IoT Security Solutions for Unified Threat Management (UTM) Market — Strategic Outlook for Enterprise Decision‑Makers (2026)

As connected devices proliferate across manufacturing floors, hospitals, smart buildings and distributed retail networks, the convergence of IoT security requirements with unified threat management (UTM) capabilities has moved from an IT architecture preference to a board‑level strategic imperative. PW Consulting’s new market research brief, "IoT Security Solution For Unified Threat Management (UTM) Market," delivers a concise, action‑oriented intelligence package tailored for C‑suite and security leaders who must make capital allocation, vendor selection and risk‑transfer decisions in 2026 and beyond.

Iot Security Solution For Unified Threat Management Utm Market

Executive snapshot — why this matters now

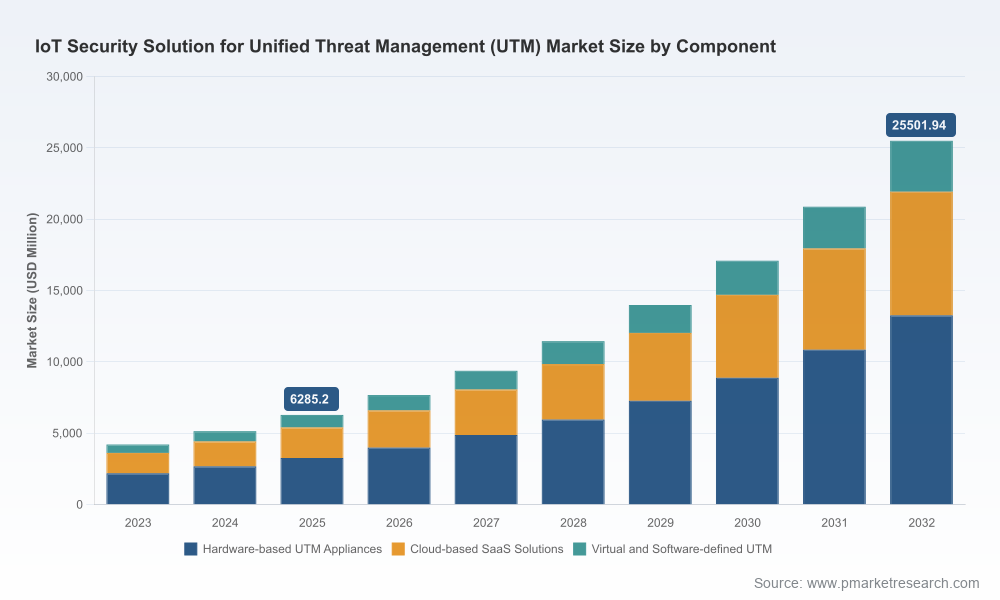

Between 2020 and 2025, enterprises accelerated IoT deployments to enable operational resilience and new business models. Our market model shows that the consolidated UTM market addressing IoT security reached USD 6,285.2 Million in the base year 2025 and is projected to expand at a compound annual growth rate (CAGR) of 22.15% over the coming forecast window (2026–2032). By 2032, the sector is forecast to exceed USD 25.5 billion (USD Million units), driven by combination of regulatory pressure, the need for device visibility/segmentation and the shift toward hybrid network architectures.

Iot Security Solution For Unified Threat Management Utm Market

What this report gives enterprise leaders in 2026

- Decision‑ready market context to prioritize investments across on‑premises appliances, cloud‑delivered services and software‑defined UTM deployments without getting lost in vendor marketing.

- Prescriptive vendor selection criteria and risk scoring tailored to IoT use cases — from time‑sensitive industrial control systems to consumer‑grade edge devices in retail environments.

- Integration and operating playbooks that translate security strategy into procurement specs, implementation phases and managed‑service partnership models.

Data‑driven trajectory — a market in rapid expansion

The macro picture is unambiguous: the combined demand for UTM capabilities that explicitly address IoT device discovery, segmentation and lifecycle protection is accelerating. Our point estimates show a clear upward trajectory year‑over‑year—illustrating not only demand growth but also the pace of vendor innovation and service model evolution that buyers must account for. This expansion is a strategic opportunity for enterprises to renegotiate terms with incumbents, explore co‑managed models with MSPs, and prioritize architectures that enable continuous device hygiene and policy enforcement.

Iot Security Solution For Unified Threat Management Utm Market

Key growth drivers and structural risks

- Regulatory enforcement and liability: EU‑level legislation that holds device manufacturers accountable for lifecycle security, and other cross‑border data rules, are forcing manufacturers and integrators to bake security into device and network design. Enterprises must factor compliance burdens and potential supply‑chain remediation costs into procurement timelines.

- Hybrid architecture adoption: The migration toward mixed deployments—hardware UTM appliances at the edge, cloud‑native controls for distributed sites, and virtualized UTM instances in private/public clouds—creates architectural complexity that amplifies integration risk if not planned with a consistent policy plane.

- Vendor consolidation and platform breadth: Market concentration measures indicate that a relatively small set of established vendors controls a meaningful share of industry revenue, but innovation from cloud and software‑centric players is expanding competitive dynamics. Buyers should evaluate both breadth of feature integration and the vendor’s ability to operationalize IoT‑specific controls at scale.

- Infrastructure cost pressures: Rising costs in data center construction and cross‑border data handling rules are changing the cost calculus for centralized vs. edge‑local processing of IoT telemetry and security analytics.

Competitive landscape — how to interpret vendor signals

The report profiles leading vendors that are shaping the UTM + IoT security agenda. Each profile includes strategic positioning, go‑to‑market motions, technology differentiators and pragmatic questions procurement teams should ask during RFPs. Among the firms covered are globally recognized network security vendors that have integrated IoT‑focused features into their UTM portfolios, and newer entrants emphasizing cloud, AI and managed service economies of scale.

