Plant Genomics Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-07-01 07:40:17

As companies recalibrate supply chains, sustainability targets, and product portfolios for the post-pandemic industrial landscape, the release paper market is emerging from the sidelines into boardroom focus. PW Consulting’s Release Paper Market Report (base year 2025) delivers a forward-looking intelligence package designed to convert market trajectory into executable decisions for 2026 and beyond. This release paper — a preview of our full report — highlights the strategic value executives, procurement leaders, product managers and investors should extract now, while reserving granular segment-level data for the full study available on our site.

Release Paper Market

Timing: 2026 is a hinge year for capital allocation. Companies that finalize sourcing, capacity and circularity investments now will lock in positions through the forecast window. Our market model quantifies the near-term runway and mid-term upside so leadership can prioritize investments with confidence.

Release Paper Market

Regulatory inflection: Extended Producer Responsibility (EPR) and recyclability rules in major jurisdictions are re-shaping product specifications and cost-to-serve. The report translates these regulatory pressures into scenario stress-tests for product redesign and waste-reuse strategies.

Release Paper Market

Cost volatility management: Raw material input dynamics — notably wood pulp price indices and kraft paper spreads — are materially affecting margin structures. The study integrates price-driver analytics to help procurement and finance teams build effective hedging and contract strategies.

Our top-line market model shows a mature, steadily expanding global release paper market. The industry reached an estimated USD 4,850 million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of approximately 5.45% over the 2026–2032 forecast horizon, reaching roughly USD 7,030–7,040 million by 2032 under the base scenario. These aggregate figures reflect a mix of steady end-use demand (labels, tapes, packaging) and pockets of accelerated adoption driven by e-commerce growth and paperization initiatives in packaging.

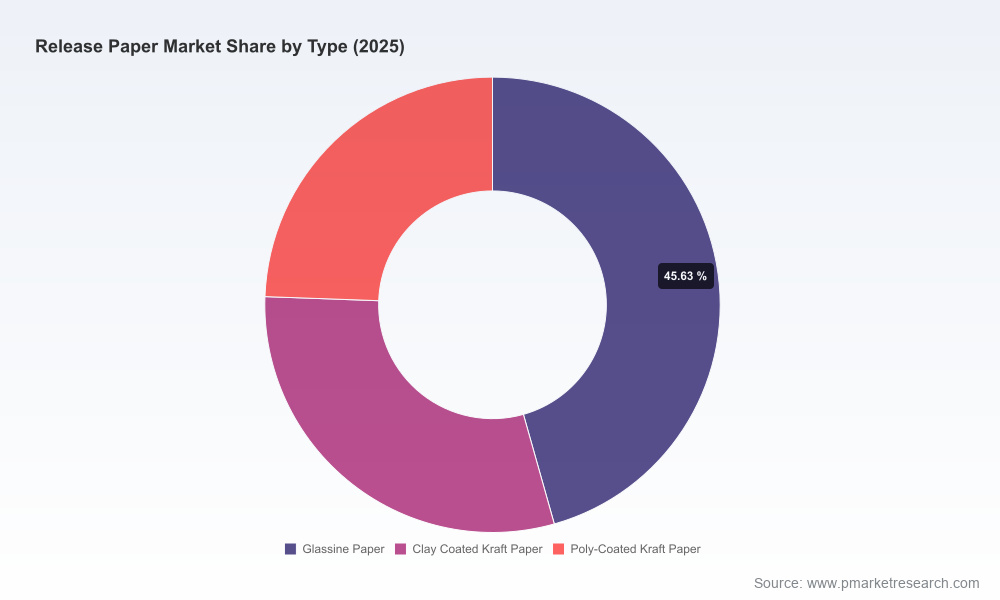

While the headline growth is attractive, the distribution of that growth is heterogeneous: demand drivers, margin profiles and technical requirements vary by substrate (glassine, coated kraft, poly-coated formats) and by application. The full report preserves these granularity layers in proprietary segment models that are deliberately not reproduced in this preview to preserve the consultative value of the dataset.

End-market pull: The primary demand engines remain labels and industrial tapes, followed by packaging migration where barrier coatings and fiber-based solutions are penetrating. Hygiene and medical applications continue to require high-performance liners with traceability and regulatory documentation.

Raw material pressure: Input costs are a persistent headwind. The US Producer Price Index for wood pulp — a useful macro indicator — stood in the high-100s (index value: 197.184 in March 2026), signaling elevated upstream pressure compared with pre-pandemic norms. Kraft paper and film feedstock prices also exhibit regional dispersion, forcing buyers to adopt region-specific sourcing and long-term contracting strategies.

Regulatory and circularity forces: EU EPR rules and regional recyclability guidelines (including several North American state-level initiatives) are driving OEMs and converters to reassess release liner specifications. Recycling pathways for silicone-coated and multi-material liners remain limited; this constraint is propelling collaborative projects to improve reuse rates and establish industrial-scale secondary feedstock chains.

Sustainability is no longer a reporting line item; it is a sourcing and engineering constraint. Innovations in barrier coatings, siliconization processes, and adhesive-release chemistry are enabling the substitution of film-based liners with paper-based alternatives in more segments than before. Leading converters are investing in coatings and deinking technologies to enable closed-loop outcomes. Recent industry initiatives illustrate this trend: collaborative projects focused on siliconized and coated paper waste reuse aim to convert waste streams back into secondary raw materials at industrial scale.

