Golf Equipment Market Overview: Key Drivers and Challenges

Other |

2026-03-02 09:30:23

As companies prepare 2026 roadmaps, the Bluetooth audio IC landscape is reshaping product architectures, supply-chain strategies, and partnership economics. PW Consulting’s Bluetooth Audio IC Market report (base year 2025; forecast 2026–2032) synthesizes commercial, technical, and geopolitical forces into a decision-ready framework. The market has more than doubled since 2020 — rising from roughly USD 3.8 billion to approximately USD 6.7 billion in 2025 — and is forecast to expand at a compound annual growth rate (CAGR) of 11.85% through 2032, when the addressable market is expected to approach USD 14.7 billion. This trajectory creates both scale opportunities and strategic inflection points for device OEMs, chipset vendors, and systems integrators.

Bluetooth Audio Ic Market

Technology consolidation around Bluetooth LE Audio and LC3. Standards evolution (including Bluetooth 5.4) is driving product re-architecture: lower bit-rate codecs with equivalent or better perceived quality enable new battery/performance trade-offs and broaden the product set that can support premium audio features.

Bluetooth Audio Ic Market

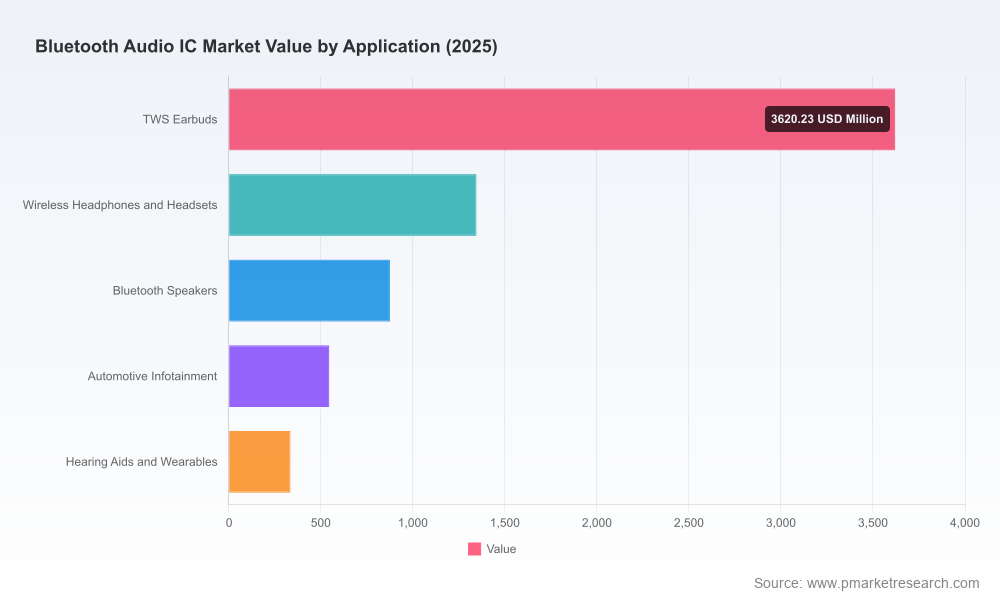

Commercial expansion is led by proliferation of hearables, TWS devices, and smart-speaker use cases — while automotive and industrial audio gateways are maturing as strategic adjacencies for chipset vendors and system integrators.

Bluetooth Audio Ic Market

Industry concentration is meaningful: the top three suppliers control a majority share of the market, and the top five account for over 70% — a structural fact that shapes negotiation dynamics, IP access, and channel availability.

Supply-chain and geopolitical frictions remain material. Controls on advanced manufacturing equipment, tariffs, and localized trade policies affect lead times, qualification cycles, and total cost of ownership for RF IC sourcing.

A validated market model with historical (2020–2025) and granular scenario projections (2026–2032) — designed for integration into corporate planning and board materials.

Supplier scorecards and risk heatmaps that combine technical capability, roadmap alignment (LE Audio, Matter, latency targets), capacity constraints, and geopolitical exposure — enabling rapid shortlisting for multi-year sourcing agreements.

Product roadmap guidance and architecture trade-off matrices (dual-mode vs. single-mode strategies, codec and DSP choices, MCU integration) for hearables, smart speakers, and automotive gateways.

Commercial playbooks covering pricing levers, licensing/royalty exposure, and channel models for white-label vs. co-engineered solutions.

M&A and partnership intelligence: prioritized targets and capabilities that deliver incremental differentiation or defensible cost positions, plus sensitivity analyses for synergies and integration risk.

Operational tools — procurement TCO templates, testing & qualification timelines, and a 12–24 month mitigation plan for semiconductor lead-time volatility.

