AI-Integrated Surgical Navigation Systems Market Dynamics: Key Drivers and Restraints

Other |

2026-06-22 08:51:05

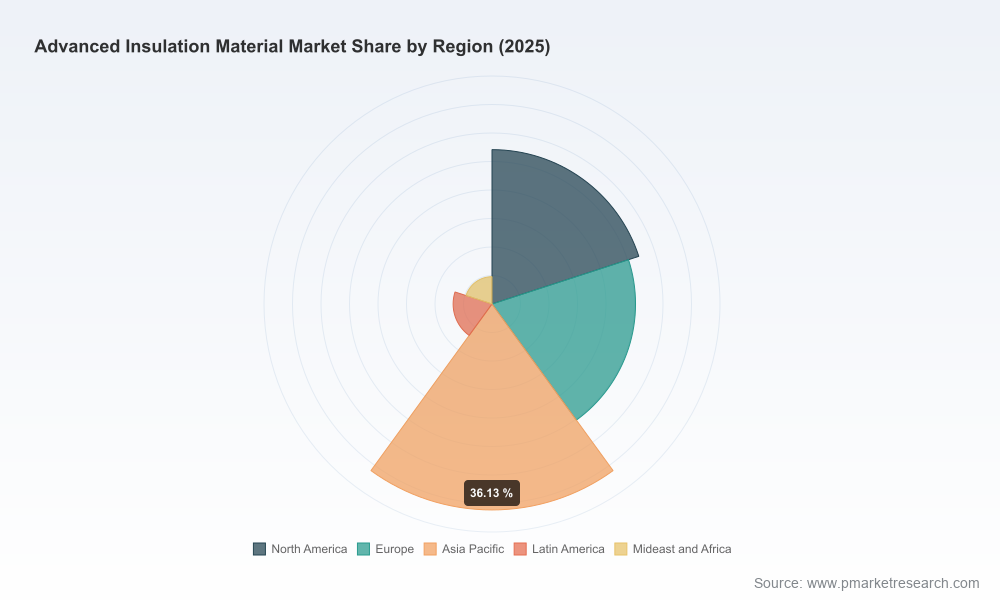

PW Consulting’s new Advanced Insulation Material Market Research (base year 2025) presents a forward-looking framework for executive decisions in 2026. The global market is on a sustained expansion path — moving from an estimated market size of USD 15.25 Billion in 2025 to a projected USD 28.32 Billion by 2032, reflecting a compound annual growth rate (CAGR) of 9.24% across the 2026–2032 forecast window. This briefing summarizes the report’s strategic value, highlights industry dynamics that will shape competitive advantage in 2026, and outlines the practical tools included in the full study that boards, business unit leaders, and M&A teams will need to act decisively.

Advanced Insulation Material Market Research

Timing: 2026 is the year when several regulatory, supply and trade inflection points converge — making short- and medium-term choices (capacity, sourcing, product roadmap) materially more consequential for long-term profitability.

Advanced Insulation Material Market Research

Growth trajectory: With a high-single-digit CAGR through 2032, advanced insulation is transitioning from a niche premium market into mainstream capital-allocation conversations across energy, construction, transport, and industrial end-markets.

Advanced Insulation Material Market Research

Concentration dynamics: Market concentration is moderate — the top three players do not dominate overwhelmingly, and the leading five together capture under half of global market value — creating space for targeted scale plays and differentiated technology strategies.

Input-cost volatility: Feedstock volatility and constrained intermediates have pushed raw-material inflation into the sector. This is driving two near-term responses: (a) accelerated materials substitution and blend-optimization projects by manufacturers, and (b) renewed emphasis on backward integration or secured long-term feedstock contracts.

Regulatory tightening: Updated construction-product and chemical regulations in key markets are raising minimum performance and environmental thresholds for insulation products. Compliance timelines in 2026 will force product reformulations, new testing routines, and re-certification bottlenecks that, if not anticipated, could delay market access for certain SKUs.

Trade and logistics friction: New trade barriers and rising freight surcharges are elevating landed cost for transcontinental shipments. Commercial teams must reassess sourcing footprints and total cost-to-serve rather than rely on unit costs alone.

Decarbonization and product performance: Buyers (developers, OEMs, utilities) are starting to equate thermal efficiency with embedded carbon. Expect procurement specifications to incorporate lifecycle and embodied-carbon metrics alongside thermal performance, favoring suppliers that can demonstrate low-carbon supply chains and certifiable product passports.

Portfolio re-mapping: Segment-level growth is uneven — certain advanced material classes and end-market use-cases will considerably outpace the broader market. Companies should map R&D, commercial and capex priorities to high-growth product–application clusters and de-emphasize legacy low-return areas.