For buyers and product leaders, the strategic decision is binary: plan for incremental improvements to existing supply chains, or commit to transformative investments (coating lines, recycling partnerships, reformulated adhesives). Our scenario analyses quantify the cost curve and time-to-benefit for both approaches.

The market is competitive but not concentrated at the very top. A set of global and regional players compete across substrate innovation, coating capabilities, and route-to-market strength. The full report provides in-depth profiles and capability maps; here we summarize strategic postures of the most influential players and the implications for buyers and investors.

Loparex LLC (USA) — A technical leader in specialty papers and film release liners. Loparex’s direct-coated and poly-coated product stack is differentiated by custom coating capabilities and close cooperation with label converters. For corporate partners, Loparex represents a high-innovation supply option for complex adhesive-release systems.

Ahlstrom (Finland) — Focused on fiber-based and sustainable release base papers. Ahlstrom’s strength is its upstream fiber integration and sustainability branding; it is an attractive strategic supplier for customers accelerating paperization.

Mondi Group (Austria/UK) — Strong on circularity-oriented product development and recently active in capacity expansion. Mondi’s 2026 facility opening in the United States underscores a tactical move to serve eCommerce and industrial packaging demand with locally produced, sustainable paper solutions.

UPM Raflatac / UPM (Finland) — A major provider of release liners and recyclable labelstock. UPM’s roadmap focuses on closed-loop label solutions and recyclable paper-based alternatives, making it a partner of choice for brand owners with aggressive end-of-life targets.

Avery Dennison & 3M (USA) — Both are vertically integrated incumbents with deep customer relationships in labeling and industrial tapes. Their scale and product portfolios provide negotiating leverage but also make them conspicuous early movers on recyclability specifications and adhesive innovations.

Regional and specialty players — Companies such as Gascogne, Sappi, LINTEC, Polyplex, and noted specialty paper manufacturers in Asia and Europe fill important niches: localized supply, specific substrate technologies, and price-competitive filmic options. Several have announced collaborations or showcased sustainable coatings at major trade events, signaling an industry-wide pivot to enable paper-based packaging.

Importantly, the competitive map is dynamic: partnerships between paper producers, coating chemists and recyclers are creating new upstream value chains. Recent public initiatives to recover siliconized and coated paper streams demonstrate the speed of ecosystem formation — and the asymmetric value for first movers that secure downstream offtake commitments.

Procurement and sourcing: Implement dual-track sourcing: secure short-term relief via regional film and coated-kraft suppliers while pursuing long-term contracts with sustainable paper suppliers that can support product redesigns. Use price-driver models to negotiate indexed contracts tied to pulp and kraft benchmarks.

Product and package engineering: Accelerate laboratory-to-pilot validation of paperized liners where feasible. Prioritize trials for products with the highest substitution potential (e.g., certain label formats and internal packaging). Measure total cost of ownership including end-of-life fees under EPR regimes.

Operations and capacity planning: Evaluate modular coating and recycling investments that can be phased. Our scenario modelling provides a prioritized investment timetable — balancing CapEx intensity against regulatory timelines and supply risk.

Partnerships and M&A: Consider bolt-on acquisitions of regional specialty papermakers or minority investments in recycling ventures to secure secondary feedstock. Strategic JV models with coating chemists and converters can quickly unlock closed-loop supply chains without full vertical integration.

Commercial go-to-market: For brand owners, embed liner recyclability and supply chain traceability into procurement scorecards. For suppliers, develop certified recycled-content product tiers and transparent LCA claims to accelerate adoption by sustainability-driven buyers.

The full report is structured to be actionable for deployment in 90–180 day decision cycles and includes:

A validated market sizing model and forecast (2026–2032) with scenario sensitivity.

Detailed segmentation by substrate, application and geography (note: proprietary segmentation tables are available in the full report).

Supply chain maps, margin waterfall models, and a raw-material cost simulator tied to pulp and kraft indices.

Regulatory impact assessment (EPR, recyclability guidance) and a compliance roadmap.

Company profiles and competitor capability matrices, including strategic positioning, technology stacks, and partnership pipelines.

Practical implementation playbooks: procurement templates, pilot design checklists, KPI dashboards and M&A screening filters.

Executive briefings and slide decks tailored for investor relations, board-level strategy reviews, and operations teams.

This preview is designed to prompt three immediate actions for executives finalizing 2026 plans:

Run a rapid sensitivity test for your product lines against a +200–300 basis point swing in pulp-related input costs. If your margins are vulnerable, prioritize contract renegotiations or relocation of production footprints.

Map your top 5 SKUs by recyclability risk and initiate supplier dialogues for paperized alternatives or recycling partnerships; our full report provides SKU-level triage templates to accelerate this work.

Engage with at least one potential partner from the compact set of specialty suppliers and recyclers identified in this preview to explore pilot trials. First movers can secure preferential supply terms and joint marketing opportunities.

The release paper market sits at an inflection: incremental growth continues, but the next phase of value accrual will be captured by players who can convert regulatory pressure and sustainability imperatives into economically viable supply chain architectures. PW Consulting’s Release Paper Market Report equips decision-makers with the models, scenarios and implementation tools to convert market intelligence into actions in 2026. The preview above signals the areas of highest strategic leverage; the full report contains the proprietary segment and company-level data needed to operationalize these insights.

For access to the complete dataset, detailed segment models, and the company capability matrices referenced here, please consult the full Release Paper Market Report on the PW Consulting publications page — your roadmap to making 2026 the year your organization turns release liner risk into competitive advantage.

For detailed analysis of this topic, please visit the official page:Release Paper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com