Digital Oilfield Market Growth with Industrial IoT Applications

Other |

2026-04-07 06:18:51

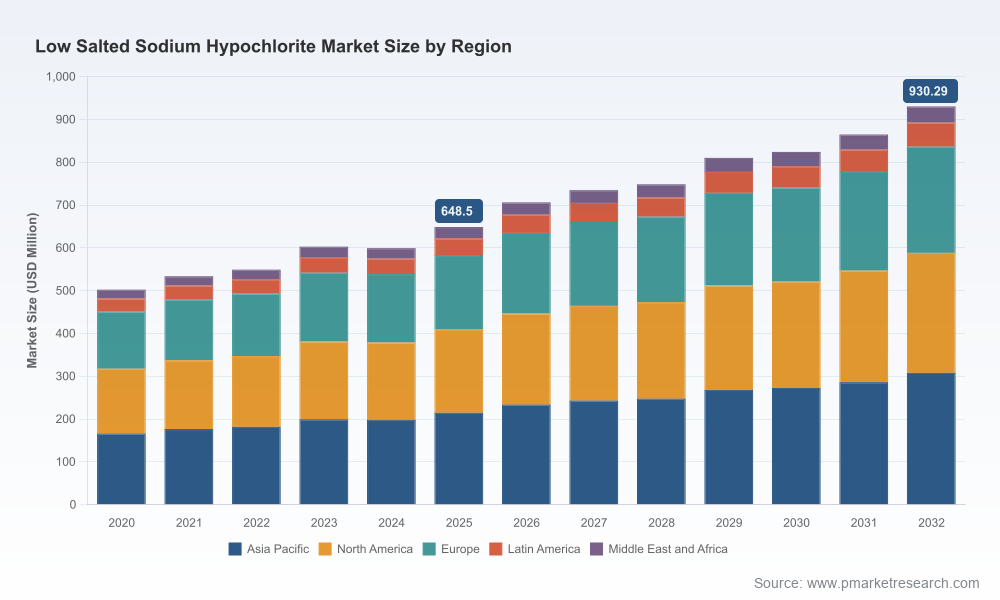

As utilities, industrial end-users and specialty chemical producers set budgets and capital plans for 2026, the choice of disinfectants and oxidation chemistries is shifting from commodity-driven sourcing to value-led procurement. PW Consulting’s new market study — base year 2025, historical review 2020–2025, forecast 2026–2032 — provides the actionable intelligence executives need to make those decisions with confidence. Our analysis shows the global low salted sodium hypochlorite market expanded from roughly USD 502 million in 2020 to about USD 648.5 million in 2025 and is forecast to continue growing at a compound annual growth rate of 5.29% through 2032, when market size is projected to approach USD 930 million. This advisory brief outlines why the 2026 planning cycle is pivotal and how the report’s practical tools translate into boardroom impact.

Low Salted Sodium Hypochlorite Market

The market’s steady mid-single-digit CAGR reflects a combination of technical substitution (higher-strength, low-impurity grades replacing older formulations), operational optimization at municipal and industrial treatment plants, and rising adoption of on-site generation where economics allow. Competitive structure remains moderately concentrated: the top three suppliers account for a meaningful share of supply, and the top five approach half of the market by revenue, signalling both opportunity and entry barriers for new players.

Low Salted Sodium Hypochlorite Market

From a demand standpoint, utilities and large industrial customers are prioritizing product purity, stability and logistics footprint; these priorities are reshaping buying specifications and procurement cycles.

Low Salted Sodium Hypochlorite Market

On the supply side, investment in production processes that reduce residual salts, chlorate/perchlorate formation and trace metals is differentiating incumbents and redefining total cost of ownership for buyers.

Operational economics: higher‑strength, low‑salt formulations demonstrably reduce consumption and corrosive wear on assets. Recent field validations have shown substantial usage reductions in wastewater and potable-treatment settings, shifting conversations from unit price to cost-per-effective-dose.

Regulatory and certification dynamics: proven low‑impurity grades are increasingly meeting or aligning to national water chemistry certifications and product stewardship standards, affecting municipal procurement requirements and liability exposure.

Supply resilience and concentration risk: with a moderate market concentration among leading producers, buyers are re-evaluating supplier diversification, strategic inventory policies and strategic partnerships to de‑risk critical supply chains ahead of capital cycles.

This study is designed as an operator-to-board playbook. Beyond market sizing and trend narratives, it includes scenario-based forecasts, supplier scorecards, and implementation-ready materials that decision-makers can use directly in procurement and investment discussions. Key deliverables include:

Executive decision matrices tying product grade (purity, strength, residual salts) to treatment outcomes, equipment wear, and lifecycle operating costs.

CapEx/Opex modelling templates that quantify the cross-over economics of switching to higher‑strength low‑salt products versus on‑site generation systems.

