Metal Powder Atomizer Market: Strategic Imperatives for 2026 — PW Consulting Insights

Executive summary

The metal powder atomizer market is at an inflection point. After steady expansion through the early 2020s, the industry is entering a phase of capacity reconfiguration, supply-chain sophistication, and product-differentiation driven by advanced materials demand from additive manufacturing, aerospace, and specialized industrial applications. Our new market study — built on 2020–2025 historical performance and a 2026–2032 forecast horizon — quantifies that trajectory and translates it into operational and corporate-level actions for decision makers targeting 2026 execution windows.

Metal Powder Atomizer Market

Market trajectory: the high-level numbers that shape strategy

Key macro indicators from our analysis provide a clear planning envelope: the global market grew from USD 482.15 million in 2020 to USD 673.4 million in 2025 and is projected to continue expanding through the 2026–2032 forecast period at a compound annual growth rate (CAGR) of 6.84%, reaching roughly USD 1,070.07 million by 2032. These topline dynamics create a predictable, mid-single-digit growth environment — large enough to support new projects and consolidation, but not so rapid that first-mover scale alone guarantees long-term dominance.

Metal Powder Atomizer Market

Concentration metrics further inform strategy: the three largest suppliers account for approximately one-third of the market, while the top five capture just under half. In plain terms, the market remains fragmented with clear pockets of leadership — a structure that favors focused scale-ups, technology differentiation, and targeted M&A to meaningfully move the share needle.

Metal Powder Atomizer Market

What this means for 2026 decision-making

- Capex timing and scale: With steady mid-single-digit CAGR, firms should prioritize modular, scalable atomization assets rather than one-off, fully integrated “big-bang” plants. Staged investments that allow rapid addition of melt/atomization modules or conversion between gas and water atomization will reduce market timing risk while preserving upside.

- Product mix strategy: Spherical, low-oxygen powders for high-value applications will continue to command premiums. Companies must match process choices (vacuum/inert VIGA/EIGA, gas atomization, or high-pressure water atomization) to end-use quality and traceability requirements rather than pursue throughput alone.

- Supply-chain robustness: Raw consumables — notably inert gases and process water — are material cost levers. Investments in gas recirculation, on-site gas generation, or closed-loop water recycling deliver both margin protection and ESG benefits.

- Regulatory and safety readiness: Production of reactive metals necessitates ATEX-rated facilities and rigorous atmosphere control. Firms entering or expanding in reactive-metal segments must budget for compliance and safety engineering early in project planning cycles.

- Go-to-market and service models: The emergence of direct-fill and inert-storage logistics (industry partnerships enabling powder transfer directly from atomizer to AM printer hoppers) alters unit economics and customer lock-in. Expect new commercial constructs that bundle powder supply, handling, and traceability services.

Operational levers that materially affect margins

Our field and cost-model work identifies a handful of operational levers that determine competitive margin bands in 2026:

- Gas handling and recirculation: For gas atomizers, argon or nitrogen consumption is a recurring, high-impact cost. Recirculation and on-site generation systems reduce variable costs and stabilize supply risk.

- Melting & atmosphere control: Vacuum induction melting and inert atmosphere processing lower non-metallic inclusions and gas pickup, enabling higher-value powder grades. These process steps, however, require additional capital and yield discipline.

- Water management for water atomization: Ultra-high pressure water atomizers leverage pressurization and recycling to manage both particle-size distribution and environmental impact; process-water reuse is an increasingly visible KPI for buyers and regulatory agencies.

- Quality assurance and certification: Investments in particle-shape analytics, oxygen/hydrogen/nitrogen monitoring, and batch-level traceability are nondiscretionary for aerospace and medical supply chains.

Competitive landscape: who matters and why

The competitive topology mixes specialist engineering OEMs, integrated metal producers, and innovative small-batch providers. Several firms illustrate the spectrum of strategic options available to market participants:

- High-purity, integrated specialists: Firms with vacuum induction melting and inert gas atomization capabilities lead in high-performance spherical powders demanded by aerospace and critical industrial markets. Their value proposition is purity, alloy breadth, and process control.

- Flexible midscale OEMs: Companies offering modular gas, water, and hybrid atomizers serve customers who prioritize agility: research centers, AM service bureaus, and niche alloy producers. These suppliers are often first to market with bespoke atomizer configurations and R&D partnerships.

- Volume-focused water atomizer providers: Established water-atomization vendors target mass-production of irregular or sub-spherical powders for traditional powder metallurgy and lower-specification industrial uses. Their competitive edge is throughput and lower per-unit processing cost.

Recent market developments underscore strategic directions: partnerships enabling inert direct-fill logistics, commissioning of new EIGA/VIGA capacity for titanium and refractory alloys, and academic–industry collaborations to close the in-house powder value chain. These moves validate two themes we flag repeatedly: vertical integration of the powder-to-part workflow, and capacity investments aimed at priority alloys rather than indiscriminate volume expansion.

Risk matrix and mitigation (practical list for 2026 planning)

- Supply concentration on critical gases: Mitigation — diversify suppliers, adopt gas recirculation, and evaluate on-site generation.

- Regulatory/safety non-compliance: Mitigation — invest in ATEX-rated equipment, third-party safety audits, and operator training programs early in project schedules.

