Industrial Grade Three-Phase Micro Inverter Market — Strategic Preview from PW Consulting

PW Consulting today releases a strategic preview of our forthcoming market research report on the Industrial Grade Three-Phase Micro Inverter Market (base year 2025). This executive briefing outlines why our analysis will be pivotal for boardrooms, corporate strategy teams, and project developers making capital and procurement decisions in 2026. The preview highlights the macro trajectory, critical technology and regulatory drivers, competitive dynamics, and the practical, decision-ready tools included in the full study — while intentionally withholding the complete, granular segmentation to encourage direct access to the full dataset and proprietary dashboards.

Industrial Grade Three Phase Micro Inverter Market

Why this market matters in 2026

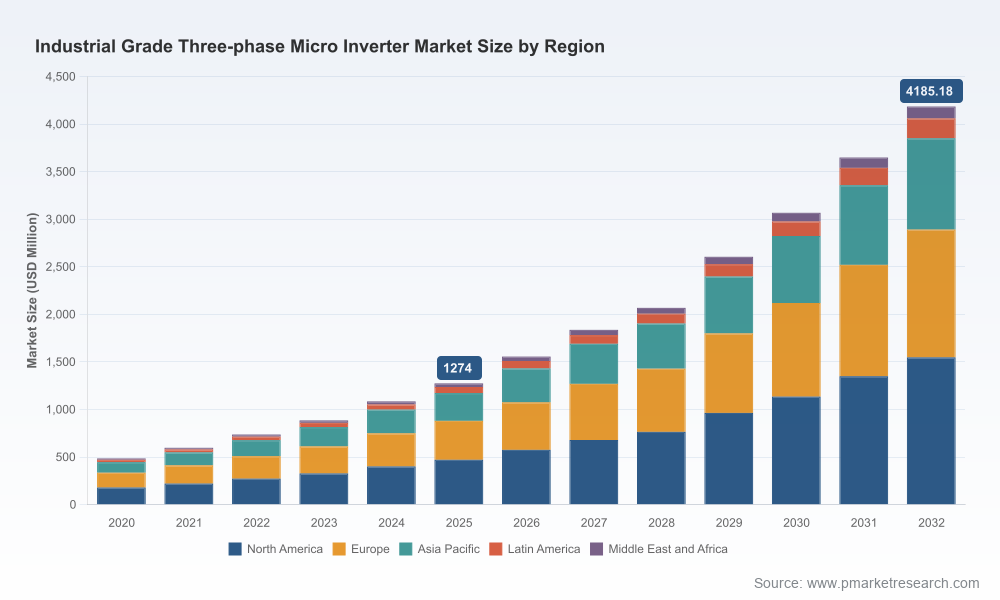

Three-phase microinverters are moving from niche to mainstream in commercial and industrial distributed PV deployments. PW Consulting’s modeling shows the global market expanding rapidly through the forecast window (2026–2032), with a compound annual growth rate (CAGR) of 18.52% from the 2026 baseline. After a period of sustained recovery and adoption between 2020 and 2025, the total market value in 2025 reached a clear inflection point and our 2026 forecast projects a marked acceleration driven by integration into larger rooftop, carport, and industrial-sited systems.

Industrial Grade Three Phase Micro Inverter Market

For executives, the implication is straightforward: suppliers and buyers who position correctly in 2026 can capture disproportionate value. Decisions relating to supplier selection, product roadmaps, localization of manufacturing, and grid-support service offerings will determine competitive positioning as the market consolidates.

Industrial Grade Three Phase Micro Inverter Market

Key macro signals shaping near-term strategy

- Fast structural growth: The market’s high-teens CAGR is supported by an improving cost-performance profile of module-level electronics and increasing preference for module-level optimization in C&I systems.

- Technology inflection: Adoption of advanced power semiconductors (notably GaN) is reducing device footprint and improving peak efficiencies — enabling new three-phase designs purpose-built for 480Y/277 V commercial grids.

- Regulatory tailwinds and constraints: Domestic content policies and national security screening frameworks are already influencing procurement decisions in major markets. Additionally, grid interconnection standards that mandate advanced ride-through and dynamic response (e.g., standards aligned with IEEE 1547 / UL 1741-SB profiles) are elevating the importance of firmware, remote update capability, and certified grid-support functionality.

- Concentration and consolidation: The market exhibits meaningful concentration at the top end; a relatively small set of vendors collectively accounts for the majority share of installed value. This creates opportunities for differentiation through service models, proprietary technology stacks, and channel partnerships.

What’s in the full PW Consulting report (practical, action-oriented deliverables)

Our full report is structured as an operational playbook for 2026 decision cycles. Highlights include:

- Forward-looking market sizing and scenario-based forecasts through 2032, with sensitivity analysis under multiple adoption and policy scenarios.

- Strategic supplier scorecards and a comparative technical benchmarking framework that evaluates efficiency, thermal performance, grid compliance, and serviceability for commercial three-phase models.

- Procurement and sourcing playbooks that translate market dynamics into vendor negotiation levers, localization vs. offshore sourcing trade-offs, and contract structures that mitigate supply-chain and regulatory risk.

- CapEx/Opex modeling templates and ROI calculators tailored to commercial/industrial PV portfolios, enabling project-level and portfolio-level investment decisions.

