Marine Anti-Vibration Mounts Market: Strategic Imperatives for 2026 — PW Consulting Insights

PW Consulting’s latest market study on Marine Anti-Vibration Mounts (base year: 2025; historical coverage: 2020–2025; forecast: 2026–2032) frames a pragmatic roadmap for executive decision-making in 2026. The market, measured in USD Million, has expanded from roughly USD 648M in 2020 to about USD 845.5M in 2025 and is projected to approach USD 1,209M by 2032 under our base-case projection (CAGR 2026–2032: 5.24%). These headline dynamics reflect a market that has moved past recovery into a steady growth phase driven by higher maritime activity, stronger emphasis on acoustic environmental compliance, and continued investment in safety, comfort, and lifecycle economics of vessels and offshore assets.

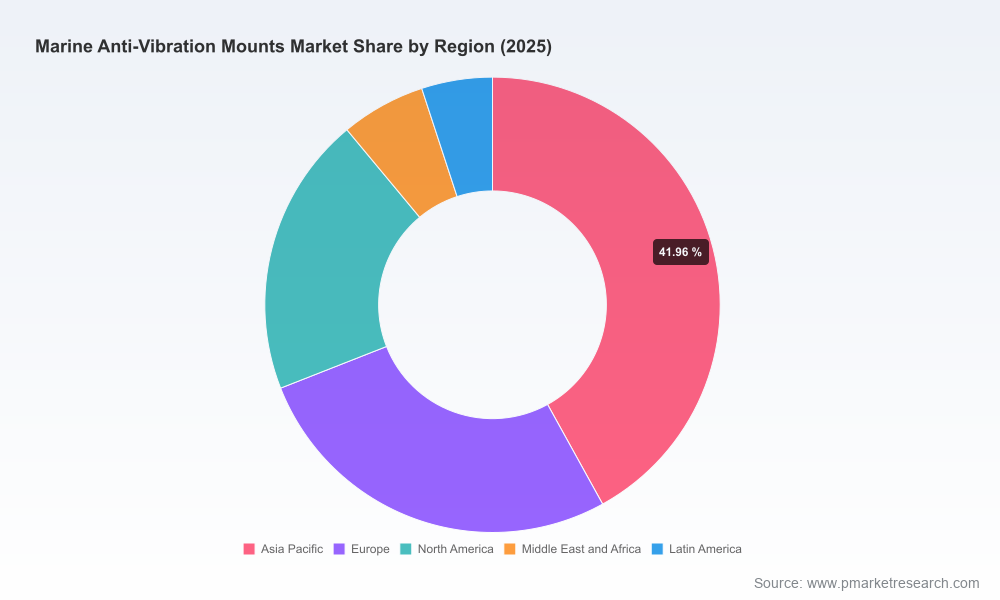

Marine Anti Vibration Mounts Market

Why this report matters for 2026 corporate strategy

- Provides a calibrated growth outlook to align product roadmaps, OEM contracts, and aftermarket strategies to a market growing mid-single digits through 2032.

- Translates raw-material volatility and regulatory pressure into quantifiable margin and pricing levers for procurement and finance teams.

- Delivers competitor benchmarking and tactical playbooks that support M&A screening, partnership prioritization, and targeted route-to-market experiments.

- Offers scenario-driven risk modelling (supply shock, regulatory acceleration, slower offshore CAPEX) to stress-test business plans for 2026 board approvals.

What the PW Consulting report delivers — actionable, not ornamental

- Robust market-sizing methodology and transparent assumptions, enabling clients to reproduce base and scenario forecasts for internal budgeting.

- Demand-driver decomposition and a forward-looking view on adoption curves for key technologies (elastomeric, polymer, hydraulic, pneumatic mounts and hybrid solutions).

- Supply-chain and raw-material cost models that translate rubber, synthetic composite and specialty-metal price swings into margin sensitivity by product family.

- Commercial playbooks: OEM negotiation templates, aftermarket service propositions, pricing strategies, and channel economics.

- Vendor scorecards and strategic profiles (product strengths, technical differentiators, market positioning) for the leading suppliers in the marine anti-vibration space.

- M&A and partnership shortlist with integration rationales, near-term synergies, and estimated payback ranges under multiple scenarios.

- Regulatory impact assessment focused on underwater acoustic requirements and compliance pathways for different vessel classes.

Note: the executive summary above intentionally highlights capabilities while omitting granular regional/application splits and detailed revenue-by-segment tables — these are preserved as gated content in the full report to support client engagement and bespoke consulting services.

Marine Anti Vibration Mounts Market

Market dynamics and strategic implications

- Growth drivers: Increased commercial shipping, renewed naval procurement cycles, expansion of offshore energy (both oil & gas and renewables), and the growing leisure-boat segment sustain demand for vibration-control solutions that improve comfort, reduce maintenance costs and limit underwater radiated noise.

- Input-cost volatility: Fluctuations in rubber and synthetic-composite prices meaningfully affect unit economics for elastomeric mounts. Procurement teams should deploy hedging strategies and multi-sourcing contracts while R&D explores material substitution and recyclable compounds to reduce exposure.

- Regulatory pressure and differentiation: Acoustic environmental protection is moving from recommendation to enforceable standards in several jurisdictions. Manufacturers able to certify underwater noise reduction and provide life-cycle compliance documentation will command pricing premiums and preferred OEM relationships.

- Product-technology bifurcation: The market is seeing a parallel demand for tried-and-tested elastomeric solutions and higher-value polymer or metal/polymer hybrid systems designed for chemical resistance and long service intervals in harsh marine environments.

