Tissue Regeneration Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-16 10:47:01

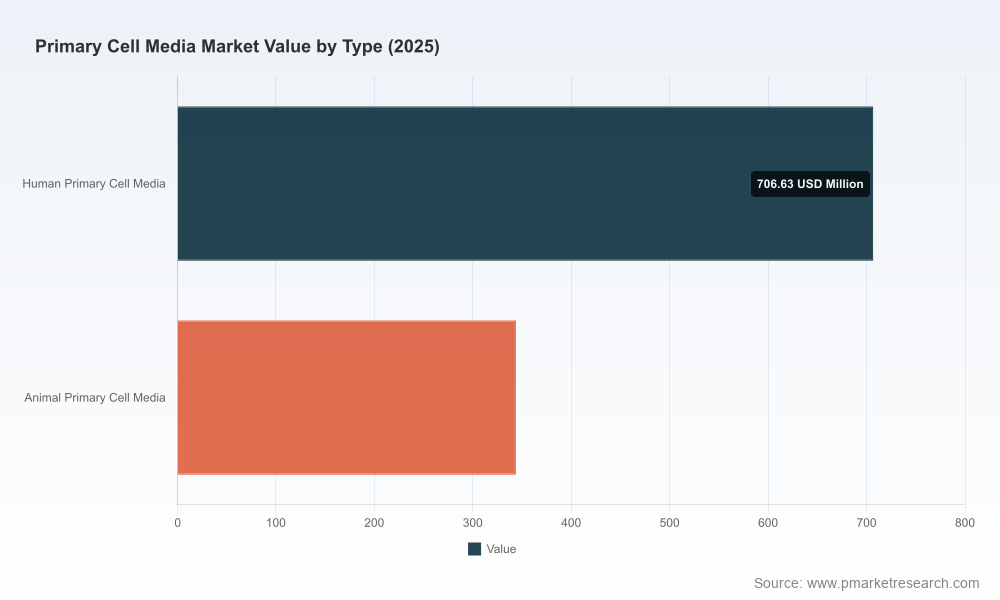

PW Consulting’s Primary Cell Media Market research provides a decisive strategic compass for life-science executives planning investments and operational moves in 2026. Built on a rigorous historical base (2020–2025) and a seven-year forecast window (2026–2032), the study quantifies a sustained, high-single-digit growth trajectory for the market and combines granular commercial intelligence with actionable playbooks. The headline: the global primary cell media market is projected to expand from approximately USD 1,050.5 million in 2025 to roughly USD 1,951.3 million by 2032, representing a compounded annual growth rate (CAGR) of about 9.25% over the forecast horizon.

Primary Cell Media Market

Timing and resource allocation: 2026 is a pivot year for many biopharma and reagent suppliers as R&D pipelines and cell-therapy translational programs move from bench to scaled preclinical validation. The report translates macro growth into near-term operational priorities, helping leaders prioritize R&D, manufacturing scale-up, and commercial investment in the most leverageable segments.

Primary Cell Media Market

Risk-informed sourcing: Raw-material volatility and quality consistency are now table stakes. Our analysis frames supplier sourcing strategies against raw-material risk scenarios, enabling procurement teams to build hedges and alternate-sourcing plans tailored to primary-cell sensitivities.

Primary Cell Media Market

Competitive positioning: With market concentration indicating that the largest three firms account for a plurality of market share while the top five consolidate a significant majority, there is clear room for both scale-driven incumbents and differentiated niche players. The report dissects competitive moats and commercial gaps that matter for 2026 M&A, partnership, and product roadmaps.

Our top-line modelling shows an expanding addressable market that nearly doubles over the 2025–2032 period. The 9.25% CAGR is not merely a function of base effects; it reflects durable demand drivers such as accelerating drug discovery throughput, the maturation of regenerative medicine platforms, and growing uptake of physiologically relevant primary-cell models in translational research. For executives this means predictable topline expansion but also escalating expectations around product qualification, batch-to-batch consistency, and regulatory traceability.

Translational R&D uptake: Primary-cell systems are increasingly preferred for candidate screening and safety assays because they reduce translational risk. This is shifting procurement away from commoditized reagents to higher-value, specification-driven media systems.

Therapeutic modality diversification: As cell therapies and organoid-based discovery progress, demand patterns are evolving toward tissue-specific and serum-reduced formulations that support complex phenotypes.

Quality and regulatory expectations: Laboratories and biotechs now demand reagent-level traceability and tight specification windows. The industry is responding with premium, well-documented media products and supply-chain transparency initiatives.

Raw-material and formulation evolution: Basal media formulations remain anchored in key amino acids, vitamins, salts and glucose, but supplementation strategies (growth factors, cytokines, plant-derived hydrolysates) are differentiating performance. Our report highlights sensitivity to raw-material source and provides recommended control limits for critical components.

