Intelligent Automatic Warehouse And Logistic Equipment Market: Strategic Outlook for 2026 Decision-Makers

Executive summary

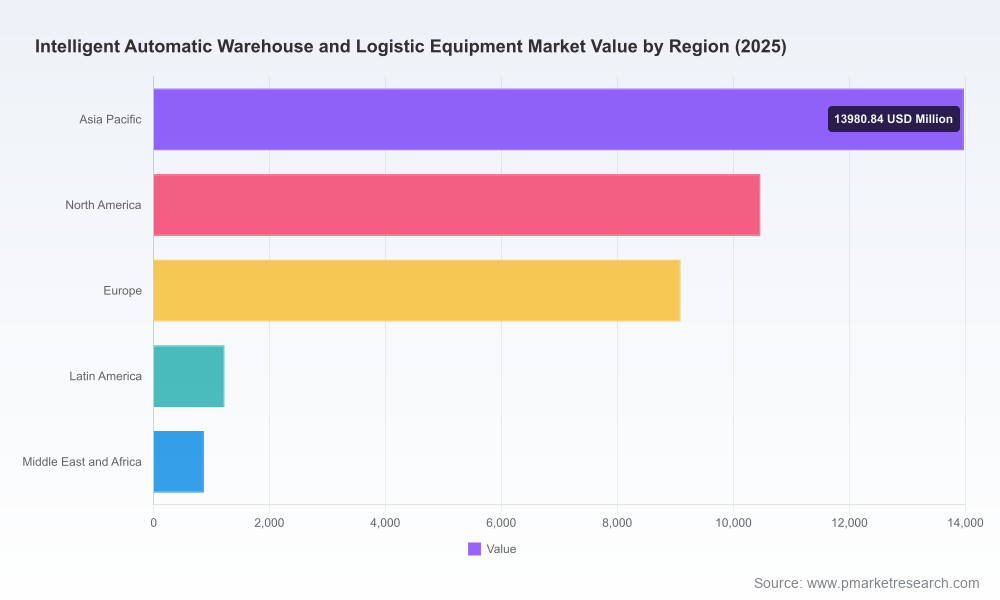

PW Consulting’s new market research brief on the Intelligent Automatic Warehouse and Logistic Equipment Market offers a focused, decision-ready perspective for organizations planning capital allocation and operational transformation in 2026. The market has expanded rapidly since 2020, reaching an estimated USD 35.6 billion in our 2025 base year, and our forecast shows sustained momentum through 2032 — underpinned by a compound annual growth rate (CAGR) of 12.04% across the 2026–2032 forecast window. By 2032 the market is projected to be materially larger than the 2025 base, reflecting accelerating adoption of automation, robotics and digital orchestration across distribution and fulfillment networks.

Intelligent Automatic Warehouse And Logistic Equipment Market

Why this report matters for 2026 corporate strategy

- Time-to-value pressure: Boards and COOs face competing demands to increase throughput, lower fulfillment cost per order, and reduce labor exposure. The report translates market growth into practical benchmarks for payback and capacity planning.

- Technology choice complexity: AMRs, AS/RS, conveyors, sortation and warehouse software increasingly function as ecosystem components. Our analysis helps executives evaluate modular vs. monolithic approaches, total cost of ownership (TCO) and upgrade paths.

- Procurement and risk: Volatile raw-material costs, tariff shifts and wage inflation require procurement strategies that protect margins. The research provides scenario-based cost sensitivities and contracting levers for 2026 negotiations.

- Regulatory and ESG alignment: Energy efficiency and regenerative system requirements are becoming de facto constraints on new projects. The report identifies compliant solution architectures that also enhance lifecycle economics.

What the report delivers (practical, operationally focused)

This is not an abstract market essay. PW Consulting’s deliverables are built for action and include:

Intelligent Automatic Warehouse And Logistic Equipment Market

- Concise market sizing and validated forecasts (2020–2025 history; 2026–2032 projections) that translate growth trends into capacity, spend and replacement cycles.

- Vendor and technology roadmaps outlining where robotics, AI-driven orchestration, and storage systems will create incremental value over the next three years.

- Implementation playbooks: RFP templates, phased deployment roadmaps, KPI sets for commissioning and steady-state operations.

- Financial toolkits: TCO calculators, scenario models sensitive to steel and aluminum pricing, labor wage inflation, and tariff regimes.

- Competitive intelligence: qualitative vendor assessments, partnership archetypes and go-to-market strategies for integrators, system OEMs and software suppliers.

- Case studies and lessons learned from live deployments to surface common pitfalls in scaling from pilot to network-wide rollouts.