- Service & aftermarket economics: The total cost-of-ownership conversation is shifting buyers toward integrated solutions (mount + installation + predictive maintenance). Companies investing in digital condition monitoring and service contracts can capture recurring revenue and improve customer retention.

Competitive landscape — strategic read on the leading players

Market concentration remains moderate (CR3 ≈ 32.45%; CR5 ≈ 48.12%), which presents both competitive pressure and consolidation opportunities. The landscape combines international incumbents with specialized regional players. Key strategic takes on selected vendors:

Marine Anti Vibration Mounts Market

- GMT Rubber‑Metal‑Technic Ltd (Leeds, UK) — Strength: purpose-designed marine engine mounts and resilient solutions with high-deflection capability. Strategic angle: licenseable design platforms and OEM partnerships for retrofits; attractive target for OEM alliances focused on vibration attenuation in medium-to-large engines.

- AMC Mecanocaucho (Spain) — Strength: rugged multi-axial stiffness architectures for mobile and marine applications. Strategic angle: well-positioned for cross-selling into adjacent mobile markets and for engineering consultancy services that differentiate through system-level vibration solutions.

- Trelleborg Antivibration Solutions (Sweden) — Strength: broad portfolio and global reach with proven marine/offshore credentials. Strategic angle: scale player able to bundle isolation, sealing and dampening systems; likely to lead on integrated platform solutions and large OEM contracts.

- R & D Marine (UK) — Strength: marine-focused engineering with strong product fit for reducing noise and propeller-thrust acceptance. Strategic angle: premium small-batch supplier for naval and custom commercial builds; attractive acquisition to bolster niche engineering capabilities.

- Christie & Grey (UK) — Strength: engineered isolation targeting underwater noise reduction; active market engagement (e.g., exhibition at the International WorkBoat Show, New Orleans, Dec 2025). Strategic angle: credibility in environmental compliance projects and high-value naval retrofit opportunities.

- Vibrasystems Inc. & Isoflex Technologies (Canada) — Strengths: materials-focused differentiation (316L stainless + EPDM; engineering polymers without rubber). Strategic angle: material innovation leaders for corrosive or oil-exposed environments; potential licensing partners for OEMs looking to extend maintenance intervals.

- AV Products, Hutchinson (Barry Controls / ASI‑Barry), Polymer Technologies (North America) — Strengths: aftermarket compatibility, fail‑safe mounts, legacy interchangeability with established brands. Strategic angle: defendable aftermarket franchises and opportunities to package service agreements and spares distribution networks.

Collectively, these profiles indicate a market where technical differentiation, material science, and channel control (OEM vs aftermarket) matter as much as price. Mid-sized engineering specialists and materials innovators represent attractive M&A targets for larger global players seeking capability depth without diluting R&D focus.

Recommended 2026 playbook — prioritized actions

- Hedge and dual-source critical elastomers: Lock multi-year supply agreements with indexation clauses and qualify polymer alternatives to limit margin erosion from raw-material spikes.

- Commercialize lifecycle economics: Shift sale conversations from unit price to total cost of ownership — bundle condition monitoring, installation, and spare-part programs to capture recurring revenue.

- Invest selectively in compliance credentials: Obtain acoustic certifications and publish verified underwater radiated-noise reduction case studies to gain access to regulated tenders and premium OEM slots.

- Pursue bolt-on M&A in aftermarket and regional service networks: With market concentration moderate, accreting acquisitions can create platform benefits (distribution scale, spare-parts logistics, faster retrofit cycles).

- Differentiate through materials and modularity: Prioritize polymer and hybrid product lines where service life and chemical resistance deliver clear buyer value; develop modular mounting systems to shorten OEM integration cycles.

- Embed digital monitoring: Pilot sensor-equipped mounts on representative fleets to validate predictive maintenance models and new service revenue streams.

Scenario planning and sensitivity

Under our base-case (CAGR 5.24% for 2026–2032) the market scales toward approximately USD 1.2Bn by 2032. Upside scenarios materialize if acoustic regulation accelerates or offshore renewables expand faster than current estimates; downside scenarios follow sustained raw-material inflation, major geopolitical disruptions to maritime trade, or slower-than-expected naval procurement. We provide stress-tested P&L and cash-flow models in the full report to quantify each scenario’s impact on margins, payback periods and working-capital needs.

How to use this intelligence in 2026

- CEOs and boards: Use the report to validate 3–5 year capital plans and M&A scorecards with upside/downside financials.

- Product & R&D leaders: Prioritize materials, sealing solutions, and digital-enabled mounts that shorten OEM qualification cycles.

- Procurement & supply-chain leads: Implement hedging, dual-sourcing, and supplier development programs using the cost-sensitivity templates included in the report.

- Commercial teams: Reframe sales to lifecycle-value propositions and pursue aftermarket service contracts for recurring revenues.

Next steps — where PW Consulting adds direct value

PW Consulting can provide tailored deep-dive workshops and custom modelling (regional roll-ups, application-level ROI, supplier due diligence) to convert this market intelligence into executable plans for 2026. The full report contains the withheld granular regional and application splits, detailed supplier scorecards, pricing matrices and a prioritized M&A shortlist — resources designed to shorten time-to-decision and improve execution confidence.

For executive summaries, bespoke scenario runs, or to commission a focused advisory engagement that converts this market view into a transactable roadmap, contact PW Consulting’s Marine & Offshore practice team.

For detailed analysis of this topic, please visit the official page:Marine Anti Vibration Mounts Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com