Contact Lens Market to Reach US$ 12.6 Billion by 2031 Amid Rising Demand for Vision Correction Solutions

Other |

2026-06-23 10:45:42

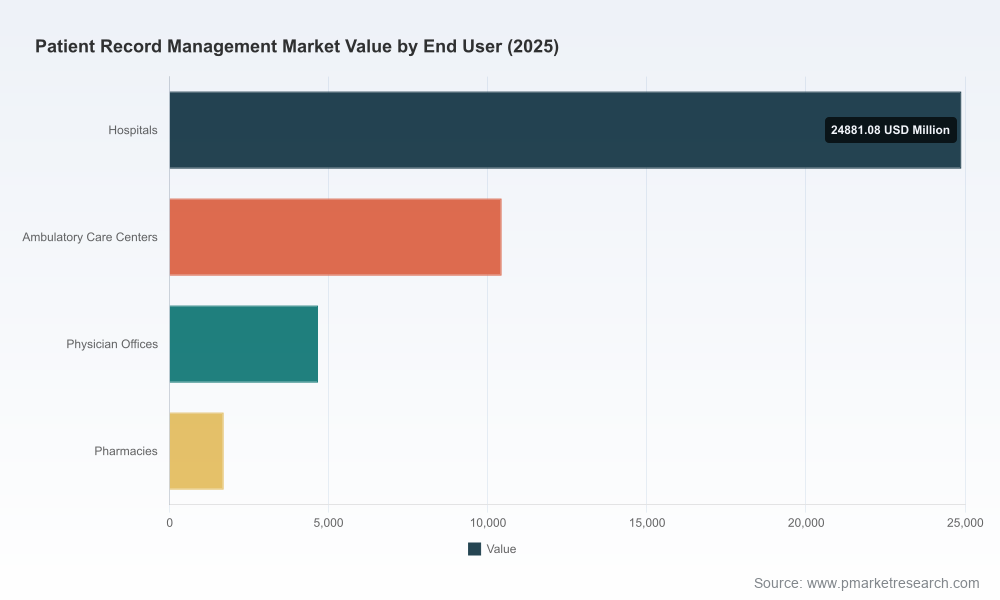

PW Consulting’s latest Patient Record Management Market study—anchored on historical performance from 2020–2025 and a forward-looking forecast for 2026–2032—presents a strategic view designed for executives making investment, procurement, and partnership decisions in 2026. The global market is substantial and expanding: our base-year assessment places the market at approximately USD 41.7 billion in 2025, with a projected compound annual growth rate (CAGR) of 6.41% through the 2026–2032 forecast window, culminating in an anticipated market size of roughly USD 64.4 billion by 2032. These macro metrics reflect structural demand for interoperable, secure, and AI-enabled patient record solutions across care settings.

Patient Record Management Market

Timing and capital allocation: 2026 is a tipping point where buyers must decide between incremental upgrades and platform transformations. The market trajectory indicates meaningful returns for targeted cloud migrations and data modernization programs.

Patient Record Management Market

Vendor strategy: consolidation dynamics are real—the leading vendors capture a material share of the market—making vendor selection and contract architecture top priorities to protect margins and continuity of care.

Patient Record Management Market

Regulatory and interoperability risk: incumbents and challengers alike face heightened compliance expectations and interoperability demands that will materially affect implementation timelines and total cost of ownership (TCO).

Regulation and compliance. Ongoing mandates (including HITECH/HIPAA enforcement) continue to set baseline security and privacy requirements; ONC’s information-blocking and certification frameworks remain central to procurement strategy (Office of the National Coordinator for Health IT).

Interoperability standards. The maturation of HL7 FHIR (most recently Release 5) is driving API-first architectures and creating a new interoperability baseline for patient record exchange (HL7 International).

Reimbursement and incentives. U.S. programs that reward certified EHR usage continue to influence adoption timing and feature prioritization—affecting both suppliers’ roadmaps and provider upgrade cycles (Centers for Medicare & Medicaid Services).

Technology acceleration. Expect AI-driven summarization, real-time analytics, and integration with wearables and remote monitoring to be differentiators. Recent vendor product updates demonstrate the trend toward embedded AI for clinical workflows.

Privacy across jurisdictions. Stringent data protection regimes—most notably GDPR requirements for processing health data in EU markets—remain a gating factor for multi-jurisdictional deployments.

