Price of under-eye filler injections in Saudi Arabia

Health |

2026-06-05 12:06:50

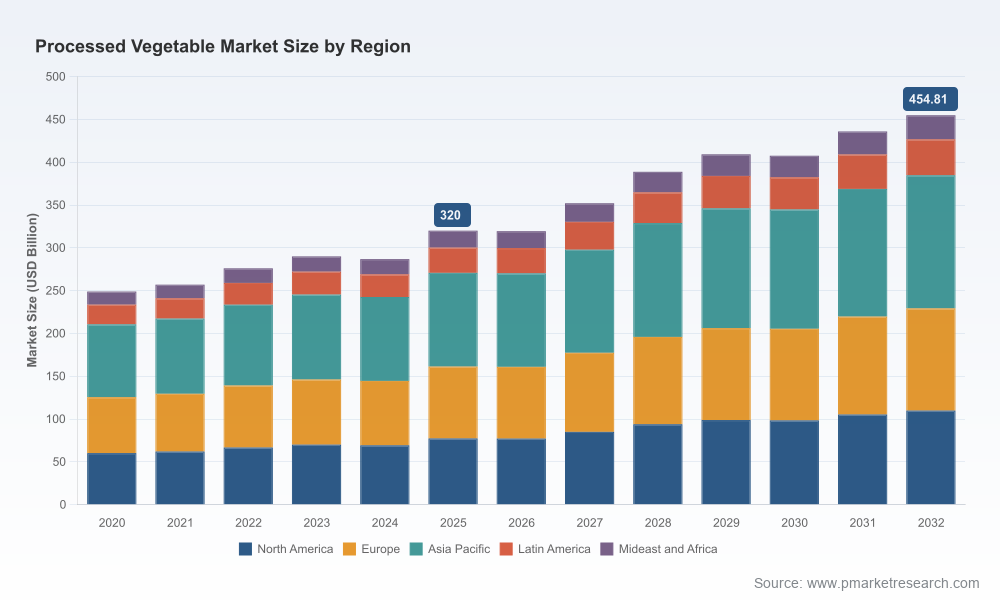

The global processed vegetable market reached an estimated USD 320.0 Billion in the base year 2025. Our forward-looking model—built on a blended bottom-up and top-down approach with scenario stress-tests—projects a compound annual growth rate (CAGR) of 5.15% across the 2026–2032 forecast window. After a modest near-term correction in 2026, the market resumes a steady expansion trajectory through 2032 driven by a mix of demand rebalancing, channel substitution, and productivity-led supply responses.

Processed Vegetable Market

This preview highlights the strategic implications of our findings for executive teams and investors preparing plans in 2026. It intentionally previews high-level conclusions and operational takeaways while withholding the full regional, application and pricing tables that form the core dataset of the full PW Consulting report—those proprietary subsegment tables and supplier-level metrics are available on the report page.

Processed Vegetable Market

Planning horizon alignment: 2026 is a pivotal planning year for many CPG and ingredient businesses recalibrating supply chains post-pandemic and post-2024–25 commodity shocks. Our report provides the macro envelope (market size, CAGR, concentration metrics) you need to align FY-26 budgets and three-year strategic initiatives with realistic demand curves.

Processed Vegetable Market

Risk quantification: The market’s moderate fragmentation—with the top-three players controlling under one-fifth of market value and the top-five below one-quarter—creates both opportunity and supplier risk that must be explicitly managed in sourcing and M&A strategies.

Operational levers: The interplay between raw-material inflation, regulatory pressure and episodic recalls makes operational excellence (quality, traceability, agile sourcing) a core value driver in 2026. Our operational playbooks show where to invest to protect margins and brand trust.

Input-cost pressure and price dynamics — USDA forecasts indicate upward pressure on fresh vegetable pricing in 2026, with notable increases both at retail and farm levels. These dynamics compress margins for processors that cannot rapidly pass cost through, and they create incentive for vertical integration, hedging strategies, and dynamic contract renegotiation.

Food-safety and regulatory volatility — The sector experienced a notable number of official recalls in 2025, and ongoing state-level initiatives targeting additives create compliance cost uncertainty. For 2026, companies must treat regulatory monitoring and rapid-response recall playbooks as board-level priorities.

Trade and tariff noise — Geopolitical and trade actions in 2025, including retaliatory measures between key North American partners, have altered cross-border supply flows for preserved vegetable lines. Firms with flexible cross-border processing footprints will have a competitive edge in mitigating short-term trade shocks.

