Myths Busted About Effective Hair loss Treatment in Riyadh

Health |

2026-05-06 07:41:02

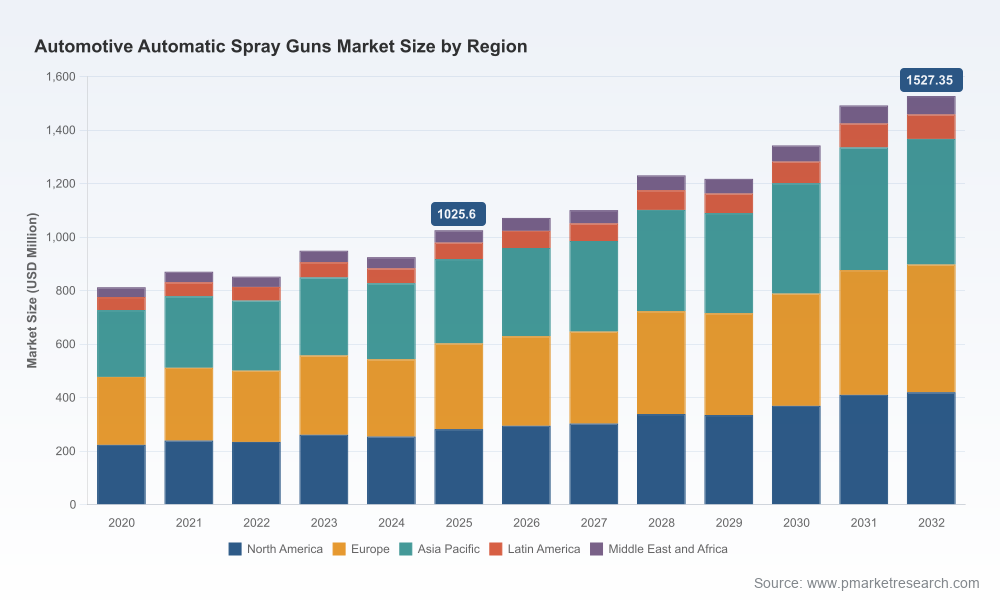

PW Consulting’s latest market research on the Automotive Automatic Spray Guns market synthesizes five years of historical performance (2020–2025) with a forward-looking forecast through 2032. The market reached a base-year value of USD 1,025.6 Million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 5.85% across the 2026–2032 forecast window, reaching an anticipated USD 1,527.35 Million by 2032. Our analysis combines quantitative forecasting with practitioner-oriented diagnostics — supply chain stress-testing, regulatory compliance playbooks, and supplier benchmarking — to deliver immediately actionable guidance for OEMs, tier suppliers, aftermarket service providers, and strategic investors planning activity in 2026.

Automotive Automatic Spray Guns Market

Timing capital expenditure: The market’s mid-single-digit CAGR masks pockets of accelerated adoption tied to plant modernizations, HVLP/electrostatic retrofits, and robotic integration. Our scenarios clarify when to accelerate CAPEX to capture premium productivity gains versus when to defer to preserve cash.

Automotive Automatic Spray Guns Market

Regulatory-driven replacement cycles: Tightening VOC and spray technology mandates (e.g., recent EPA and regional rules with phased deadlines through 2028, and continuing EU VOC restrictions) are shifting equipment specs and total cost of ownership considerations. The report quantifies regulatory impact vectors and the implied upgrade timelines for compliance and competitive parity.

Automotive Automatic Spray Guns Market

Supplier strategy: Market concentration analysis (CR3 ~38.5%; CR5 ~52.7%) highlights an industry that is neither fragmented nor dominated by a single incumbent. This creates windows for selective partnership or consolidation strategies; our supplier scorecards identify when to partner, when to dual-source, and when to pursue vertical integration.

At the headline level, the market grew from the lows observed early in the decade to exceed one billion USD in 2025, with a steady, policy- and productivity-driven expansion expected to 2032. However, that aggregate growth conceals three operational dynamics that will determine winners and losers in 2026:

Technology mix shifts — increasing adoption of high-transfer-efficiency systems (HVLP, electrostatic, and emerging airless-electrostatic hybrids) in new OEM lines, coupled with selective retrofits in high-throughput shops.

Capex vs. service-model tradeoffs — OEMs prioritize upfront precision and robotics compatibility; refinishing shops often favor modular, lower-capex investments paired with service contracts.

Cost pressure from inputs — specialty alloys and nozzle-grade stainless steel are rising in cost, forcing premium gun manufacturers to re-evaluate bill-of-materials, pricing, and aftermarket strategies.

This study was designed for executives who need to move from insight to action in 2026. Key deliverables include:

Financial modelling toolkit — pre-built TCO and payback calculators that incorporate purchase, integration, maintenance, consumables, and regulatory compliance costs for different spray technologies.

Scenario playbooks — three demand and compliance scenarios (baseline, accelerated compliance, and conservative CAPEX) with recommended timing for procurement, trial deployments, and full-line rollouts.

Supplier benchmarking and RFP templates — comparative scorecards on quality, automation friendliness, aftermarket availability, and cost-to-serve; ready-to-use RFP checklists tuned to OEM and refinish buyer needs.