The competitive environment combines a set of large, entrenched platform providers with specialized vendors serving niche practice types. Market concentration is meaningful: the top three vendors account for roughly 42% of the market, and the top five cover nearly 58%—a profile that creates both advantages (stability, integration breadth) and negotiation challenges (pricing pressure, slower innovation cycles in some segments).

Epic Systems Corporation — Recognized for large health system deployments and deep clinical functionality. Recent product enhancements toward AI-powered patient record summarization reinforce Epic’s strategy of embedding advanced clinical decision support and interoperability capabilities across enterprise deployments (Epic Systems, October 2025).

Oracle Cerner — Positioned to scale cloud-native analytics through hyperscaler partnerships; its recent collaboration with Google Cloud signals an emphasis on advanced ML-driven population health and record analytics (Oracle press release, September 2025).

Athenahealth — A major cloud-first competitor; recent ONC certification milestones (June 2025) strengthen its value proposition for providers seeking certified, cloud-based platforms with rapid feature delivery.

Allscripts, NextGen, eClinicalWorks, GE HealthCare — These vendors compete across ambulatory, specialty, and imaging-integrated segments; their differentiated go-to-market models (telehealth integration, mobile access, specialty workflows) matter when matching platform capabilities to clinical and operational priorities.

Product differentiation via AI: Epic’s October 2025 enhancements introduce automated summarization capabilities that reduce clinician documentation time and improve record usability (Epic Systems official announcement).

Hyperscaler partnerships: Oracle Cerner’s September 2025 partnership with Google Cloud accelerates large-scale analytics workloads and shortens time-to-insight for record-based initiatives (Oracle press release).

Certification as a competitive lever: Athenahealth’s ONC certification (June 2025) is illustrative of how regulatory compliance can be converted into a procurement advantage for cloud vendors.

This study goes beyond headline forecasting. It provides a pragmatic toolset for decision-makers preparing 2026 strategies:

Actionable executive dashboards that map scenarios (conservative, base, accelerated) against capital and operating budgets for 2026–2028.

Vendor scorecards and selection matrices tied to clinical workflows, interoperability readiness (FHIR Release 5), and AI capabilities—designed to shorten RFP cycles.

Implementation playbooks that align migration pathways (lift-and-shift vs phased modernization) with risk mitigations for data portability and downtime.

TCO and ROI models, including sensitivity analyses for cloud vs on-prem architectures and projected maintenance/licensing trajectories.

Regulatory compliance checklists and a jurisdictional risk matrix (GDPR, HIPAA, ONC requirements) for multinational deployments.

M&A and partnership playbooks that identify value capture levers in consolidation scenarios and hyperscaler collaborations.

Prioritize interoperability: Require FHIR Release 5 compatibility as a baseline in procurement documents. Interoperability readiness will directly affect integration costs and speed to clinical value.

Adopt an AI governance framework: As vendors ship AI-enabled record capabilities, organizations must define validation, monitoring, and clinician feedback loops before broad rollout.

Design hybrid migration paths: Capitalize on cloud economics where appropriate, but plan for phased migration to manage clinical risk and contractual exposure.

Renegotiate supplier economics with market context: Use the current concentration dynamics and vendor roadmaps to secure outcome-based SLAs and shared-risk pricing where possible.

Protect cross-border data flows: Incorporate privacy-by-design clauses and data localization strategies to comply with GDPR and other regional protections.

Consistent with the “teaser” principle used in this briefing, we present the macro market scale, growth trajectory, and strategic implications to support immediate decision-making. Detailed regional and application split figures, granular vendor market shares, and full pricing models are intentionally reserved for the full report to preserve competitive value for subscribers and clients. If you require that level of granularity for negotiation or investment due diligence, the complete dataset and appendices are available in the paid report and through our custom advisory engagements.

For procurement teams, CIOs, digital health investors, and strategy groups planning 2026 initiatives, the PW Consulting Patient Record Management Market report is designed as both a reference and a playbook. Download the full report or request a tailored executive briefing to receive:

The complete segmentation tables and interactive models underpinning our forecasts.

Vendor benchmarking with raw scorecards and procurement-ready RFP language.

Custom scenario modeling aligned to your enterprise’s revenue, patient volumes, and regulatory footprint.

Contact PW Consulting to schedule a briefing and obtain the full dataset and supporting materials that will equip your organization to act with confidence in 2026.

For detailed analysis of this topic, please visit the official page:Patient Record Management Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com