and partnership criteria: Target acquisitions that deliver complementary technology (laser diodes, sensors), differentiated IP, or immediate access to regulated markets via cleared product portfolios. Given the market’s moderate concentration, strategic bolt-ons can accelerate scale without disproportionate premium multiples.

Top-line market model (2020–2032) with scenario analyses under alternative adoption and pricing cases, and sensitivity to raw-material inflation.

Granular segmentation tables by technology, distribution channel, and region — presented with interactive modeling to test “what-if” strategies. (Note: granular segmentation tables are intentionally not disclosed in this preview.)

Competitive heatmap and capability matrix, including IP position, regulatory status, channel strengths, and recent strategic moves for the key market participants.

Regulatory roadmap and clinical evidence playbook: recommended study designs, endpoints aligned to labeling, and a template 510(k) timeline for accelerated clearances.

Commercial playbooks: 100-day launch plan, a 12-month scaling roadmap, pricing elasticity experiments, and a channel-margin calculator for multi-market rollouts.

Supply-chain resilience toolkit: supplier risk scores, cost-saving design opportunities, and near-term sourcing recommendations to mitigate component shortages and inflation.

Board and investor briefings: Use the macro growth projections and concentration context to justify near-term R&D and channel investments while establishing realistic payback horizons tied to forecast cash flows.

Product committees: Reprioritize roadmaps to include regulatory evidence milestones and post-market safety monitoring that directly map to commercial claims.

Corporate development: Apply the M&A criteria and competitor capability assessment to identify priority targets and potential bolt-on opportunities for rapid scale.

Commercial leadership: Implement the hybrid channel playbook and subscription strategies to increase unit economics and reduce customer-acquisition costs over the forecast cycle.

The at-home hair removal market is maturing into a technology- and regulation-led consumer device category. The pathway to outsize returns in 2026 will be defined by firms that combine clinical rigor and regulatory foresight with digitally native distribution and resilient supply chains. PW Consulting’s full report provides the end-to-end intelligence and executable playbooks necessary to convert the 7.2% CAGR trajectory and market-scale opportunity into concrete, defensible business outcomes.

To access the full dataset, segmentation tables, competitor scorecards and the 100-day/12-month playbooks referenced here, please visit PW Consulting’s At-Home Hair Removal Devices market report page or contact our industry team for a briefing. The preview intentionally limits disclosure of granular regional and application-level splits to encourage direct engagement for subscription clients and decision-makers seeking the complete intelligence set.

For detailed analysis of this topic, please visit the official page:At Home Hair Removal Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com