Drug Delivery Market Size, Share, Trends, and Industry Forecast by 2032

Other |

2026-06-04 07:52:35

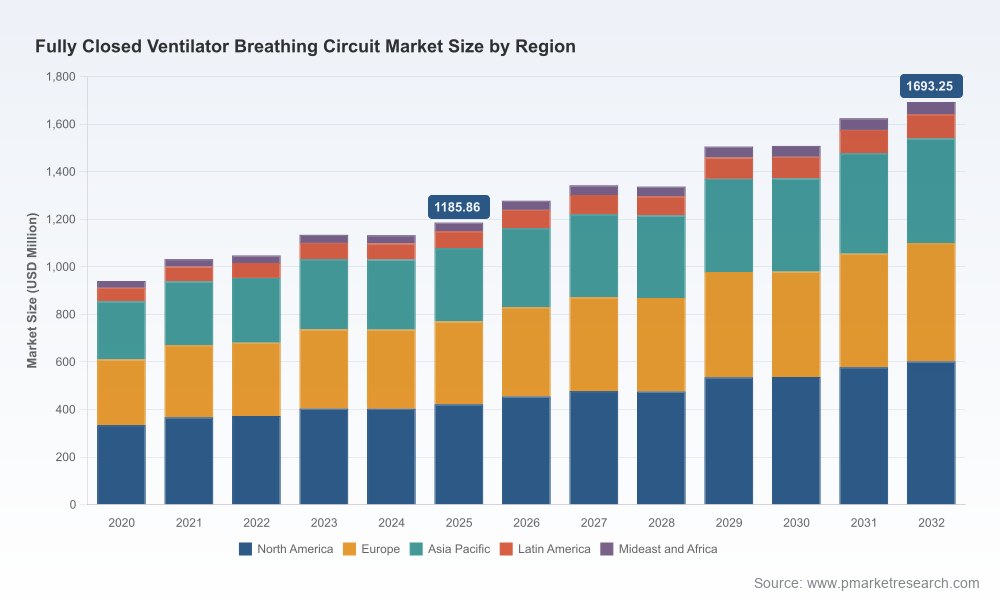

PW Consulting’s latest market research on the Fully Closed Ventilator Breathing Circuit market synthesizes seven years of historical data (2020–2025) and an actionable forecast window (2026–2032). At the aggregate level the market reached a meaningful scale in the base year (2025) and is projected to grow at a compound annual growth rate (CAGR) of 5.22% across the forecast period, with our long‑range scenario projecting continued expansion through 2032. For executives preparing 2026 budgets and three‑to‑five‑year roadmaps, this report translates industry-level momentum into executable commercial strategies without exposing sensitive SKU- or region-level intelligence that is reserved for report subscribers.

Fully Closed Ventilator Breathing Circuit Market

Investment prioritization: Identify which product and technology investments are likely to deliver the best risk-adjusted returns within a moderate-growth environment (approx. 5% CAGR).

Fully Closed Ventilator Breathing Circuit Market

M&A and partnership screening: Define acquisition targets and OEM partners by technology adjacency, installed-base synergies, and aftermarket revenue potential.

Fully Closed Ventilator Breathing Circuit Market

Regulatory and reimbursement roadmaps: Anticipate conformity and coding pressures that will shape product design, labeling, and commercial pricing strategies in major markets.

Manufacturing and sourcing planning: Align capacity expansion and supplier contracts to a predictable growth trajectory and to mitigate single‑source risk for critical subcomponents.

Go‑to‑market optimization: Tailor channel, pricing, and clinical-engagement programs to shorten procurement cycles and accelerate hospital adoption.

Transparent methodology: Replicable topline market model covering 2020–2025 historicals and a base-year of 2025, plus scenario- and sensitivity-based forecasts for 2026–2032 (currency: USD, revenue unit: Million).

Actionable segmentation framework: Multi-dimensional segmentation (product type, application, geography) mapped to buying behaviors, procurement levers, and clinical requirements. (Note: detailed, downloadable segmentation tables and SKU-level forecasts are available in the full report.)

Operational playbooks: Templates for production capacity planning, sterilization and packaging design, and supplier scorecards tuned to closed-circuit product lines.

Commercial toolkits: Pricing and rebate models, tender-response templates, and hospital value-case decks for infection‑control and condensate reduction benefits.

Company scorecards and competitor heatmaps: Side‑by‑side analyses of leading suppliers, proprietary benchmarking across technology, regulatory readiness, manufacturing footprint, and aftermarket economics.

Scenario & stress testing: Upside/downside cases showing how demand and margin behave under different clinical adoption, regulation, and supply-disruption scenarios.

