Biotechnology Market Size, Share, Growth Drivers, and Forecast 2034

Other |

2026-06-23 13:58:18

PW Consulting’s latest Audit Management Software Systems Market report (base year 2025; forecast 2026–2032) shows a market in sustained expansion, driven by accelerating digital transformation in GRC (governance, risk and compliance) and a rapid adoption of AI-enabled automation. The global market rose from roughly USD 1.64 billion in 2020 to USD 2.8 billion in 2025 and is forecast to continue expanding at a compound annual growth rate (CAGR) of 11.2% across the forecast window, reaching an estimated USD 5.9 billion by 2032. For executive teams planning budgets and capability roadmaps in 2026, this report translates those macro trajectories into immediately actionable strategy.

Audit Management Software Systems Market

Regulatory inflection points are reshaping procurement and implementation. The full enforcement of the EU AI Act in 2026 and a proliferation of U.S. state privacy statutes mean audit platforms must deliver auditable AI governance and robust data-mapping capabilities out of the box.

Audit Management Software Systems Market

Operational pressure from auditor shortages and rising labor costs is forcing organizations to shift from manual evidence collection and spreadsheet-based workflows to automated, audit-ready pipelines.

Audit Management Software Systems Market

Enterprise architectures are consolidating: buyers expect audit tools to be interoperable with finance, ERP, and broader GRC stacks while supporting hybrid deployment models and subscription economics that lower TCO.

Vendor ecosystems are evolving: incumbents are embedding AI and analytics at the workflow level, while agile mid-market vendors compete with no-code platforms and rapid integrations—creating both competitive risk and opportunity for strategic sourcing.

Market sizing and validated forecasts (2020–2032) to support multi-year investment planning and scenario modeling.

Vendor landscape and competitive positioning, including capability matrices that evaluate audit planning, execution, evidence management, AI governance, and integration maturity.

Go-to-market and procurement playbooks: RFP templates, evaluation scorecards, total cost of ownership (TCO) models, and contracting levers specific to SaaS subscription models.

Implementation and change-management blueprints: phased deployment plans, data-migration checklists, KPI definitions for continuous assurance, and auditor enablement guides.

Risk-impact assessments: regulatory compliance roadmaps for AI and privacy laws, plus mitigation strategies for vendor lock-in, data residency, and audit trail requirements.

Industry use cases and ROI exemplars that quantify time-to-value for typical audit and compliance processes.

Note: this release intentionally presents high-level market dynamics and strategic findings. Detailed segment-by-segment revenue tables, regional splits, and proprietary vendor scorecards are available in the full report on our website.

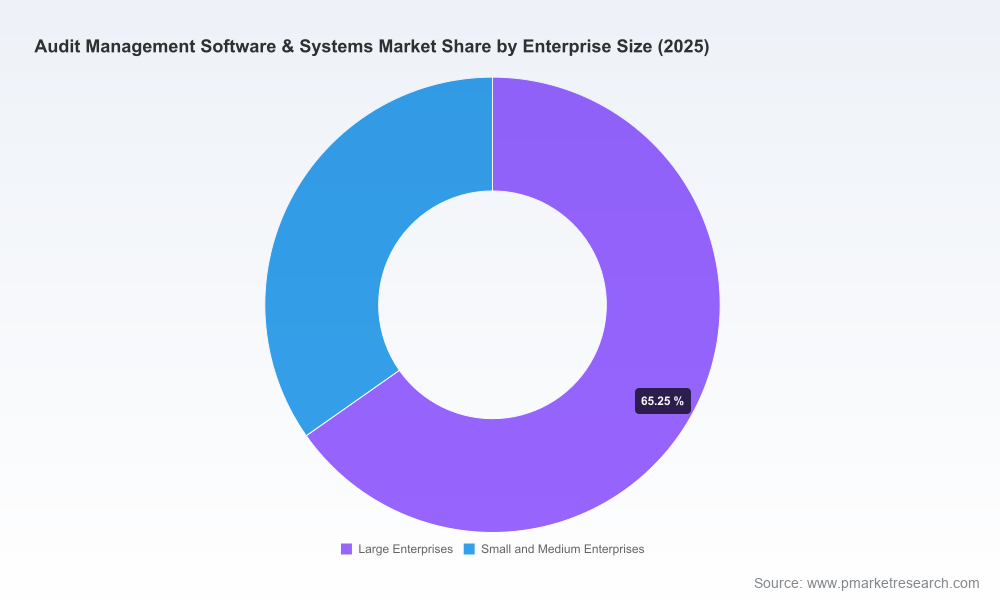

The market exhibits moderate concentration: the top three vendors account for roughly 35.5% of market revenue while the top five capture about 48.2%. That structure creates a duopoly of influence among leading platforms and meaningful space for specialist and mid-market challengers to differentiate.