Competitive landscape — what leaders are doing

The market balances large, system-oriented incumbents and fast-moving specialists. Large integrators and OEMs remain dominant in full-facility projects, delivering end-to-end AS/RS, conveyors, sortation and execution software; robotics and AMR specialists are attacking fulfillment and last-mile use-cases with rapid-deployment models and subscription-friendly commercial terms. Key strategic threads we observed across leading suppliers include:

Intelligent Automatic Warehouse And Logistic Equipment Market

- Platformization and software-first playbooks — companies are bundling software, lifecycle services and data products to move revenue from one-time equipment sales toward recurring streams.

- Hybrid partnering models — traditional OEMs increasingly partner with AMR and software startups to accelerate time-to-market and extend solution breadth.

- Regional engineering hubs — vendors are optimizing delivery by locating pre-configured modules closer to demand centers while retaining central R&D for core technologies.

Representative companies covered in the competitive review include global systems integrators and OEMs as well as robotics pioneers and software-led providers. Our analysis assesses strengths in engineering scale, service networks, software maturity and go-to-market models — and identifies where niche specialists can win on speed, flexibility and lower up-front capital.

Market structure and concentration

The intelligent warehouse equipment market remains meaningfully fragmented: the top three vendors account for under a fifth of total market activity, and the top five together represent only about a quarter. This dispersion creates opportunities for regional leaders, vertical specialists and technology-focused entrants, while also making strategic consolidation or partnerships an attractive route for companies seeking scale.

Dynamics shaping 2026 decisions — tailwinds and risks

- Labor and operational economics: Persistent labor shortages and wage inflation are a primary catalyst for automation. Organizations should model productivity gains not only as headcount replacement but as flexibility that enables new fulfillment models.

- Material and tariff volatility: Rising steel and aluminum costs, coupled with recent tariff shifts, have increased project price uncertainty. Our scenario models quantify the sensitivity of project economics to raw-material escalations and suggest contracting strategies to hedge supplier exposure.

- Energy and sustainability mandates: Regulatory mandates and corporate ESG commitments are steering equipment choices toward energy-efficient designs and regenerative technologies. These choices often carry longer payback horizons but better long-term operating economics and lower regulatory risk.

- Technology acceleration: Advances in AI-driven orchestration (including multi-agent coordination), perception, and modular robotics are compressing deployment timelines and expanding the addressable set of automation use-cases.

Recent industry signals

- Trade shows and conferences in early 2026 reaffirmed vendor focus on flexible, software-driven solutions and demonstrated incremental hardware innovations targeted at throughput and energy efficiency.

- Vendor technology updates highlighted AI trends such as multi-agent coordination for fleets of warehouse robots — a capability that materially improves utilization in dynamic fulfillment environments.

- Macro policy changes and commodity movements are already driving procurement cycles and have shifted buyer preference toward contract structures that share price risk.

Actionable recommendations for executives in 2026

Below are prioritized actions tailored to management horizons. Each recommendation aligns to the practical tools available in the PW Consulting deliverables.

- Immediate (0–12 months): Run an automation readiness audit focused on throughput bottlenecks and labor-sensitive nodes; launch one or two modular pilots with clear success metrics and an integration plan into existing WMS/ERP systems.

- Near term (12–24 months): Negotiate project contracts with supplier price-adjustment clauses tied to defined commodity indices; require lifecycle service agreements that guarantee uptime and data access for continuous optimization.

- Medium term (24–36 months): Commit to modular AS/RS or AMR rollouts to scale capacity in step functions rather than single-site, high‑risk builds; invest in orchestration software and data plumbing to extract value across sites.

- Strategic (36+ months): Consider platform plays — acquiring or partnering with software/robotics providers to capture recurring revenue and ensure interoperability across your distributed network.

- Risk management: Build commodity- and tariff-sensitivity into capital approval processes and maintain contingency capital for material-driven cost shocks.

How PW Consulting’s report helps you act in 2026

Our study is structured to move organizations from insight to implementation. We combine rigorous market sizing and scenario models with procurement playbooks, vendor evaluation frameworks and detailed deployment checklists. For leadership teams, the report is a toolkit that translates projected market growth and technology trajectories into quantified investment cases, tender packages, and post‑implementation KPIs.

Next steps

PW Consulting’s Intelligent Automatic Warehouse and Logistic Equipment Market report functions as a strategic “trailer” — it demonstrates analytical depth and operational readiness while reserving full segmentation tables, vendor scorecards and granular financial models for the complete report. For a tailored executive briefing, a sample toolkit or to discuss scenario modeling for your network, visit the PW Consulting reports page or contact our advisory desk to schedule a 60‑minute strategic consultation.

For detailed analysis of this topic, please visit the official page:Intelligent Automatic Warehouse And Logistic Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com