Channel mix shift — Retail resilience continues alongside selective recovery in foodservice. Processors that can optimize SKUs across channels and offer ready-to-cook/ready-to-heat formats will capture higher-margin pockets as consumer convenience appetite persists.

The processed vegetable sector remains consolidated at the top yet broadly fragmented across the long tail of regional and private-label players. Leading multinationals and established processors continue to pursue a mix of organic expansion and targeted M&A to secure raw material access, fill portfolio gaps, and scale processing capacity.

Dole plc and Fresh Del Monte-related moves: Global players with integrated supply chains retain advantages in raw-material sourcing and year-round capacity scheduling. The acquisition activity observed in early 2026 shows the strategic logic of acquiring packaged vegetable assets to capture shelf-ready categories and shorten go-to-market cycles.

Branded frozen/canned specialists: Firms such as Conagra, Greenyard, and Bonduelle sustain market share via strong retail and foodservice relationships; their strategic focus is on SKU rationalization, premiumization of frozen ranges, and sustainability-linked sourcing programs.

Regional champions and category specialists: Producers like Ardo, Seneca Foods, J.R. Simplot and others are competing on service levels, co-manufacturing capabilities and private-label scale. Their agility in harvest-to-processing windows is a key differentiator for industrial and foodservice customers.

Private capital and distressed opportunities: The 2025 bankruptcy of a legacy canned-vegetable incumbent and subsequent asset divestitures created buying opportunities for strategically minded acquirers. Expect continued portfolio reconfiguration through 2026 as buyers pursue scale, geographic fill-ins and margin improvement synergies.

The PW Consulting full report is structured to be directly actionable for strategy, commercial, and operations teams. Highlights include:

Proprietary market model and sensitives — interactive demand-supply scenarios across the 2026–2032 horizon with price and volume sensitivities tied to raw-material, regulatory and channel scenarios.

Competitive playbooks — company-level profiles, capability maps and M&A heatmaps that identify likely acquirers, divestiture targets and partnership candidates.

Commercial toolkits — SKU rationalization frameworks, margin-scenario templates, and route-to-retailer negotiation tactics designed to protect EBIT in inflationary periods.

Sourcing & operations diagnostics — harvest-to-plant calendars, supplier-criticality matrices and recommended investments in traceability and cold-chain automation.

Risk register and regulatory tracker — prioritized recall and compliance scenarios with recommended governance and crisis-playbook templates for 2026 readiness.

Note: this preview omits the full breakouts by region, application and SKU-level pricing tables that constitute the core proprietary dataset. Those subsegment tables and supplier-by-plant metrics are accessible in the full report on the PW Consulting report page.

Re-risk your raw-material pipeline now: implement dual-sourcing and short-term forward contracts for critical vegetables where farm-level price volatility is highest. Tie a portion of purchasing to indexed contracts to limit margin erosion.

Accelerate traceability investments: allocate capital to end-to-end traceability and rapid-testing capabilities; this reduces recall costs, insurance premiums and protects brand equity.

Pursue bolt-on acquisitions that close capability gaps: prioritize targets that provide processing capacity in undersupplied geographies or add high-margin convenience formats that play well in retail and foodservice.

Rationalize SKUs across channels: reduce low-velocity SKUs and reallocate real estate to premium frozen and convenience offerings that command higher margins and retailer support.

Embed regulatory scenario planning in commercial contracts: include clauses that fairly share compliance-cost shocks and create rapid price-adjustment mechanisms tied to verified input-cost indices.

Design a recall rapid-response playbook: cross-functional rehearsals and supplier-cascading protocols cut time-to-isolation and materially reduce downstream costs and reputation damage.

For boards and executive teams, the report is designed to support three immediate actions in Q1–Q2 2026:

Validate or reset FY-26 revenue and margin targets using the report’s baseline and downside scenarios.

Prioritize a short list of operational investments and M&A targets with 12–18 month payback under the conservative scenario.

Stand up a regulation-and-recall risk cell that uses our monitoring dashboard to trigger contract and capex contingencies.

The processed vegetable market in 2026 is neither a simple growth story nor a pure restructuring narrative; it is a market of selective winners. Firms that combine supply-side resilience, channel agility and disciplined capital deployment will outpace the broader market. PW Consulting’s full report supplies the quantitative subsegment data, supplier scorecards and scenario-ready playbooks you need to convert these strategic themes into operational plans.

To obtain the full dataset, regional and application breakouts, and the complete set of tools and templates referenced in this preview, please visit the PW Consulting report page for the Processed Vegetable Market. Our team is available to brief leadership teams and to tailor the analysis to your portfolio and geographic footprint.

For detailed analysis of this topic, please visit the official page:Processed Vegetable Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com