The Bluetooth audio IC field features a mix of global tier‑1 silicon houses and highly focused regional specialists. Each archetype implies a different partnership model and risk profile:

Qualcomm (San Diego, USA): market and IP leader with broad product lines that include flagship SoCs tailored for premium TWS and spatial audio. Qualcomm’s roadmap and ecosystem partnerships (codecs, voice platforms, and mobile SoC integration) make it the default strategic partner for OEMs pursuing high-end differentiation and rapid global scale.

Realtek (Hsinchu, Taiwan): cost-performance specialist with strong position in highly price-sensitive consumer segments. Attractive for high-volume OEMs seeking integrated solutions with quick time-to-market.

Airoha Technology (Zhubei City, Taiwan): focused on premium TWS features (AI-assisted ANC, low-latency profiles). Best-suited for OEMs targeting premium audio experiences without full in-house ASIC development.

BES Technic (Shanghai, China): notable for high-fidelity audio and advanced ANC capabilities, and for aggressively sampling next-generation low-power devices — a strategic option where cost and local integration are priorities.

Nordic Semiconductor (Trondheim, Norway): strong in Bluetooth LE Audio and LC3 adoption, making it a preferred partner for hearables and connected audio accessories that prioritize low-power and modern standard compliance.

Espressif, Texas Instruments, STMicroelectronics: each brings differentiated value — Espressif for integrated IoT/audio combinations, TI for low-power audio processing and industrial-grade support, and ST for gateway and MCU-driven architectures.

Recent product and certification events (for example, new LE Audio SoCs and sampling of ultra-low-power chips) accelerate the pace at which OEMs must validate partners and lock software stacks, shortening typical qualification windows.

Standards: Adoption of LE Audio and mandated LC3 codec changes device-level trade-offs and interoperability testing scope. Early adoption benefits include differentiation and better power profiles; late adoption risks include obsolescence in premium segments.

Geopolitics & trade policy: Export controls and tariffs create measurable sourcing friction. Firms with single-region sourcing strategies or that rely on specific tool chains for RF IC fabrication face longer qualification cycles and potential cost escalation.

Manufacturing cadence: Foundry lead times for key process nodes have stabilized compared to 2021–2022 but remain material for planning; 40nm-class capacity and queue dynamics should be incorporated into multi-year procurement forecasts.

Product & roadmap: Define a LE Audio adoption timeline aligned to product tiering. For premium SKUs, prioritize dual-mode SoCs and spatial audio capabilities; for value tiers, optimize for single-mode LE implementations to preserve cost targets.

Sourcing: Move from single-supplier dependency toward a 2+1 model (two qualified suppliers and one development partner) to balance negotiating leverage with resilience. Include contract clauses for capacity reservation and price collars tied to key input indices.

IP & software: Lock core audio stacks and certification plans early. Budget for codec licensing and implement over-the-air upgradability to extend product lifecycles and capture post‑purchase feature revenue.

Supply-chain hedging: Build scenario-dependent buffer strategies (inventory, dual sourcing, strategic wafer locks) for 12–24 month disruption horizons, and de-risk critical toolchain exposure by maintaining alternate testing and packaging suppliers.

M&A & partnerships: Target acquisitions or JV structures that fill capability gaps (ANC DSPs, neural on-device processing, low-power front-end IP) rather than scale alone — speed to market on differentiated features is the primary value lever.

Hardware OEM: Use the supplier scorecard and TCO templates to recalibrate BOM targets for new product cycles and to implement an accelerated qualification timeline aligned with standards adoption.

Chipset vendor: Benchmark roadmap against peers and prioritize developer enablement (reference firmware, test kits) to shorten OEM time-to-integration and to increase sticky software revenue.

Private equity / corporate development: Apply the M&A playbook to identify bolt-on targets that deliver immediate product differentiation and to stress-test acquisition assumptions using our sensitivity scenarios.

This report is designed to be more than a static forecast. It equips executives with the analytical tools and scenario-tested guidance required to make procurement commitments, to prioritize R&D investments, and to manage geopolitical risk — all underpinned by a transparent market model and supplier intelligence. The market’s growth profile — near-term scale and medium-term acceleration — means decisions made in 2026 will materially influence unit economics, feature roadmaps, and channel strategies for the next five years.

This briefing intentionally previews strategic findings while withholding the full segmentation datasets, granular regional and application splits, and company-level shipment tables that underpin our recommendations. For access to the complete market model, supplier scorecards, interactive scenario tools, and the detailed annexes (including qualification timelines and cost build-ups), please consult the full report on the PW Consulting research portal.

For detailed analysis of this topic, please visit the official page:Bluetooth Audio Ic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com