Blood Plasma Derivatives Market 2026: Strategic Imperatives for Decision‑Makers

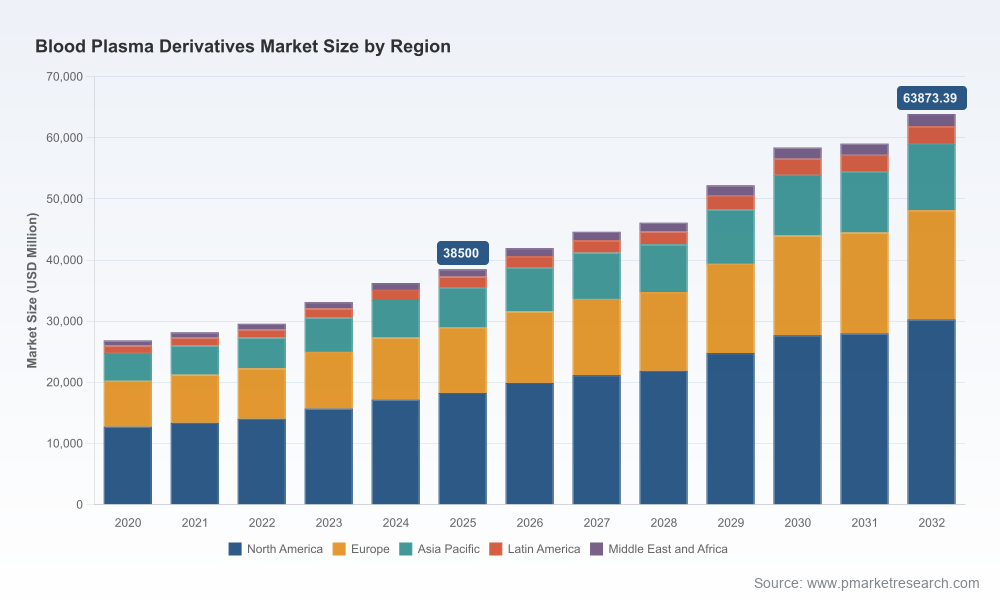

As health systems and biopharma companies prepare budgets and strategic roadmaps for 2026, the global blood plasma derivatives market is entering a phase where volume growth, supply-chain fragility and industrial-scale investments intersect. PW Consulting’s latest market study — covering historical performance (2020–2025) and forward projections through 2032 — finds the market expanding at a robust mid‑single‑digit to high‑single‑digit trajectory (7.5% CAGR across the forecast window), with the industry market value increasing materially from the early 2020s and expected to exceed USD 60 billion by the end of the decade. For executives weighing capacity investments, M&A, or new market entry, the implications are immediate: scale matters, supply matters more, and timing of capital deployment will determine competitive positioning for the next cycle.

Blood Plasma Derivatives Market

Why 2026 is a Pivotal Year

- Near‑term volume and revenue dynamics. Our base‑year analysis (2025) shows a market that has recovered and grown substantially compared with 2020 levels. The first planning year after the report’s base (2026) marks an inflection where committed capacity expansions, regulatory approvals and payer negotiations begun in prior years start to translate into supply and revenue shifts.

- Structural supply constraints. Plasma collection and fractionation remain capital‑ and time‑intensive. Manufacturing lead times—from plasma collection through fractionation and final release—regularly span many months, creating a lag between demand signals and available supply. That lag amplifies the value of early, decisive capacity investments and strategic upstream partnerships in 2026.

- Policy and reimbursement pressure. Regulatory and reimbursement regimes in key markets continue to influence access and pricing; countries pursuing self‑sufficiency will reshape regional demand and sourcing strategies during the 2026–2032 horizon.

What the Report Provides — Practical, Decision‑Grade Content

PW Consulting’s report is designed as an operational playbook for corporate leadership, investment committees and commercial teams. Core deliverables include:

Blood Plasma Derivatives Market

- Market sizing and three‑scenario forecasts (conservative, base, upside) calibrated to real‑world lead times, capacity build‑out schedules and pricing elasticity — enabling CFOs to stress‑test business plans.

- A supply‑chain map with counterparty risk scoring: plasma sourcing channels, fractionation hubs, key CMOs and single‑point‑of‑failure sites, together with mitigation playbooks for short‑ and medium‑term disruptions.

- Regulatory pathway and quality impact analysis for major jurisdictions, identifying timelines and incremental compliance costs associated with viral safety, donor screening and advanced fractionation technologies.

- Commercial and reimbursement intelligence: payer segmentation, tender behaviour archetypes, and a negotiation toolkit for securing favorable formulary placement and tariff structures.

- Investment and M&A decision framework: valuation sensitivities, asset vs. capability buy considerations (plasma centers, fractionation lines, fill/finish), and transaction checklists tailored to the sector’s concentration dynamics.

- Operational playbooks: capacity commissioning roadmaps, automation adoption profiles, OPEX and CAPEX phasing, and productivity benchmarks for fractionation facilities.

- Competitive benchmarking and scenario‑based strategy matrices that link corporate capabilities to likely market outcomes across the forecast horizon.

Competitive Landscape — What the Major Players Are Doing

The sector remains concentrated. The largest global players collectively account for a dominant portion of market supply, creating high barriers to entry for new competitors while simultaneously generating opportunities for adjacent players through specialization and regional strategies.

