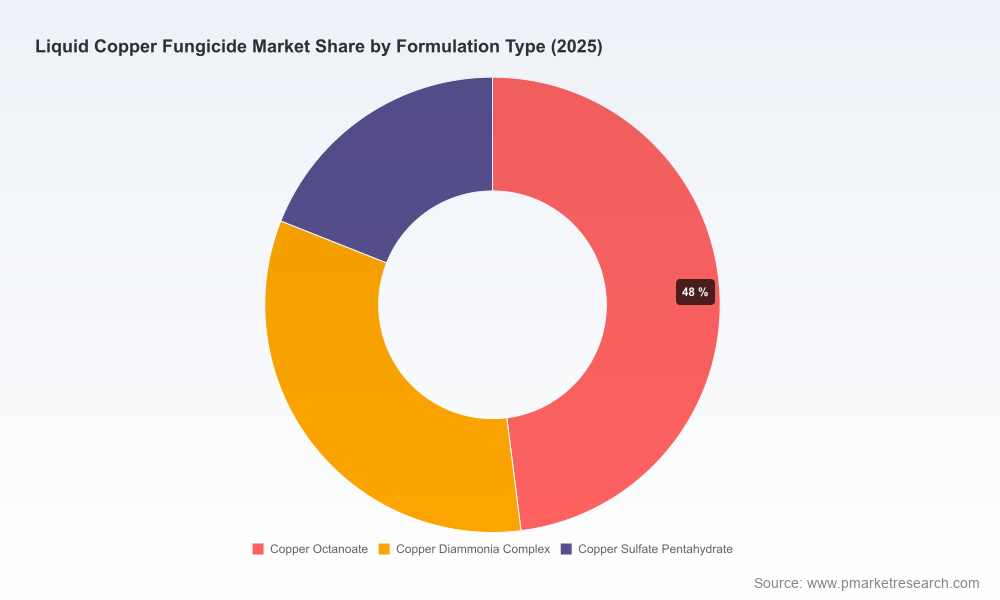

Liquid Copper Fungicide Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Consultant and Chief Industry Analyst, I present a focused preview of our new market research on the Liquid Copper Fungicide market. This briefing synthesizes the macro trends, competitive dynamics, regulatory inflection points, and practical decision frameworks that will matter to executive teams planning actions in 2026. It showcases the analytical depth of the full study while deliberately preserving granular segment tables and proprietary model outputs to encourage direct access to the report.

Liquid Copper Fungicide Market

Why this market matters in 2026

Liquid copper fungicides occupy a unique intersection of agronomy, regulation, and commodity dynamics. After steady recovery and adoption through the early 2020s, the market is on a clear, predictable growth trajectory. Our baseline model—anchored to a 2025 base year—projects a compound annual growth rate (CAGR) of 4.82% over the forecast window, with total market revenues expanding year-on-year under current policy and supply assumptions. This steady growth masks important volatility drivers that will determine who wins and who is exposed in 2026 and beyond.

Liquid Copper Fungicide Market

What the full report delivers (practical, operational content)

- Proprietary demand model calibrated to 2020–2025 historicals and stress-tested across regulatory, price, and adoption scenarios for 2026–2032.

- Scenario-based pricing and margin impact tool that quantifies the P&L effects of raw material shocks, tariff regimes, and EU/ANSES-style use restrictions.

- Supply-chain risk matrix mapping supplier concentration, substitutability of copper salts, and lead-time sensitivities by formulation and geography.

- Regulatory playbook with compliance checklists, labeling adaptations, and worker-safety protocols to meet tighter authorization conditions.

- Commercial go-to-market frameworks for both bulk agricultural channels and retail/home-garden segments, with tactical pricing and bundling recommendations.

- M&A and partnership screening criteria that identify high-impact targets (distribution assets, formulators, niche brands) based on synergies and integration payback timelines.

- Product-portfolio optimisation templates to prioritize formulation investments (liquid vs suspension, novel copper complexes) under environmental-use constraints.

These modules are built to be deployed immediately by strategy, commercial, and procurement teams. The report includes ready-to-use slides and model shells so teams can adapt analysis to internal ERP and financial systems without rebuilding the wheel.

Liquid Copper Fungicide Market

Macro dynamics shaping 2026 strategy

- Commodity price and tariff risk: Refiners and formulators face heightened input-cost uncertainty. Recent market intelligence shows notable upward pressure on copper feedstock prices, and proposed tariff measures in some importing countries materially increase the cost envelope for formulated liquid products. Procurement teams must now combine short-term hedging with long-term supplier diversification.

- Regulatory tightening: Regulators in Europe and select national agencies have begun to re-authorize copper uses under tighter conditions to mitigate soil accumulation and aquatic toxicity. At the EU level, explicit multiyear limits on copper application guide farm-level use reductions. National agencies have simultaneously applied stricter worker-protection and environmental constraints. These actions accelerate demand for copper-reducing strategies and substitutions where agronomically viable.

