When Do You Need Wisdom Tooth Extraction in Dubai?

Health |

2026-06-19 05:25:01

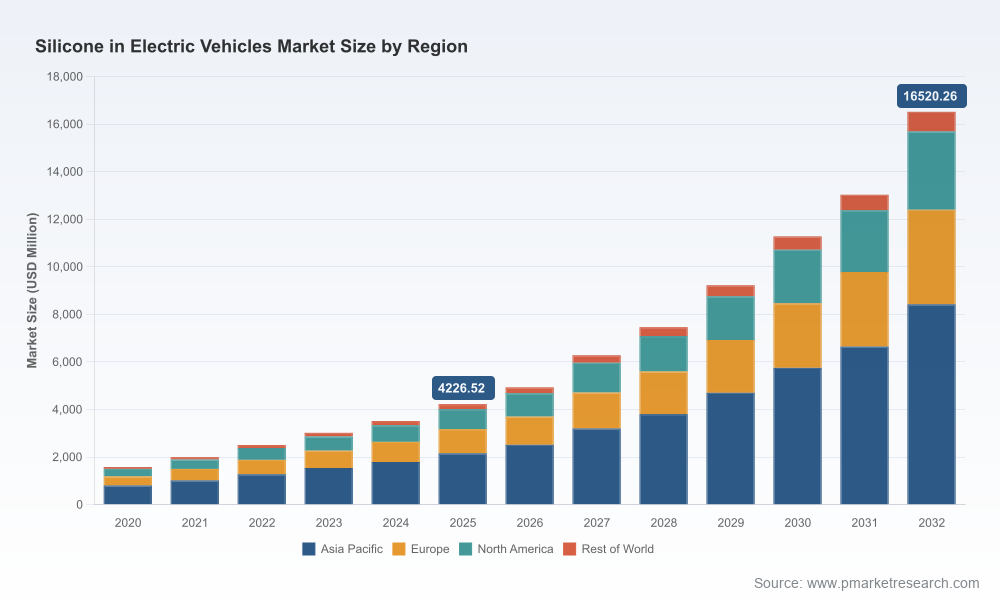

PW Consulting’s latest market study on Silicone in Electric Vehicles provides a timely, decision-grade intelligence package for executives shaping 2026 strategies. The sector has moved from niche enabling chemistries to mission-critical components across battery systems, power electronics, motors and charging infrastructure. Our analysis shows the market expanding rapidly: total industry revenues rose from roughly USD 1.58 billion in 2020 to about USD 4.23 billion in 2025, and are projected to accelerate to approximately USD 16.52 billion by 2032 under a 21.5% CAGR for the 2026–2032 forecast window. This brief distills the levers that will matter to commercial, procurement and technology leaders in the year ahead — while preserving the granular forecasts and segment-level data for subscribers to the full report.

Silicone In Electric Vehicles Market

Strategic timing: With seven-year projections indicating multi-fold market growth, 2026 is the inflection point for scaling production, locking supply and prioritizing R&D investments. Companies that move from pilot to industrialized silicone solutions this year will capture structural share as OEMs accelerate EV content.

Silicone In Electric Vehicles Market

Margin management: Raw-material and feedstock volatility observed in 2025–2026 compresses margins for unhedged suppliers and converters. Procurement and pricing strategies executed early in 2026 will determine competitiveness through 2027–2028.

Silicone In Electric Vehicles Market

Regulatory compliance as a market gate: New safety rules and battery regulations implemented since 2025 increase demand for flame-retardant and qualification-ready silicones. Compliance-oriented product roadmaps and certification pathways must be integrated into 2026 product development cycles.

M&A and partnerships: Given a market that is consolidating around a handful of large players while specialty innovators proliferate, 2026 is prime for targeted bolt-ons, joint development agreements, and offtake partnerships to secure technical differentiation and capacity.

Electrification demand surge: Global EV volumes and the ensuing electronics and thermal-management requirements are primary demand engines. As EV sales approach mid-double-digit millions annually, demand for silicone-based thermal interface materials, encapsulants and adhesives has grown materially (notably a double-digit year-on-year uplift for thermal management solutions reported through 2024–2025).

Regulatory tailwinds: Safety-focused legislation has elevated silicones from “preferred” to “required” in several battery applications where flame retardancy and thermal stability are mandated. This regulatory change reallocates specification power to players who can demonstrate certified, scalable formulations.

Input-cost pressure: In 2025–early 2026, silicone rubber and polysiloxane feedstock costs experienced notable increases driven by robust demand and energy-related supply constraints. These dynamics are creating near-term procurement risk but also opportunity for vertically integrated suppliers and buyers who pursue hedging and long-term supply agreements.

Supply concentration and competition: Market concentration metrics indicate that a limited group of global chemical majors and specialist silicone providers account for a substantial portion of market capacity. This creates both supply resilience from incumbent technical capabilities and openings for agile niche players with differentiated chemistries or application know-how.