Blood Plasma Derivatives Market

- Grifols (Barcelona) — continues to pursue European capacity expansion and vertical integration across plasma collection and fractionation. Recent investments to bolster European manufacturing capability indicate a strategic emphasis on controlling lead times and margin retention in core products.

- CSL Behring (CSL Limited, Australia; U.S. operations based in Pennsylvania) — has signaled an aggressive U.S. investment posture, with multi‑hundred‑million to billion‑scale capital commitments and the adoption of robotics and automation in fractionation. Their mix of large‑scale manufacturing and process automation presents a blueprint for competitiveness where throughput and cost per gram matter.

- Takeda (Tokyo) — leveraging a diversified portfolio and targeted manufacturing expansions to secure its position in both immunoglobulin and rare‑disease niches. Strategic emphasis on pipeline products and manufacturing redundancy are visible themes.

- Octapharma (Switzerland) — capacity expansions in Europe reflect a play to capture incremental global demand and to serve as a price‑ and supply‑responsive alternative to the largest incumbents.

- Kedrion, BPL, LFB, Biotest, Sanquin, SK Plasma — collectively, these regional and specialized players emphasize niche leadership (e.g., rare disease indications, national supply mandates, or domestic collection infrastructure). Their agility in regional channels and strong local payer relationships create defensive moats that are attractive to partners and acquirers.

Recent corporate actions — large capital investments, facility awards for automation and doubling of regional capacity — confirm an industry pivot: companies are converting strategic intent into heavy industrial commitments. That trend both alleviates and concentrates supply risks: while aggregate capacity rises, new lines are costly and multi‑year, preserving first‑mover advantages for those with access to capital.

Dynamics Shaping Competitive Advantage

- Upstream control. Organizations that secure plasma sourcing (through owned donor networks, long‑term procurement contracts, or joint ventures) insulate downstream operations from competitive pressure and price volatility.

- Manufacturing scale + modernisation. Investments in automated fractionation and sustainable process technologies reduce unit costs and improve time‑to‑market — crucial in an environment where product release timelines are long.

- Regulatory and quality excellence. Compliance capability is non‑negotiable; firms that embed regulatory forecasting and rapid change‑control processes can accelerate label expansions and geographic launches.

- Payer engagement. Given persistent cost pressures in many health systems, differentiated commercial strategies (outcomes‑based agreements, tiered pricing, and localized reimbursement dossiers) will determine access across markets.

Strategic Recommendations for 2026 Decision Makers

For executive teams planning for 2026, the report identifies a set of prioritized actions that balance risk, capital intensity and time to impact:

- Prioritize upstream partnerships: Lock in plasma supply through diversified sourcing strategies (domestic collection, strategic long‑term contracts, and M&A where feasible) to de‑risk production pipelines.

- Sequence capacity investments: Focus on modular, automation‑friendly expansions that can ramp in 18–36 months rather than single large‑monolithic projects that are inflexible to demand variance.

- Use M&A selectively to acquire strategic capabilities (collection networks, fractionation lines or specialized product portfolios) rather than only revenue growth — integration risk is high and must be planned for.

- Invest in regulatory foresight and quality systems: Establish cross‑functional “regulatory war rooms” to shorten approval timelines for label expansions and geographic launches.

- Negotiate with payers early and design evidence generation programs that anticipate outcome concerns — reimbursement shapes access as much as production capacity.

- Build scenario‑based inventory and procurement policies to manage the 6–12 month product lifecycle realities; use rolling forecasts and optionality in supplier contracts to maintain responsiveness.

- Develop a talent and digital roadmap: Skillsets in biologics manufacturing engineering, regulatory affairs, and supply‑chain analytics will be essential; digital twins and predictive maintenance deliver measurable uptime benefits.

What the Full Report Unlocks (Why You Should Read It)

This release is an executive summary of a comprehensive analysis. The full PW Consulting report provides the granular models, sensitivity analyses and operational artifacts that leaders need to convert strategy into executable plans, including:

- Interactive financial models and scenario stress tests aligned to CAPEX phasing and pricing scenarios;

- Detailed supply‑chain risk heatmaps and supplier contact intelligence for operational execution;

- Regulatory timetables and jurisdiction‑specific compliance checklists;

- Commercial playbooks for payer negotiations, tenders and differentiated product positioning;

- M&A playbooks with valuation ranges, integration risk matrices and a curated short‑list of priority targets and partners.

We intentionally present high‑level strategic insight here to guide 2026 planning conversations while reserving the full analytical datasets, segment tables and proprietary models for the full report. Leaders preparing capital allocations, M&A pipelines or market entry decisions will benefit most from the full dataset and bespoke advisory options PW Consulting provides.

Concluding View

The blood plasma derivatives market is becoming an industrial bioscience sector where operational excellence, upstream control and regulatory competence create durable advantage. Growth is significant and predictable enough to justify major capital programs, yet supply dynamics and long manufacturing cycles make timing and structure of those investments decisive. For organizations that move in 2026 with a clear supply‑first strategy, calibrated capacity investment and payer‑aligned commercialization, the coming seven years present material opportunity. For those that delay, the industry’s concentration and the high cost of entry will make recovery expensive.

Contact PW Consulting or download the full report to access the full forecasting models, strategic playbooks and company‑level intelligence necessary to operationalize these recommendations.

For detailed analysis of this topic, please visit the official page:Blood Plasma Derivatives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com