Palm Kernel Shells Biomass Market: Strategic Imperatives for Corporate Decision‑Making in 2026

Executive preview

As energy transition agendas accelerate across Asia and export markets in East Asia and beyond, Palm Kernel Shells (PKS) are moving from a niche by‑product to a strategic biomass commodity. PW Consulting’s latest Palm Kernel Shells Biomass Market report (base year 2025) captures that shift with a data‑driven forecast and actionable playbooks for executives planning capital, procurement, or sustainability decisions in 2026.

Palm Kernel Shells Biomass Market

Market snapshot — growth trajectory you cannot ignore

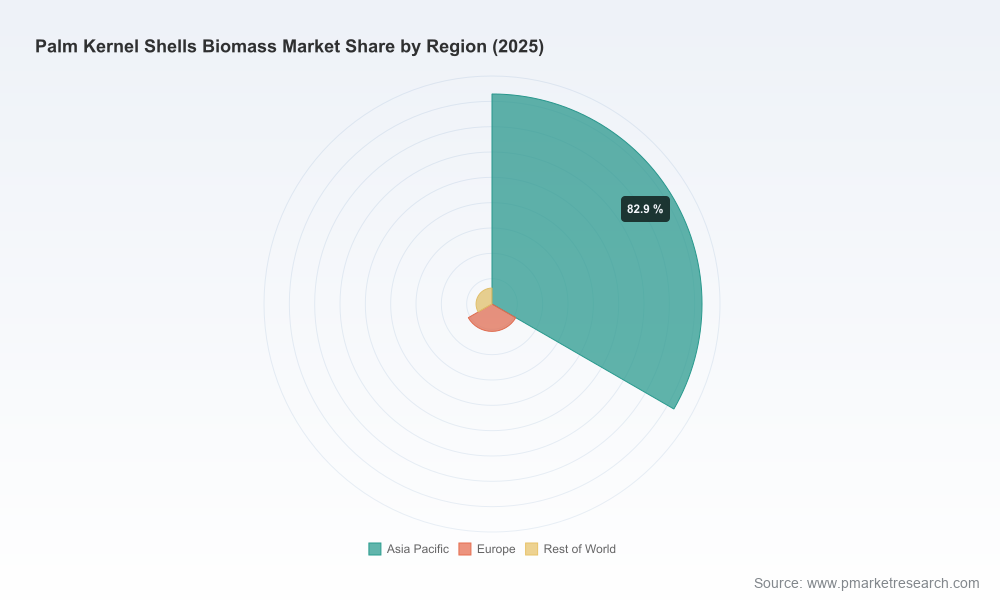

The global PKS market has more than doubled in the past half‑decade, rising from the low hundreds of millions (USD Million) in 2020 to an estimated market size of approximately 1,310.0 (USD Million) in 2025. Our forecast through 2032 projects continued robust expansion to roughly 2,318.9 (USD Million), implying a compounded annual growth rate (CAGR) of 8.5% over the forecast horizon. This trajectory reflects rising demand for high‑density biomass in power generation, industrial boilers and co‑firing applications, combined with increasing buyers’ emphasis on certified, traceable feedstock.

Palm Kernel Shells Biomass Market

Market structure is neither atomized nor tightly consolidated: the three‑firm concentration ratio sits at about 32.4%, while the top five account for roughly 45.8%. That profile creates strategic windows for mid‑sized traders and integrated producers to scale via capacity investments, long‑term offtake agreements, or specialized services (e.g., GGL certification support, logistics bundling).

Palm Kernel Shells Biomass Market

Why this report matters for 2026 decisions

- Timing of investment and offtake: With demonstrated CAGR and predictable seasonality tied to palm oil cycles, 2026 is a critical point for locking pricing and capacity—either by securing long‑term supply or by hedging procurement strategies to manage export levy cycles and quality premiums.

- Sustainability compliance: GGL and similar sustainability credentials are now gating exports to key markets. The report details compliance pathways and the commercial premiums associated with certified PKS — essential for buyers and processors negotiating contracts in 2026.

- Operational due diligence: Logistics, calorific performance (typically 15–16 GJ/MT), moisture management and ash behavior materially affect boiler performance and whole‑asset economics. Our operational checklists and supplier scorecards reduce technology and contracting risk.

- Regulatory sensitivity: Export taxes, levies and service tariffs in producing countries directly influence landed cost models. The report maps recent policy moves and models their short‑ and medium‑term pricing impacts across the supply chain—critical intelligence for CFOs and trading desks.

Report deliverables — practical, executable content

Rather than theory, the report is structured to be used at the deal table. Key deliverables include:

- Consolidated market sizing and scenario forecasts (2026–2032) with upside/downside sensitivity to feedstock availability, export policy shifts, and major demand drivers.

- Buyer playbooks for power utilities, independent power producers (IPPs), and industrial steam users covering contract structures, quality specifications, and logistics optimization.

- Supplier playbooks for processors and mill operators focused on capacity sequencing, certification pathways (e.g., GGL), and export readiness.

- Commercial dashboards — anonymized company comparators, pricing indices, and freight elasticity tools that allow users to simulate landed cost outcomes under different tax/levy regimes and route choices.

- Risk registers and mitigation matrices covering regulatory, operational, and reputational vectors (including GGL compliance monitoring and chain‑of‑custody verification).

- An actionable M&A and JV checklist for investors evaluating expansion in processing capacity, cross‑border logistics assets, or downstream pelletization and briquetting facilities.