- Market structure and concentration: The market exhibits moderate concentration: the top three players account for a material share of global revenues, and the top five command a clear majority. This structure creates both consolidation opportunities (buying distribution and specialty formulator assets) and competitive pressures on pricing and innovation.

- Channel bifurcation: Commercial customers (large-scale row and permanent-crop growers) and retail/home-garden buyers are diverging in needs—one demanding cost-effective bulk supply and integrated IPM (integrated pest management) solutions, the other demanding convenience, safety, and compliance assurances. Winning players will customize product/packaging and service layers to each segment.

Competitive landscape — who to watch

The market is populated by multinational crop-protection leaders, regional formulators, and specialist producers. Major crop protection and chemical firms, together with established specialty formulators and agricultural distributors, are pursuing slightly different plays:

- Large agrochemical groups with broad portfolios are leveraging formulation science and channel reach to defend pricing and to bundle liquid copper options with complementary fungicides and fungicide-resistance management programs.

- Regional and specialty players focus on targeted formulations (e.g., novel liquid complexes, organic-certified options) and distributor relationships to secure shelf and application preference in local markets.

- Retail and consumer-focused firms compete on convenience, labeling clarity, and compatibility with consumer-grade application equipment.

Representative names covered in our competitive assessment include multinational incumbents and specialist formulators. For each, the report analyzes: product and formulation pipelines, channel footprint, labeling/regulatory posture, recent commercial and M&A activity, and a scorecard for 2026 competitive posture. The analysis highlights how different go-to-market moves—such as acquiring distribution assets or launching differentiated copper complexes—affect share and margin trajectories.

Regulatory and raw-material shocks: planning templates

Policy shifts and commodity moves are not theoretical. Recent regulatory authorizations in certain European jurisdictions have imposed stricter use conditions and worker-safety requirements for copper products. Simultaneously, raw-material benchmarks show elevated spot prices for copper salts, and trade-policy proposals have the potential to raise import costs materially in key manufacturing hubs.

Our report provides actionable templates that link these shocks to company KPIs: price-to-end-user elasticities, pass-through rates by channel, margin sensitivity by formulation, and contingency playbooks (e.g., temporary surcharge mechanics, supplier nomination, reformulation timelines). These templates are designed for rapid adoption in 2026 budget and procurement cycles.

Practical recommendations for 2026

- Immediate (0–6 months): Establish copper feedstock hedging and diversify suppliers; audit product labels and worker-safety instructions to ensure compliance with tightening authorizations; pilot premium, low-application-rate formulations where agronomically feasible.

- Near term (6–18 months): Rebalance portfolio toward higher-margin liquid formulations with differentiated application benefits; pursue selective distribution acquisitions to shore up retail and regional coverage; deploy field trials that quantify copper-reduction efficacy to support stewardship claims.

- Strategic (18–36 months): Invest in formulation R&D focused on lower-copper-content efficacy, alternative actives, and adjuvant technologies; integrate digital agronomy services to lock-in customers through decision-support and residue-monitoring programs; assess vertical integration opportunities for upstream copper raw-material processing.

Why PW Consulting’s models matter for C-suite decisions

Executives reading market headlines need tools that translate macro narratives into actionable choices. Our report’s combination of demand modelling, regulatory scenario matrices, and commercial playbooks converts uncertainty into ranked options with quantified impacts on revenue, margin, and working capital. The models are designed specifically for incorporation into 2026 operating plans—delivering ROI-calibrated guidance for pricing, procurement, product investment, and M&A prioritization.

A final note on data access — the “trailer” approach

This article is intentionally a strategic preview. We demonstrate the depth of our analysis—coverage of historicals (2020–2025), an explicit 2026 base, a full forecast through 2032, and a validated CAGR figure—while withholding detailed segment-level tables and exact numerical splits by region, formulation, and application. Those granular datasets and the full financial model are available exclusively in the full report and the accompanying data pack.

If your 2026 planning cycle requires a rapid, evidence-backed guide to procurement strategy, product prioritization, or M&A, PW Consulting’s Liquid Copper Fungicide report provides the executable outputs you need to act with confidence.

Next steps

- For immediate access to the full report, proprietary models, and client workshops tailored to your portfolio: request the complete report and a briefing session through our website or your PW Consulting account manager.

- For custom scenario runs (e.g., with in-house procurement contracts or regional exposure maps), engage our analytics team to adapt the model to your internal data and decision timelines.

PW Consulting stands ready to help leadership teams convert regulatory uncertainty and commodity volatility into competitive advantage in the evolving liquid copper fungicide marketplace.

For detailed analysis of this topic, please visit the official page:Liquid Copper Fungicide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com