The report is constructed to be directly usable by strategy, commercial, and R&D teams. Core deliverables include:

Forecast models (2026–2032) with scenario toggles — base, accelerated-adoption, and supply-disruption stress tests — enabling rapid what-if analysis for budgeting and capacity planning.

Buyer personas and procurement playbooks that translate scientific preferences into commercial terms and procurement KPIs (lead times, quality acceptance criteria, supplier scorecards).

Product positioning matrices and price-elasticity models to support launch decisions for differentiated media (e.g., chemically defined vs. serum-containing, tissue-specific formulations).

Supply-chain resilience toolkit including a raw-material risk register, critical-supplier dependency maps, and recommended dual-sourcing strategies for high-risk inputs.

Go-to-market (GTM) blueprints for incumbents and challengers — channel strategy, bundling approaches with consumables or assays, and partnership mapping with contract developers and translational CROs.

Regulatory readiness checklist oriented to research-use and translational supplies, focusing on documentation, lot-release testing, and claims management.

Executive dashboards and investment-grade appendices: transparent assumptions, data tables, and an audit trail of primary and secondary sources to support board-level decision-making.

The market is anchored by several globally recognised players offering a mix of branded media systems, specialized formulations, and integrated reagent portfolios. Our competitive assessment profiles strategic positioning and capability vectors rather than relying solely on revenue share.

Thermo Fisher Scientific — leverages a broad life-science portfolio and strong Gibco brand equity. Strengths: end-to-end product set, global commercial reach, and application support that de-risks adoption for large labs.

Merck KGaA (MilliporeSigma) — notable for integrated kits and supplement bundles enabling faster onboarding for primary-cell workflows. Strengths: deep reagent and kit integration for workflow reproducibility.

Lonza Group — positions itself at the interface of research and bioprocessing, with formulations and services tailored for translational pipelines. Strengths: tissue-focused product lines and process development expertise.

Corning Incorporated — combines media with specialized consumables, offering optimized environments for adherent primary cells. Strengths: product-system thinking that improves end-user outcomes.

Specialist and regional players (e.g., PromoCell, FUJIFILM Irvine Scientific, STEMCELL Technologies, Celprogen) — these firms compete on niche differentiation (tissue specificity, chemically defined formulations, stem-cell focus) and responsiveness to researcher needs.

Emerging and service-oriented vendors — firms such as Cell Applications, Cyagen, Creative Bioarray, Caisson Laboratories and BD Biosciences contribute to a vibrant supplier base with focused product lines and regional strengths.

Market concentration metrics underline a market with meaningful leadership: the top three players account for a substantial portion of sales, and the top five amplify that dominance further. This structure encourages strategic choices between scaling to compete on reach versus carving technical niches where differentiation yields price and margin premium.

Prioritise formulation differentiation: For product teams, investing in tissue-specific additives, serum-free chemistries, and validated accessory kits will be a primary route to defend pricing power.

Mitigate raw-material risk now: Procurement should operationalize the supplied raw-material risk register and pursue alternate suppliers or in-house qualification for hydrolysates and other variability-prone inputs.

Choose partnerships over one-off sales: Commercial leaders should pursue bundled offerings (media + matrix + assay) and embed application support to entrench customers and shorten conversion cycles.

Prepare for regulatory scrutiny: Firms targeting translational customers must adopt more stringent documentation and lot-testing protocols earlier in product life cycles.

Use M&A strategically: Acquiring niche formulation specialists or distribution adapters can be a faster route to cover white-space areas than organic development alone.

Immediate (0–6 months): Deploy the procurement playbook, run supplier stress tests, and initiate priority validation of second-source raw materials.

Medium-term (6–18 months): Launch a pilot premium formulation or a bundled application kit, backed by co-marketing with translational CROs; set measurable targets for customer adoption and margin uplift.

Strategic (18–36 months): Evaluate inorganic partnerships to gain formulation IP or specialized production capacity; align manufacturing investments to projected volume curves from our forecast scenarios.

In keeping with our “trailer” approach, this summary demonstrates the analytic depth and direct utility of the study without publishing the granular regional and application-level slices that many commercial and M&A decisions require. Key segmentation tables, regional demand curves, application-specific adoption timelines, and client-ready datasets are reserved for the full report and accompanying data workbook. These deliverables allow you to tailor the projections precisely to your product mix, geography, and go-to-market model.

For a copy of the full Primary Cell Media Market report, the forecast data workbook, and our custom advisory engagement options for 2026 execution, visit PW Consulting’s Primary Cell Media Market page or contact our industry practice. The full package includes the confidential segmentation matrices and the scenario models necessary to convert these insights into executable plans.

For detailed analysis of this topic, please visit the official page:Primary Cell Media Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com