Competitive landscape — who to watch and what their moves imply

Our industry mapping combines public filings, site visits and proprietary interviews to profile the supply chain’s most active players. A few strategic takeaways:

- Integrated regional producers with processing footprints and sustainability certification are establishing durable commercial advantages. Their ability to offer certified, export‑grade PKS at scale shortens buyers’ procurement cycles and reduces due diligence friction.

- Trading houses and Japanese buyers continue to play a pivotal role in demand aggregation and quality assurance, because they maintain long‑term relationships with certified mills and coordinate multi‑port dispatch strategies.

- European and Southeast Asian suppliers focused on quality consistency (sizing, low ash) are adapting product lines to support co‑firing and activated carbon feedstock markets—broadening demand beyond traditional steam and power segments.

Company highlights (select)

- BIO ENECO Sdn Bhd (Elridge Energy Holdings Bhd subsidiary) — Malaysian processor and exporter that has emphasized GGL certification and multiple processing sites. Recent capacity expansion and multi‑year supply arrangements underscore an aggressive push to capture certified export flows into Japan and regional markets. (See: https://bioeneco.com/)

- Iwatani Corporation — A long‑standing Japanese buyer and supplier aggregator that sources PKS from Indonesia and Malaysia and offers flexible delivery from multiple Southeast Asian ports; their presence highlights the importance of buyer‑led logistics solutions. (See: https://www.iwatani.co.jp/eng/business/material/resources-advanced/products/pks/)

- NISSIN BIO ENERGY SDN. BHD. — Focused on stable, quality supply from Malaysia; positions itself as a reliable partner for industrial users seeking consistent energy feedstock. (See: https://nissin-bio-energy.com.my/)

- PT Dharma Satya Nusantara Tbk (DSNG) — An Indonesian mill operator supplying certified PKS with integrated offtake pathways; recent activity signals mill‑level producers will continue to capture margin by upstream integration. (See: https://dsn.co.id/)

- CM Biomass — European supplier emphasizing technical specifications (low ash, consistent size, calorific performance) for industrial boiler and activated carbon markets; illustrates demand diversification for PKS beyond power generation. (See: https://www.cmbiomass.com/products/palm-kernel-shells/)

- Other active players — A number of regional specialists and trading houses are expanding services across Southeast Asia to provide end‑to‑end logistics, certification support, and tailored product grades for co‑firing and pelletized applications.

Recent developments that will shape 2026 commercial strategy

- Major capacity additions and long‑term MOUs by certified processors have tightened the market for export‑grade PKS and shifted leverage toward certified suppliers in short contract cycles.

- Awarding of sustainability‑linked recognition for co‑firing projects signals growing acceptance of PKS in large power systems, supporting demand stability for compliant product streams.

- Producer country policy moves — including export taxes/levies and adjusted export service tariffs — are increasingly used as instruments to modulate exports and domestic supply. These policy levers have immediate implications for landed cost modeling and sourcing strategies.

Regulatory and raw material dynamics — what to monitor

PKS procurement economics are a function of three interlinked vectors: raw material availability at mills, certification and traceability costs, and export‑related fiscal measures. Typical PKS technical specifications (net calorific value and ash content ranges) are reasonably consistent across suppliers, but quality management (moisture control, sizing) materially affects combustion efficiency and logistics density. On the policy front, producers’ export tax regimes and service tariffs are dynamic and should be treated as variables, not constants, in any 2026 procurement model.

Strategic playbook — recommended actions for 2026

- Buyers (utilities, industrials): Prioritize bilateral contracts with certified suppliers or pooled offtake through trusted aggregators to secure quantity and quality. Embed GGL compliance clauses, acceptance testing protocols, and freight pass‑through tolerances.

- Processors and mill owners: Fast‑track certification where feasible and consider staged capacity expansions tied to secured offtake to preserve working capital. Explore value‑addition (pelletization, briquetting, charcoal feedstock) to capture downstream margins.

- Traders and logistics providers: Differentiate via bundled services—certification handling, port scheduling, moisture control and last‑mile delivery—to reduce buyers’ transaction costs and increase stickiness.

- Investors and M&A teams: Target assets that combine processing scale with export compliance and port access. Mid‑market consolidation or strategic partnerships with certified processors will accelerate market share gains without the time and cost drag of greenfield certification.

Methodology, confidence and next steps

PW Consulting’s market model uses historical data (2020–2025), proprietary shipment and price indices, site‑level capacity surveys and supply‑chain interviews to produce scenario forecasts for 2026–2032. Our confidence intervals reflect sensitivity to export policy shifts and major capacity additions; we provide scenario stress‑tests in the full report so decision‑makers can quantify downside exposure and upside capture strategies.

Closing — the intelligence edge for 2026

For executives planning capital allocation, securing reliable feedstock, or negotiating long‑term offtake, 2026 is a pivotal year. The PKS market’s robust CAGR and clear movements toward certified supply chains create both opportunities and execution risks. PW Consulting’s Palm Kernel Shells Biomass Market report translates those dynamics into transaction‑ready recommendations, supplier scorecards, pricing tools and risk matrices.

Access the full analysis, anonymized company dashboards, and the operational playbooks referenced in this preview at our report page. The preview above showcases the depth of the research while reserving the granular segment and company‑level datasets to the full report—designed specifically to support decisive action in 2026.

For detailed analysis of this topic, please visit the official page:Palm Kernel Shells Biomass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com