Supplier verification checklists, pilot design templates, and standardized test protocols to accelerate validation at municipal or industrial sites.

Regulatory and certification compendium summarizing key regional certifications and handling requirements pertinent to low‑impurity hypochlorite grades.

Go‑to‑market playbooks for producers and distributors with channel segmentation, pricing strategy windows, and partnership frameworks to expand into municipal and food/pharma applications.

Risk matrices and mitigation roadmaps for raw material volatility, logistics disruptions and regulatory shifts — calibrated to a range of macroeconomic scenarios through 2032.

Recent industry developments underscore the practical benefits of the new generation of low‑salt products. Notably, a 15.5 wt% high‑strength low‑salt sodium hypochlorite trial demonstrated significant reductions in consumption and more consistent performance compared to standard-strength alternatives at a municipal wastewater treatment facility. Leading producers are also formalizing stewardship and handling guidance for concentrated, low‑impurity products — updates that reduce implementation friction for large buyers.

Technical routes such as staged chlorination combined with salt-removal processes can produce very high‑strength feeds that, when formulated and diluted for distribution, deliver substantially longer shelf life and lower degradation rates than conventional product. In parallel, on‑site generation technologies continue to evolve, offering an attractive alternative where transport, storage risk, or site footprint favour decentralized production.

The report profiles the established and emerging suppliers shaping the market. Highlights include concentrated, high‑purity manufacturers and vertically integrated chlor‑alkali players with proprietary processing capabilities. Representative company profiles (summarized) include:

Private chlor‑alkali producer based in New Jersey with regional plants in the U.S. Northeast. Markets a concentrated, ultra‑pure low‑salt bleach tailored for municipal disinfection and long‑term operational stability in water treatment settings. Noted for close customer relationships and long-term supply reliability.

California‑headquartered specialty producer known for premium, high‑strength low‑salt formulations. Recent field validation showed material usage reductions and extended stability versus conventional grades, supporting total cost of ownership claims for municipal and industrial buyers.

Major integrated chlor‑alkali manufacturer with broad North American footprint. Offers super‑concentrated low‑salt hypochlorite and has issued updated product stewardship guidance to support safe handling and uptake of higher‑concentration grades among large users.

Japanese specialty chemicals firm offering certified low‑impurity hypochlorite grades that meet national water supply standards. Strength in regulatory alignment and specialty markets such as food production and tap‑water sterilization.

Japanese producer with branded low‑salt hypochlorite formulations focused on public water supply and industrial bleaching applications, emphasizing low halogen impurity profiles.

These suppliers illustrate two strategic models: (1) integrated large‑scale producers advancing proprietary purification and handling protocols; and (2) specialty vendors focusing on product differentiation through certification, application support and local service. Buyers should map supplier capability profiles against internal risk appetites and operational constraints when setting supplier selection criteria.

Reframe procurement KPIs: move from unit price to cost-per-effective-dose and asset‑lifecycle impact. Include pilot outcomes and equipment wear projections in procurement scorecards.

Design short pilots before large rollouts: use standardized test templates to validate claimed consumption reductions and stability under local operating conditions.

Adopt a hybrid supply strategy: combine contracted deliveries of higher‑strength low‑salt products with selective on‑site generation where site economics and risk profiles justify the capital outlay.

Prioritise suppliers with documented stewardship and certification alignment, particularly for municipal and food/pharma applications where liability and compliance risk is higher.

Invest in supplier development: for producers, prioritize R&D and process upgrades that reduce chlorate/perchlorate formation and trace metal content; distributors should train field service teams to manage higher‑concentration product handling.

The report is structured to move teams from insight to action within a single planning cycle. Our vendor scorecards, pilot templates and economic models are ready to be inserted into procurement RFPs, CAPEX proposals and risk assessments. For executives preparing 2026 budgets, the research translates market forecasts and technical dynamics into clear investment trade-offs and near‑term capture strategies.

We maintain the full set of regional, product‑grade and application‑level granularity in the full report — the segmentation tables, per‑region demand drivers, and supplier share tables are intentionally retained in the core document to preserve the strategic detail procurement and business‑development teams require. This brief is a trailer: it outlines the shape of opportunity, demonstrates analytical depth, and invites stakeholders to engage the full study to access the complete datasets and executable templates.

If your 2026 plans include reassessing disinfectant portfolios, upgrading production/process controls, or piloting alternative supply models, PW Consulting’s Low Salted Sodium Hypochlorite Market report is designed to accelerate those initiatives. Contact our advisory team to schedule a tailored briefing and obtain the full report with regional breakdowns, supplier share tables and the implementation playbooks needed to act decisively in 2026.

For detailed analysis of this topic, please visit the official page:Low Salted Sodium Hypochlorite Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com