The competitive map is a blend of global chemical majors and specialized silicone firms. PW Consulting’s proprietary benchmarking shows incumbents pursuing three distinct playbooks: (1) technology-led product differentiation for thermal and electrical insulation, (2) capacity expansion and vertical integration to manage feedstock exposure, and (3) customer-intimate co-development with OEMs and tier-one suppliers.

Dow (Midland, Michigan, USA) — Focus: encapsulants, thermal interface materials and sealants for batteries and power electronics. Recent product showcases at major battery industry trade events underscore Dow’s emphasis on next-generation battery encapsulation systems designed for manufacturability and safety compliance.

Wacker Chemie (Munich, Germany) — Focus: silicone gels, elastomers and adhesives for potting, insulation and vibration damping. Wacker’s product launches in 2025 signaled a push into higher-performance gel systems tailored for power electronics insulation and long-term reliability under thermal cycling.

Momentive Performance Materials (Waterford, New York, USA) — Focus: thermal management gap fillers and protective coatings. Momentive’s trade-show activity shows a strategy centered on tight integration between material performance and inverter-level thermal architectures.

Shin-Etsu Chemical (Tokyo, Japan) — Focus: silicone rubbers, fluids and greases for seals, gaskets and motor lubricants. Shin-Etsu leverages scale in base chemistries to provide qualification-ready elastomers to automotive OEMs.

Elkem Silicones (Oslo, Norway) — Focus: encapsulation, EMI shielding and structural adhesives. Elkem’s portfolio emphasizes multifunctional silicones that combine thermal, mechanical and electrical protection — attractive for integrated battery modules.

KCC Corporation / Kumho Chemical (Seoul, South Korea) — Focus: encapsulants and thermal pads designed for high-safety, high-efficiency battery pack layouts. KCC targets close collaborations with regional OEMs to shorten qualification cycles.

Recent product launches and trade-show demonstrations from these companies highlight a competitive environment where technical differentiation and speed-to-qualification are decisive. PW Consulting’s full report contains supplier scorecards, technology-readiness assessments and engagement roadmaps for each of these firms.

Forward-looking market model with annual revenues from 2020 through 2032, scenario runs and sensitivity to raw-material price and EV adoption paths.

Competitive scorecards with go-to-market strategies, technology strengths, capacity footprints and supplier risk ratings for major players.

Supply-chain risk maps and stress-test scenarios (feedstock shocks, energy disruptions, regulatory acceleration) with quantified impact ranges and mitigation playbooks.

Product-application playbooks: thermal management, power electronics, motor systems, charging infrastructure and interior/exterior adhesive use cases — each with qualification requirements and adoption timelines.

Commercial levers for 2026: procurement contracting templates, price-indexation approaches, and regional sourcing strategies designed to protect gross margins during input volatility.

An M&A and partnership compass highlighting white-space niches, integration risks and target criteria for bolt-on acquisitions or strategic alliances.

Prioritize thermal-management platforms that are qualification-ready: target modular solutions that reduce integration lead time with OEMs and shorten validation cycles.

Lock in feedstock through diversified, multi-year contracts and explore partial vertical integration where scale justifies it — especially for manufacturers sensitive to polysiloxane price oscillations.

Embed regulatory compliance early: align formulation and testing roadmaps with current battery safety standards and anticipated tightening of requirements in core markets.

Use strategic partnerships to accelerate market access: co-development agreements with tier-one suppliers and targeted pilot projects with OEMs can convert product demonstrations into production contracts within 12–18 months.

Hedge through product differentiation: invest in multifunctional silicones that combine thermal, mechanical and electrical benefits to command premium positioning and protect margins.

Monitor consolidation opportunities: acquisitive M&A can secure capacity and IP, but careful integration planning is necessary given the specialized manufacturing and qualification timelines.

Prepare flexible manufacturing footprints: design capacity decisions to allow rapid reallocation between battery, power electronics and motor-related silicones as customer demand mixes evolve.

For commercial, product and procurement leaders, the actionable takeaway is clear: 2026 should be treated as a strategic investment year. Use the first half of 2026 to finalize supplier contracts, accelerate product qualification with top-tier OEM programs, and set up scenario-based hedge strategies for feedstock exposure. For corporate development teams, maintain active target screens for niche technology providers and specialty converters whose capabilities can be integrated into broader value chains.

PW Consulting’s full Silicone in Electric Vehicles Market report contains the proprietary models, segment-level forecasts, supplier benchmarking and tactical templates referenced here. To access the detailed breakdowns, scenario files and supplier matrices that we intentionally withhold from this public briefing, please visit PW Consulting’s report page or contact our industry desk for a tailored briefing and data license.

For detailed analysis of this topic, please visit the official page:Silicone In Electric Vehicles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com