- Regulatory matrix and compliance checklists mapping key markets to domestic-content, security-screening, and interconnection requirements, including actionable steps for suppliers seeking qualification in priority jurisdictions.

- Supply-chain heat maps and raw-material risk assessments focused on advanced semiconductor availability (e.g., GaN adoption pathways), passive components, and inverter-grade passive cooling solutions.

- Go-to-market recommendations and channel strategies for OEMs, BOS integrators, and system EPCs — including partnership frameworks for module manufacturers, digital service providers, and energy management platforms.

Note: In keeping with our “trailer” approach, the comprehensive region- and application-level splits and the proprietary vendor ranking matrix are available only within the complete report and interactive data package.

Competitive landscape — what to watch in 2026

The industrial-grade three-phase microinverter segment is technologically diverse and strategically contested. A group of established MLPE and inverter vendors are executing differentiated approaches — from deep integration into existing inverter portfolios to aggressive product innovation using GaN and multi-module microinverter topologies.

- Enphase Energy — A prominent challenger that has moved decisively into C&I markets with GaN-based three-phase products designed for 480Y/277 V systems. Enphase’s recent product launch and commencement of domestic shipments underline a strategy focused on meeting domestic-content requirements and simplifying installation for commercial projects. Their approach emphasizes module-level optimization, high efficiency, and grid-support capabilities.

- APsystems (Altenergy Power Systems) — Concentrating on multi-module microinverter architectures and high-voltage three-phase options, APsystems continues to pursue scale in distributed commercial applications through flexible module configurations.

- Hoymiles — Rapidly expanding its high-power three-phase portfolio with multi-module designs for large C&I rooftops. Their value proposition centers on power density, reactive power control, and cost competitiveness targeted at distributed commercial deployments.

- Deye, Chilicon Power, AE Conversion, Envertech, ZJBENY, Sparq Systems — These players represent a mix of regional champions and technology specialists. Their strategies range from leveraging broader inverter ecosystems to offering niche technical differentiation in reliability, serviceability, or form factor.

Competitive pressure will come from both product innovation (higher efficiency, better thermal management, smarter grid interactions) and commercial models (warranty terms, O&M services, and integrated monitoring). The market concentration metrics in our analysis indicate that the top three to five firms control a substantial portion of market value — a dynamic that makes targeted partnerships and channel plays critical for challengers and buyers alike.

Technology, regulation and supply-chain — strategic implications

- GaN and the device frontier: GaN-based power electronics are no longer experimental in three-phase microinverters; they are an enabling technology for higher efficiency and compact, transformer-less architectures. Procurement teams must assess supplier roadmaps for GaN adoption, validation testing, and long-term component availability.

- Standards and firmware: Meeting grid-support standards is a baseline requirement. More important is the supplier’s capability to deliver secure remote firmware updates and a documented compliance path as interconnection requirements evolve — this is increasingly a procurement decision criterion.

- Local manufacturing and policy exposure: Domestic content rules and foreign-entity screening can change project eligibility and financing. Corporates should map regulatory exposure across target markets and consider localized manufacturing or qualified domestic suppliers as strategic insurance.

- Concentration risk: Where a small number of vendors dominate, buyers must design multi-supplier strategies, performance-based contracts, and contingency sourcing to avoid single-supplier disruption.

How executives should use this report in 2026

PW Consulting designed the report for immediate operational use in 2026 planning cycles:

- Boards and strategy teams can use the scenario forecasts to stress-test capital plans and M&A hypotheses.

- Procurement leaders will find the supplier scorecards and contract templates useful for RFQ and vendor qualification rounds.

- Product and R&D teams should use the technical benchmarks and supply-chain maps to prioritize feature roadmaps (e.g., GaN integration, grid services, modular stacking) and to identify strategic component partnerships.

- Project developers and financial sponsors can apply the ROI templates to compare microinverter architectures versus central/string inverter constructs under varied tariff and moratorium scenarios.

Conclusion — actionable intelligence with reserves

PW Consulting’s preview underscores a decisive inflection in the industrial-grade three-phase microinverter market. High growth, accelerating technological change, evolving regulatory constraints, and meaningful market concentration together make 2026 a pivotal year for strategic positioning. Our full report converts these dynamics into executable recommendations, procurement playbooks, and validated financial models designed to support real decisions over the next 12–24 months.

To preserve competitive integrity and to provide maximum value to subscribers, we are intentionally withholding the full region/application-level splits and proprietary vendor ranking tables from this public preview. The complete dataset, interactive dashboards, and consultancy add-ons are available through PW Consulting’s report portal.

Next steps

- Visit PW Consulting’s Industrial Grade Three-Phase Micro Inverter Market report page to access the full report, dataset, and board briefing pack (available to subscribers and enterprise clients).

- Schedule a bespoke executive briefing with our lead analysts to review implications for your portfolio, procurement roadmap, or product strategy.

- Engage our advisory team for tailored scenario modeling, vendor due diligence, or RFx support tied to your 2026 procurement cycles.

PW Consulting — Transforming market intelligence into decisive action for 2026.

For detailed analysis of this topic, please visit the official page:Industrial Grade Three Phase Micro Inverter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com