Technical Surface Insulation Evolution: Analyzing Key Drivers Steering Global Fireproof Ceramic Consumption

Other |

2026-06-15 12:51:42

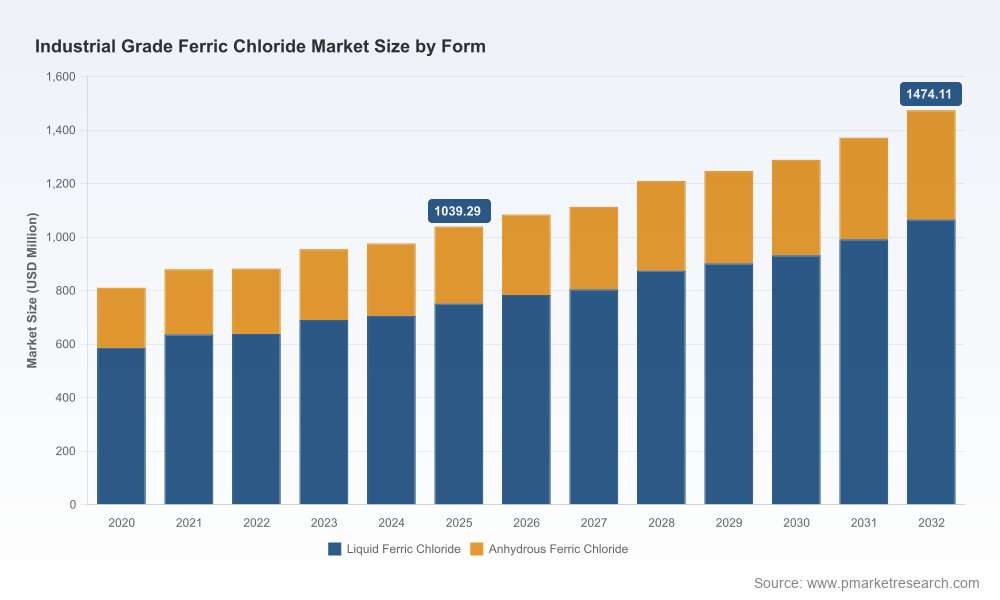

PW Consulting’s new Industrial Grade Ferric Chloride Market report (base year 2025; forecast period 2026–2032) equips executives with the pragmatic intelligence required to make high-consequence procurement, investment, and M&A decisions in 2026. Our modeling shows the global market approaching a multi‑billion-dollar scale over the forecast window, expanding at a compound annual growth rate (CAGR) of 5.12% from 2026 through 2032. This briefing summarizes the report’s strategic value, highlights the risk vectors likely to shape supplier economics in 2026, and outlines the operational playbook buyers and investors must deploy—while preserving the detailed segment and supplier-level metrics available only in the full report.

Industrial Grade Ferric Chloride Market

Regulatory tightening and capital cycles converge. Stricter effluent limits and nutrient removal mandates continue to elevate demand for iron-based coagulants. At the same time, public and private water infrastructure investment plans that were deferred in earlier cycles are moving into execution, creating discrete demand pockets that will crystallize supplier share and margins during 2026.

Industrial Grade Ferric Chloride Market

Feedstock and production bottlenecks will determine near-term pricing and availability. Ferric chloride production is materially dependent on inputs from the chlor‑alkali and steel sectors. Reductions in chlor‑alkali capacity or depressed steel scrap availability have historically constricted ferric chloride supply; these linkages mean chemical buyers must treat ferric chloride as a cross-sector strategic raw material, not a routine commodity.

Industrial Grade Ferric Chloride Market

Market concentration is meaningful but not prohibitive. The market’s top tiers capture a dominant share of production, which creates countervailing dynamics: incumbents can exert pricing discipline, but meaningful opportunities remain for regional players and niche specialists to win business through service, certification, and technical differentiation.

Market sizing & forecast framework: transparent, auditable modeling that reconciles historical shipment data with supply‑side plant capacity and projected demand drivers for the 2026–2032 horizon.

Segment-level demand scaffolding: demand drivers and growth levers by form (solution vs. solid), application class, and industry verticals—presented as directional demand scenarios rather than raw allocation tables, to support procurement and product prioritization without exposing confidential client-sensitive splits in this synopsis.

Supplier scorecards and capability maps: operational profiles for the material producing base—capacity types, certification footprint, quality grades offered, and route‑to‑market strengths—designed to support dual‑sourcing and tender strategy decisions.

Supply‑risk heatmaps: risk-adjusted analyses capturing feedstock exposure (chlor‑alkali and steel), utility dependence, logistics choke points, and regulatory certification risk (e.g., potable water standards).

Procurement playbook: tactical templates for contracting (price adjustment clauses, minimum‑take clauses, force majeure definitions tailored to feedstock constraints), inventory optimization heuristics, and supplier segmentation for commercial negotiations.

Investment & M&A playbook: screening criteria and valuation adjustments for capacity add-ons, brownfield expansions, and bolt-on acquisitions—coupled with a shortlist of archetypal target profiles (regional producers with certified products, toll manufacturers with spare capacity, and integrated chemical groups).