- Quality failure for high-spec powders: Mitigation — implement end-to-end traceability, inline analytics, and stage-gate release protocols tied to customer acceptance tests.

- Customer lock-in by logistics innovations: Mitigation — pursue partnerships that mirror direct-fill advantages (e.g., certified inert containers) or co-invest in integrated handling solutions with key customers.

Actionable pathways: five strategic plays for 2026

- Selective capacity expansion: Prioritize additional atomizer units for alloy segments exhibiting above-average growth and margin — scale incrementally with pre-validated offtake agreements.

- Vertical integration where it matters: Integrate melt-to-printer logistics for premium alloy lines while outsourcing commodity powder production to low-cost specialists.

- Technology differentiation: Invest in atmosphere control, particle-shape control, and digital process twins to reduce variability and command quality premiums.

- M&A and partnerships: Target tuck-ins that extend alloy capability or add direct-fill/logistics IP rather than attempting large-scale horizontal consolidation in a fragmented market.

- Operational sustainability: Deploy water-recycling and gas-recirculation projects with clear payback horizons; position sustainability as a procurement differentiator for OEMs.

What PW Consulting’s report delivers (practical, executable content)

Our report is designed as a hands-on decision-support tool for executives, investors, and plant managers who need to act in 2026. Key deliverables include:

- A proprietary demand model covering 2020–2032 with scenario toggles for alloy mix, end-use adoption curves, and pricing sensitivity;

- A capital-expenditure playbook that maps atomizer types to expected unit economics, throughput profiles, and time-to-market for typical scale-ups;

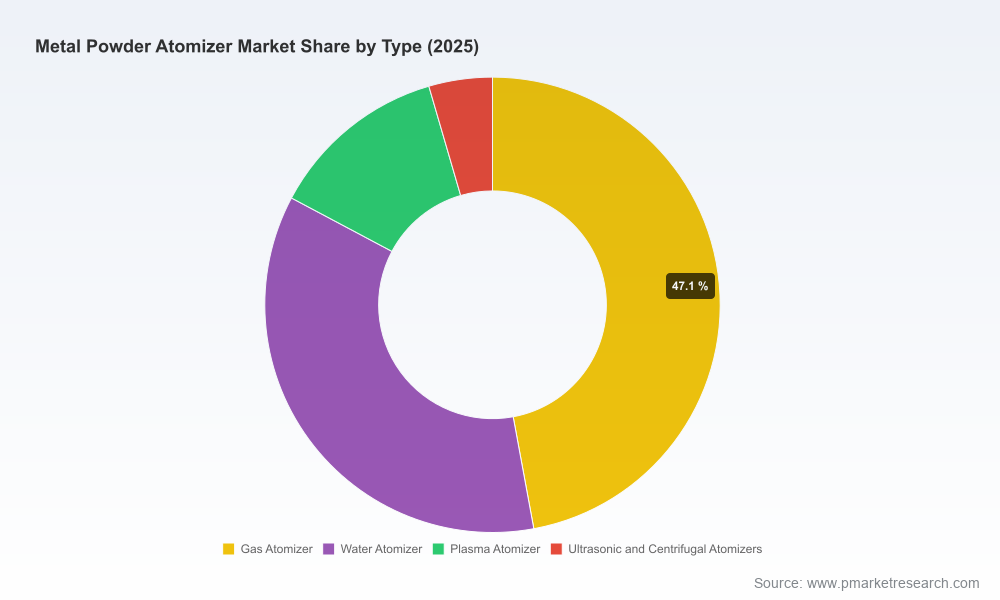

- Vendor and technology archetypes with comparative assessments (strengths, limitations, ideal use cases) for vacuum/inert, gas, water, plasma, and ultrasonic/centrifugal atomization;

- Regulatory and safety checklist tailored for reactive-metal processing including ATEX compliance and atmosphere-control requirements;

- A supplier-sourcing guide and procurement RFP templates that reflect current lead times, equipment delivery risks, and post-installation support metrics;

- An M&A screening tool using concentration metrics, route-to-market gaps, and integration risk scoring to prioritize targets that move CR upwards efficiently;

- Case studies and playbook examples from recent industry moves that demonstrate capacity commissioning, partnership models, and production scaling.

Final considerations and call to action

The 2026 planning window rewards pragmatism: balance measured capacity additions with differentiated product strategies and operational improvements that reduce key variable costs. The mid-single-digit CAGR provides a stable growth runway — but success will accrue to firms that simultaneously manage consumable costs, ensure regulatory readiness, and differentiate on quality and logistics convenience.

For procurement teams, engineering leads, and corporate strategists preparing 2026 budgets, PW Consulting’s Metal Powder Atomizer Market report converts market projections into executable steps, financial templates, and vendor playbooks. The report includes the full dataset, interactive models, and granular segmentation that underpin the summary insights presented here — reserved expressly for report subscribers.

To access the complete dataset, interactive forecast model, and supplier scorecards that drive the specific asset-level recommendations in this brief, visit our report landing page or contact PW Consulting for a tailored briefing and executive workshop.

For detailed analysis of this topic, please visit the official page:Metal Powder Atomizer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com