AuditBoard (Optro) — Positioned as a connected risk platform, AuditBoard’s strength is in integrated workflows for audit, risk, compliance and ESG supported by AI features that promote unified GRC execution. Its value proposition suits organizations prioritizing connected risk data models.

Workiva — Known for cloud-native integrated reporting and strong controls around finance and sustainability reporting, Workiva’s governed-AI approach addresses auditors’ demands for explainability and traceability in financial disclosure workflows.

Diligent — With Diligent One, the company pushes a consolidated governance platform that tightly links board governance, risk committees, and audit functions—an appealing option for organizations seeking a single-pane governance view.

Wolters Kluwer (TeamMate) — TeamMate+ remains a default for internal audit teams with deep planning, execution and issue-tracking capabilities; it is often favored where audit methodology and firm-wide consistency are priorities.

MetricStream — Strong in enterprise GRC, MetricStream differentiates on risk-based auditing and compliance workflows, making it suitable for complex, regulated environments with cross-functional risk requirements.

Onspring — A flexible no-code GRC platform that has rapidly extended into embedded AI and data privacy management products; Onspring’s speed-to-configure and recent product launches make it an attractive pick for resource-constrained GRC teams seeking rapid automation.

SAP — SAP Audit Management appeals to large SAP-centric estates where integration into ERP and financial systems and mobile-enabled field auditing are critical. SAP’s ecosystem advantage enables seamless data flows for continuous auditing use cases.

Recent market activity underscores two themes: (1) major players are building or partnering to add AI-powered evidence extraction and automated audit workflows (for example, strategic AI partnerships announced by major information providers), and (2) smaller, nimble vendors are shipping purpose-built capabilities such as embedded AI suites and data privacy modules that accelerate time-to-value for buyers.

Chief Audit Executive (CAE): Prioritize platforms that provide end-to-end audit lifecycle support, demonstrable AI governance, and out-of-the-box evidence lineage. Run proof-of-concepts focused on a high-impact audit cycle to validate automation benefits before enterprise rollout.

CFO / Head of Finance: Align procurement with finance-system integration requirements and insist on scenario-based TCO comparisons that include transition and ongoing audit labor savings. Use subscription and consumption metrics to negotiate performance-based pricing.

Chief Information Officer (CIO): Insist on modular APIs, robust identity and access controls, and data residency assurances that meet evolving privacy laws. Build a staged integration plan to minimize legacy-system disruption.

Head of Risk & Compliance: Map regulatory obligations (e.g., EU AI Act, state privacy laws) to vendor capabilities as pass/fail criteria. Require vendors to supply AI model documentation, bias testing outputs, and explainability tools where applicable.

AI governance risk: Mitigation — require model provenance, logging, and human-in-the-loop controls; include contractual audit rights for AI behavior and outputs.

Data privacy and residency: Mitigation — mandate data mapping, encryption-at-rest/in-transit, and clear subprocessor lists in SLAs; seek regional deployment options where necessary.

Integration debt and lock-in: Mitigation — favor pre-built connectors and open APIs; stage deployments to allow parallel runs during cutover; include exit assistance clauses and data export guarantees.

Skill gaps and adoption: Mitigation — invest in auditor upskilling, appoint product champions, and measure adoption using process KPIs tied to savings and quality improvements.

Use the report’s forecast scenarios to size investments and create conservative/accelerated spend plans that align with broader digital transformation budgets.

Apply the vendor scorecards and the provided RFP templates to shorten procurement cycles and capture negotiation leverage based on measurable feature- and risk-based criteria.

Embed the implementation playbook and ROI templates into your 12–24 month deployment plan to secure internal sponsorship and quantify expected cost and time savings.

For 2026 decision-makers, the choice of audit management system is no longer just a technology decision — it is a strategic lever that affects compliance posture, audit productivity, and enterprise risk visibility. PW Consulting’s full Audit Management Software Systems Market report translates the market’s robust growth trajectory (11.2% CAGR) and competitive dynamics into concrete actions: vendor selection criteria, regulatory roadmaps, and implementation playbooks designed to de-risk deployments and accelerate value realization.

To access the full dataset, detailed segmentation, vendor scorecards, and bespoke advisory options, visit our research portal on the PW Consulting website. The full report contains the proprietary tables and granular analysis that enterprise procurement and audit leaders will need to finalize 2026 budgets and vendor shortlists.

For detailed analysis of this topic, please visit the official page:Audit Management Software Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com