Product and formulation roadmaps: guidance on opportunities for differentiated offerings (stabilized solutions, blended coagulants, high‑purity anhydrous grades) and commercialization timelines.

Scenario planning toolset: three executable scenarios (constrained supply / premium pricing; balanced market; volume‑led competition) with trigger points, KPIs, and contingency actions for each.

The competitive field combines global chemical majors, regional specialists, and vertically integrated producers. Our analysis profiles leading players across manufacturing footprint, certification posture, technical capabilities, and commercial orientation:

PVS Chemicals — A North American specialist with multiple domestic production sites and certified product lines. Strengths: supply reliability for water and industrial customers, NSF/ANSI certification credentials, and strong service orientation. Risk: regional feedstock shocks and single‑market concentration for certain product lines.

Kemira (Water Solutions) — Global footprint and multi‑site production in North America and Europe provide deep customer relationships in municipal and industrial water treatment. Strengths: integrated water chemistry portfolio and scale. Risk: exposure to cyclical raw material pricing and the capital intensity of maintaining regulatory-compliant plants.

Tessenderlo Group — European producer with emphasis on high‑purity grades and sludge dewatering performance. Strengths: technical product differentiation. Risk: European cost base versus lower‑cost competitors.

BASF — Offers both anhydrous and solution grades and benefits from integrated chlorine electrolysis capacity in Europe. Strengths: integration and product breadth across industrial applications. Risk: strategic focus may prioritize higher‑margin specialty volumes over standard coagulant volumes.

Regional and emerging producers (India, China, Middle East) — Several medium‑to‑large capacity plants target water treatment, PCB etching, and surface treatment markets. Strengths: cost competitiveness and export orientation. Risk: certification gaps for potable water applications and quality consistency variability across producers.

Our report quantifies market concentration metrics and interprets what those metrics mean for strategic players. While the top-tier producers control a sizable share of global capacity, the remaining market remains sufficiently fragmented to permit strategic entrants and contract manufacturers to secure profitable niches—particularly those that can offer certification, consistent supply, and tailored technical support.

Chlor‑alkali linkage: fluctuations in chlorine availability and chlor‑alkali economics propagate directly into ferric chloride production cost and availability. Companies should build feedstock‑sensitive procurement scenarios and model margin sensitivity to chlorine price movements.

Steel and scrap dependency: where ferrous feedstock derives from scrap or integrated ferrous sources, shifts in steel demand and scrap markets can create second‑order supply shocks. This creates opportunity for feedstock substitution strategies and vertical integration to stabilize input flows.

Certification as a commercial barrier: potable water use requires compliance with recognized standards; certified suppliers command preferred access to municipal tenders. Buyers should map certification status across potential suppliers and include certification timelines as a factor in sourcing decisions.

Logistics & storage considerations: liquid ferric chloride is transport- and storage‑intensive. On‑site blending or storage assets can be decisive levers to insulate operations from short-term shortages.

For buyers (municipalities, industrial users): adopt a dual‑track sourcing strategy—secure core volumes with certified incumbents under medium‑term contracts while qualifying lower-cost regional sources for overflow and spot coverage. Establish inventory KPIs (days of cover) tied to your treatment criticality.

For chemical producers and toll manufacturers: prioritize investments in certification, quality control, and customer technical services. Consider contracting chlorine co‑supply or partnering with chlor‑alkali operators to reduce feedstock exposure.

For investors: target bolt-on acquisitions that increase access to certified product lines, regional distribution networks, or specialized formulation capabilities. Apply a discount factor to targets with significant feedstock concentration risks.

For R&D and product teams: accelerate development of stabilized solutions and blended coagulants that can command premium positioning based on dosing efficiency, sludge management benefits, or lower lifecycle costs.

For procurement leaders: renegotiate contracts to add transparent price‑link mechanisms tied to clearly defined feedstock indices, and incorporate performance SLAs that reflect supply reliability and certificate maintenance.

Our work translates market projections and operational realities into executable decisions. Clients use the report to:

Right‑size inventory and contract duration to the likelihood of short-term supply contractions identified in our heatmap analysis.

Design acquisition screens and post‑merger integration plans that capture synergies between feedstock control and finished‑goods distribution.

Implement procurement clauses that protect margins from feedstock volatility while preserving supplier incentives to invest in capacity.

Prioritize capital allocation toward certifications, process upgrades, and technical service capabilities that create defensible commercial differentiation.

Ferric chloride is transitioning from a largely commoditized coagulant to a strategically managed material where feedstock exposure, certification, and service capability determine commercial outcomes. As 2026 approaches, stakeholders who adopt an integrated approach—combining procurement sophistication, supplier capability mapping, and targeted investments—will materially reduce execution risk and capture disproportionate value. PW Consulting’s full Industrial Grade Ferric Chloride Market report provides the granular, source‑level data, supplier scorecards, and executable templates required to operationalize the priorities summarized here.

To access the full dataset, detailed segmentation tables, and supplier-level mappings (with certification, capacity, and plant-level notes), please visit the PW Consulting report page. The detailed segment allocations and proprietary company-level analyses are intentionally withheld from this briefing to preserve the actionability of the full report.

For detailed analysis of this topic, please visit the official page:Industrial Grade Ferric Chloride Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com