Cost-to-serve optimization: Elevated logistics and input-cost uncertainty mean pricing alone won’t protect margins. Firms must redesign distribution networks, re-evaluate regional manufacturing footprints, and adopt dynamic surcharge mechanisms that preserve competitiveness without sacrificing volume.

Regulatory-first product design: Compliance timelines and evolving measurement standards mean product launches must be underpinned by regulatory roadmaps and third-party validation to avoid costly post-launch remediation.

M&A and partnerships: Given the market’s moderate concentration, acquisitive scale-ups and technology bolt-ons remain an effective route to capture specialized capabilities (e.g., aerogel processing, cryogenic systems, high-temperature blankets) and accelerate access to targeted end-markets.

The competitive field combines large chemical and building-material legacy players with specialist advanced-material firms. The ecosystem’s structure favors incumbents that can deploy capital at scale, while also leaving meaningful white space for technology-focused entrants that solve narrow, high-value problems.

BASF SE — With broad upstream chemical capabilities, BASF remains a strategic bellwether for commodity-to-specialty transitions in insulation foams. Recent capacity investments underscore a play to secure margin through scale and vertical integration.

Dow Inc. — Dow’s emphasis on next-generation PIR systems and trade-show visibility indicates a two-pronged commercial strategy: push premium performance products while defending share in core construction channels.

Saint-Gobain — Combining traditional mineral wool portfolios with aerogel-based offerings positions Saint-Gobain to capture both volume-driven and specification-heavy building projects, particularly where sustainability credentials are decisive.

Rockwool and Knauf Insulation — These materials and systems players are doubling down on acoustic and fire-performance differentiation, leveraging product-system thinking to capture share in façade and retrofit programs.

Aspen Aerogels and Cabot Corporation — Technology specialists focused on aerogels and composites are commercializing applications in EV battery thermal management, subsea and cryogenics, translating lab-led IP into higher-margin, application-specific solutions.

Armacell, Kingspan, Owens Corning — These firms blend manufacturing scale with channel reach; their competitive advantage lies in product breadth, distribution relationships and the ability to cross-sell into adjacent building and industrial ecosystems.

Recent corporate activity — from new aerogel EV applications and capacity expansions to certification wins and targeted product launches — signals that incumbents and specialists are both investing along complementary dimensions: scale, sustainability credentials, and high-value applications.

PW Consulting’s full report is built to be operational. It contains:

Proprietary demand model and scenario engine: configurable by macro scenario, feedstock price path, and regional build-out timelines so teams can stress-test investment cases.

Regulatory and standards matrix: jurisdictional timelines, compliance impact maps, and mitigation playbooks tied to product design and labeling.

Supplier and cost-supply maps: practical guidance on alternative sourcing, contract structuring, and landed-cost calculators tailored to trans-Pacific, intra-Europe and near-shore production strategies.

Commercial playbooks: go-to-market options for premium vs. volume channels, specification-winning tactics for OEMs and building developers, and channel-partner scorecards.

M&A and partnership pipeline: curated target profiles, valuation heuristics, integration-risk checklists and a short list of high-priority bolt-on candidates identified by capability gap analysis.

Risk register and mitigation templates: covering raw-material shocks, regulatory non-compliance, trade disruptions and logistics surcharges with actionable mitigation steps and decision triggers.

Immediate (0–6 months): Lock in multi-year feedstock arrangements or hedges for critical intermediates; prioritize regulatory compliance audits for products sold in public-building and infrastructure tenders.

Near term (6–18 months): Accelerate pilots for high-value application segments (e.g., battery thermal management, deep-cryogenic systems) where technology specialists command premium pricing and defensible margins.

Medium term (18–36 months): Rebalance manufacturing footprint toward a hybrid model — regional plants for volume-facing product lines and centralized centers of excellence for specialty materials — to reduce landed-cost exposure and preserve innovation throughput.

Strategic: Build a 24–36 month M&A pipeline focused on acquiring differentiated processing capabilities, control over critical microporous materials, or tested channel access into fast-growing end-markets.

Consider this brief a strategic “trailer”: it highlights the core forces shaping the sector, reveals where value will accrue, and signals the operational playbooks that will convert market growth into sustainable margin expansion. The full PW Consulting report contains the proprietary segment-level datasets, price and margin simulations, regional demand maps, supplier scorecards and actionable M&A targets that boards and transaction teams require to execute with confidence in 2026.

For executives preparing capital allocation decisions, procurement resets, or M&A strategies this year, the next step is a tailored briefing with our industry and transaction teams. PW Consulting will overlay your portfolio, P&L sensitivities and risk tolerances against the scenarios in the report to produce a decision-ready roadmap that captures upside and limits downside through 2032.

For detailed analysis of this topic, please visit the official page:Advanced Insulation Material Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com