Three macro dynamics determine near-term outcomes for fully closed breathing circuits: clinical priorities, technology evolution, and regulatory/reimbursement mechanics. Clinically, infection‑control bundles and a renewed emphasis on minimizing circuit breaks are keeping closed systems in high demand across critical care environments. Technology innovations that minimize condensate and extend closed‑system runtimes—such as permeable membrane designs, embedded heated-wire solutions, and vapour-permeable tubing—are driving differentiation in buying decisions.

From a regulatory perspective, breathing circuits are governed under established frameworks (for example, U.S. classification and connector/connector performance standards). Compliance pressure is increasing in high-volume markets as standards for connectors, materials and labeling (e.g., ISO connector standards) converge with hospital procurement requirements. On reimbursement, coding ambiguity persists: certain breathing circuit codes are subject to bundling rules and are not separately reimbursable when billed with routine ventilator servicing codes, which compresses the perceived value of standalone consumable upgrades in some payer regimes.

Supply‑side considerations are equally material. Manufacturing complexity varies between disposable single‑use designs and reusable/autoclavable systems; each demands distinct validation, sterilization, and supply‑chain resilience plans. A 2026 procurement strategy that ignores sterilization throughput, sterilant availability, or heated-wire component supply may see delayed product launches and margin erosion.

Fisher & Paykel Healthcare (Auckland, NZ) — A technology leader in condensate management (e.g., permeable membrane and Evaqua evolutions). Their 2025 regulatory activity (FDA 510(k) clearances supporting compatibility with single‑limb circuits and NIV interfaces) signals intent to expand hospital footprint and compatibility across ventilator platforms.

Plasti‑med (Turkey) — Differentiates through embedded spiral heated‑wire solutions for active humidification; attractive for customers prioritizing condensate control in compact designs.

Unimax Medical Systems, GaleMed, Besmed, Cathwide (Taiwan & regional suppliers) — Regional OEMs and contract-manufacturers focused on a mix of disposable closed circuits, closed‑suction systems and reusable options; competitive on cost and local regulatory agility.

Shenzhen Besdata (China) — Volume supplier of disposable closed circuits and closed‑suction catheters; notable for rapid product cycles and competitive pricing in Asia and emerging markets.

Armstrong Medical (UK) — Known for heated‑tubing and vapour‑permeable approaches (e.g., AquaVENT); the company competes on minimizing water traps and reducing maintenance touchpoints in high‑acuity settings.

Major medtech integrators (Teleflex, ICU Medical, Dräger, Medtronic, Hamilton) — These players integrate circuit technology with ventilators or anesthesia platforms and compete on systems compatibility, brand trust, and bundled service contracts.

Collectively, the competitive set exhibits a mix of specialized technology vendors, contract manufacturers, and integrated medtech OEMs. The market is neither atomized nor dominated by a single player — strategic opportunity exists for firms that can combine technical differentiation with robust regulatory documentation and OEM partnership models.

De‑risk product launches through regulatory first‑mover planning: Secure required conformity evidence (connector standards, biocompatibility, sterilization validation) early in product development to avoid time‑to‑market delays.

Invest selectively in condensate‑management IP: Target technologies (vapour‑permeable membranes, optimized heated‑wire routing) that demonstrably reduce maintenance events—these deliver a hospital cost‑of‑care narrative that supports premium pricing.

Build OEM and channel partnerships: Pursue co‑development with ventilator OEMs and establish long‑dated aftermarket supply agreements to secure recurring revenue.

Design manufacturing resilience: Map critical subcomponents (heated‑wire assemblies, specialized polymers) and establish dual sourcing or nearshore capacity to mitigate lead‑time risk.

Adopt value‑based commercial models: Where reimbursement is compressed, offer bundled service or outcome‑based contracts that align supplier incentives with reduced ventilator‑associated complications.

Screen M&A through aftermarket economics: Prioritize targets with strong consumable sales, a defensible installed base, and regulatory dossiers that are transferable or easily upgradable.

Beyond the report, PW Consulting offers tailored services to convert insight into action: interactive financial models and scenario workshops, M&A target screening and vendor diligence, commercialization roadmaps, and clinical‑economics packages designed for hospital adoption teams. Clients gain access to our full dataset and executable deliverables, including SKU-level forecasts, regional and application splits, supplier cost models, and a downloadable Excel-based decision engine.

For executives who need to finalize 2026 capital plans, our report functions as both a market compass and an operational playbook: it identifies where growth will come from, what variables most influence margin and revenue, and which levers (technology, regulatory timing, channel structure) unlock the highest returns.

PW Consulting intentionally reserves granular regional, application and SKU-level figures for the full report to protect client value and to ensure decision-makers evaluate sensitive strategic inputs with our advisory support. To access the complete dataset, company scorecards, and the downloadable forecasting model, please visit the PW Consulting report page or contact our industry team for a briefing and tailored workshop.

For detailed analysis of this topic, please visit the official page:Fully Closed Ventilator Breathing Circuit Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com