- Fortinet, Inc. (Sunnyvale, CA) — recognized for integrated NGFW platforms with UTM capabilities that emphasize segmentation and real‑time device visibility.

- Cisco Systems, Inc. (San Jose, CA) — combines Secure Firewall and cloud‑managed appliances with device profiling and threat intelligence orchestration for large, distributed estates.

- Check Point Software Technologies Ltd. (Tel Aviv) — focuses on policy enforcement and prevention across hybrid deployments, with a cloud security angle for IoT ecosystems.

- Sophos Ltd. (Abingdon, UK) — offers unified firewalls with dedicated IoT management features and regular platform updates to close operational vulnerabilities.

- WatchGuard Technologies, Inc. (Seattle, WA) and SonicWall Inc. (Milpitas, CA) — both provide appliance and virtualized options designed for SME and MSP channels, with increasing emphasis on co‑managed services.

- Barracuda Networks, Inc., Juniper Networks, Inc., Huawei Technologies Co. Ltd., and Palo Alto Networks, Inc. — each brings distinct tradeoffs between appliance capability, cloud orchestration and AI‑driven detection for IoT scenarios.

Recent product and platform activity through 2026 demonstrates vendor strategies: product refreshes to embed Zero Trust Network Access (ZTNA), SASE integrations, and modular co‑managed offerings aimed at MSP channels. These moves are not mere feature churn — they change commercial relationships and operating models for enterprise buyers. Procurement teams should treat such launches as triggers to revisit contractual SLAs, incident response commitments and cyber‑warranty propositions.

Regulatory and operational context that shifts strategic priorities

- New liability and data access rules require visibility into device data flows and the ability to demonstrate lifecycle patching and vulnerability management for connected devices.

- Cross‑border data controls and bulk data transaction rules introduce new vendor due‑diligence obligations and may limit where certain analytics or forensic processes can run.

- Rising capital and operating costs for data center and edge infrastructure further tip the balance in favor of architectures that optimize for latency, compliance and total cost of ownership (TCO).

How enterprises should act in 2026 — recommended strategic moves

- Shift from point‑product procurement to policy‑centric architecture. Specify outcome‑based SLAs (device discovery rate, segmentation enforcement time, mean‑time‑to‑isolate) rather than only appliance throughput or rule counts.

- Adopt hybrid procurement: blend appliance investments where latency or air‑gapped control matters with cloud‑delivered UTM services for remote sites and fractal growth areas.

- Insist on auditable device lifecycle processes. Suppliers must demonstrate patch pipeline governance, vulnerability disclosure tracking and contractual commitments aligned with device manufacturer liability regimes.

- Rationalize vendor portfolios with a two‑track approach: maintain strategic relationships with incumbent providers for critical environments and run targeted proofs‑of‑concept with cloud/SaaS innovators to test operational resilience and cost elasticity.

- Embed M&A and partner scouting into security roadmaps. The market’s concentration profile shows room for acquisitive activity and strategic alliances that can accelerate IoT‑specific feature delivery for enterprises that need faster time‑to‑compliance.

What the full PW Consulting report contains (practical deliverables)

Designed as an implementation playbook rather than a purely academic study, the full report includes:

- A detailed market model (historical 2020–2025 and forecast 2026–2032) with scenario analyses and sensitivity testing calibrated for alternative adoption curves.

- Vendor scorecards and vendor‑fit maps that translate product capability into procurement language: architectural fit, channel model, managed service availability, and operational maturity.

- Regulatory impact matrix and compliance checklists keyed to major jurisdictions and lifecycle obligations that affect IoT device manufacturers and enterprises.

- Three technical deployment blueprints (industrial control, clinical device networks, distributed retail/branch environments) with phased implementation plans and measurable KPIs.

- TCO and ROI frameworks that capture not only CapEx and OpEx, but also expected reduction in incident exposure and insurance premium impacts.

- M&A heatmaps, partner ecosystem guides and an MSP selection rubric for organizations considering co‑management or outsourcing models.

- Templates and RFP language to accelerate procurement cycles and shorten vendor evaluation timelines.

Note: in keeping with our "trailer" approach for this public release, we present the strategic implications and deliverable descriptions above while intentionally withholding granular tables and dollar‑by‑dollar segmentation extracts. The full dataset, including interactive models and vendor benchmarks, is available through PW Consulting’s report portal.

How to use this insight in boardroom decision cycles

- Short term (0–6 months): use the report’s procurement templates and compliance matrix to harden immediate exposure points and to negotiate service terms that reflect IoT lifecycle risk.

- Medium term (6–18 months): run pilot architectures that marry appliance‑level enforcement for critical zones with cloud orchestration for scale; rebaseline budgets using the report’s TCO scenarios.

- Long term (18–36 months): align security strategy with business transformation plans—ensure that future plant/clinic rollouts include contractual security deliverables from device OEMs and channel partners.

Concluding recommendation

The intersection of IoT and UTM is no longer an edge concern. With a robust growth trajectory and market dynamics shaped by regulation, vendor consolidation and infrastructure cost pressures, enterprises that proactively realign their procurement and architecture strategies will gain both risk reduction and competitive agility. PW Consulting’s market brief provides the practical instruments and strategic framing teams need to make those choices with confidence in 2026.

Access the full intelligence package

For the complete dataset, interactive models, vendor scorecards and implementation assets referenced in this summary, visit the PW Consulting insights portal to request full access to the "IoT Security Solution For Unified Threat Management (UTM) Market" report and supporting toolkits.

For detailed analysis of this topic, please visit the official page:Iot Security Solution For Unified Threat Management Utm Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com