Integration and maintenance protocols — robotics and paint-line integration checklists, downtimes minimization approaches, and maintenance cadences proven to reduce defects and improve first-pass yields.

The market’s competitive fabric blends long-established industrial players with agile regional manufacturers. Our qualitative and operational assessment focuses on the core vendors shaping procurement and innovation dynamics:

Graco Inc. (Minneapolis, MN, USA) — Known for high-transfer-efficiency lines and strong robotic integration (e.g., PerformAA Auto, Pro Xp Auto Electrostatic). Strengths: global service footprint, proven performance in high-volume OEM lines. Strategic implication: Best partner for large-scale automation projects where integration and uptime are prioritized.

SATA GmbH & Co. KG (Kornwestheim, Germany) — Renowned for ergonomic design and precision atomization; active in both OEM and refinish channels. Recent product previews indicate a push upmarket. Strategic implication: A core supplier for premium finishes and Tier 1 OEMs focused on aesthetic differentiation.

Anest Iwata Corporation (Yokohama, Japan) — Offers advanced atomization platforms (WA series) with a reputational edge in finish quality. Catalog refreshes signal a continued emphasis on performance upgrades. Strategic implication: Attractive for programs where finish quality and parts variability demand high atomization control.

Nordson Corporation (Westlake, Ohio, USA) — Strong in electrostatic and powder systems for high-volume coating lines. Strategic implication: A primary contender where precision metering and electrostatic efficiency drive material savings.

EXEL Industries / Sames (Épernay, France) — Offers diverse airspray, airmix and electrostatic guns, with strengths in assembly line standardization. Strategic implication: Best suited for multi-site standardization programs and integrator partnerships across Europe and beyond.

Carlisle Fluid Technologies (DeVilbiss, Binks) (Scottsdale, AZ, USA) — Focused on transfer efficiency and legacy industrial strength. Strategic implication: Reliable incumbent for manufacturers seeking proven solutions and strong aftermarket support.

Ningbo Lis Industrial & Zhejiang Rongpeng (China) — Cost-competitive, customizable solutions targeted to production and refinishing customers; notable for flexible OEM relationships. Strategic implication: Attractive for price-sensitive retrofit programs and regional sourcing strategies where lead times and customization matter.

Partnerships and training alliances (e.g., a 2026 strategic supplier partnership with a major technical training institute) signal a focus on workforce capability building — important when adopting more automated gun systems.

Product previews and catalog refreshes from key European and Japanese vendors indicate an infusion of incremental performance upgrades rather than a disruptive technology shift — suggesting that buyers should prioritize integration and lifecycle cost over speculative technology bets in 2026.

Regulatory tightening (regional VOC rules and air-quality mandates) is accelerating demand for HVLP and comparable high-efficiency technologies. Compliance deadlines through 2028 create a compressed window for large-scale retrofits in some jurisdictions. Concurrently, rising prices for stainless steel and specialty alloys are increasing unit manufacturing costs for premium guns and spares.

Mitigation approaches we recommend: hedge long-lead components via multi-year contracts, co-design nozzle geometry to enable alternative alloys without sacrificing finish quality, and build regulatory compliance into procurement specifications rather than as a post-purchase retrofit.

Run a 12–24 month pilot program before full-line replacement. Use the report’s TCO calculators to compare pilot outcomes across performance metrics and payback timelines.

Adopt a phased procurement strategy tied to regulatory milestones — prioritize lines in jurisdictions with near-term compliance deadlines and defer lower-risk sites to benefit from incremental product improvements and price normalization.

Negotiate modular service agreements that include spare-part pools and training commitments; workforce readiness is the single biggest hidden cost in automation rollouts.

Consider supplier diversification: combine established global vendors for core automated lines with regional manufacturers for retrofit and lower-volume applications to optimize cost and lead times.

For investors and M&A teams: target companies that demonstrate clear service monetization, aftermarket strength, or unique integration IP rather than pure hardware plays, given continued consolidation dynamics.

This research is structured to be a working tool for procurement, engineering, strategy, and M&A teams. Beyond market sizing and forecasts, the report includes:

Detailed supplier scorecards and integration risk matrices;

Regulatory impact timelines and compliance cost envelopes;

Scenario-based CAPEX calendars and sensitivity analyses for raw-material cost shocks;

Practical appendices: RFP templates, maintenance checklists, and ROI models that can be dropped into 2026 budget processes.

For 2026 planning, leaders must balance compliance-driven urgency with prudent CAPEX sequencing. PW Consulting’s Automotive Automatic Spray Guns report turns headline growth and a 5.85% CAGR into operationally relevant actions: where to invest, whom to partner with, and how to protect margins in the face of rising input costs and regulatory complexity. To access the full set of data tables, segmented revenue breakdowns, and the complete supplier benchmarking toolkit — including downloadable models and RFP templates — please visit the PW Consulting report page or contact our industry team to arrange a brief walkthrough tailored to your organization’s priorities.

For detailed analysis of this topic, please visit the official page:Automotive Automatic Spray Guns Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com