Global Tobacco Leaves Market Set to Hit USD 27.1 Billion by 2034 at 3.7% CAGR

Other |

2026-06-18 10:17:33

PW Consulting's new 4‑Bromoanisole Market report provides an operational playbook for companies making material decisions in 2026. The market for 4‑Bromoanisole has shown steady, predictable growth through the early 2020s and the outlook remains constructive: total market revenue rose from USD 46.1 Million in 2020 to USD 56.7 Million in 2025, and our baseline forecast projects growth to USD 77.27 Million by 2032, implying a compound annual growth rate (CAGR) of approximately 4.52% across the 2026–2032 forecast window. For executives evaluating capacity moves, pricing tactics, or strategic partnerships this year, the report converts these macro trajectories into actionable decisions without relying on speculative assumptions.

4 Bromoanisole Market

Three practical pressures make 2026 a pivotal planning year for participants in the 4‑Bromoanisole value chain:

4 Bromoanisole Market

Our report maps these pressures to concrete strategic actions (pricing frameworks, supplier stratification, inventory policy, and product‑portfolio choices) that can be implemented in the next 6–12 months.

4 Bromoanisole Market

PW Consulting’s topline modelling combines historical shipment data (2020–2025) with bottom‑up supply assessments and demand drivers in pharmaceuticals, flavors & fragrances, and specialty materials to deliver a conservative baseline and two alternate scenarios (constrained supply; accelerated demand adoption). The baseline shows steady expansion in absolute revenue with mid‑single‑digit CAGR across the forecast period. We calibrated our scenarios to real inputs: recent increases in bromine and anisole feedstock costs, trade tariff status, and regulatory developments.

Two points that should drive boardroom conversations in 2026:

Our company analysis synthesizes public product specifications, pack sizes, service models, and route‑to‑market strategies for the primary suppliers in the market. Notable themes we observe:

Representative company profiles included in the report:

Market concentration metrics (presented in the report) show a moderate level of concentration: the market top three and top five firm shares suggest that competitive dynamics will be governed by service differentiation rather than pure price competition alone. Our supplier scorecards rate players across purity ranges, packaging flexibility, analytical support, lead‑time reliability, and regulatory readiness.

Raw‑material developments in late 2025 and early 2026 have direct implications for near‑term procurement strategy. Notably, bromine costs experienced an upward repricing driven by supply constraints in key producing regions, and anisole feedstock has seen price pressure from derivative demand and upstream phenol tightness. Our cost‑pass‑through analysis quantifies how these inputs propagate to finished 4‑Bromoanisole pricing under common margin frameworks.

For procurement leaders, the report recommends a layered hedging approach: secure core capacity through contracts with performance clauses, identify alternative sourcing corridors to mitigate regional disruptions, and negotiate variable pricing mechanisms tied to transparent input indices. We also model the inventory carrying cost tradeoffs between holding strategic stock versus paying a premium for emergency spot shipments.

Regulatory shifts are reshaping compliance costs. Recent registration and safety documentation requirements in major jurisdictions have increased administrative burden for substances with specific hazard classifications. Our regulatory impact analysis maps the incremental cost and time‑to‑market implications for different product grades and routes of sale (research vs. GMP pharmaceutical supply). Additionally, current trade measures on brominated anisoles remain in place in some markets; our tariff sensitivity analysis demonstrates when onshore production becomes economically preferable to importation.

Consistent with PW Consulting’s focus on implementable intelligence, the report contains:

Our consulting team advises three concurrent moves for companies aiming to convert the 2026 environment into long‑term advantage:

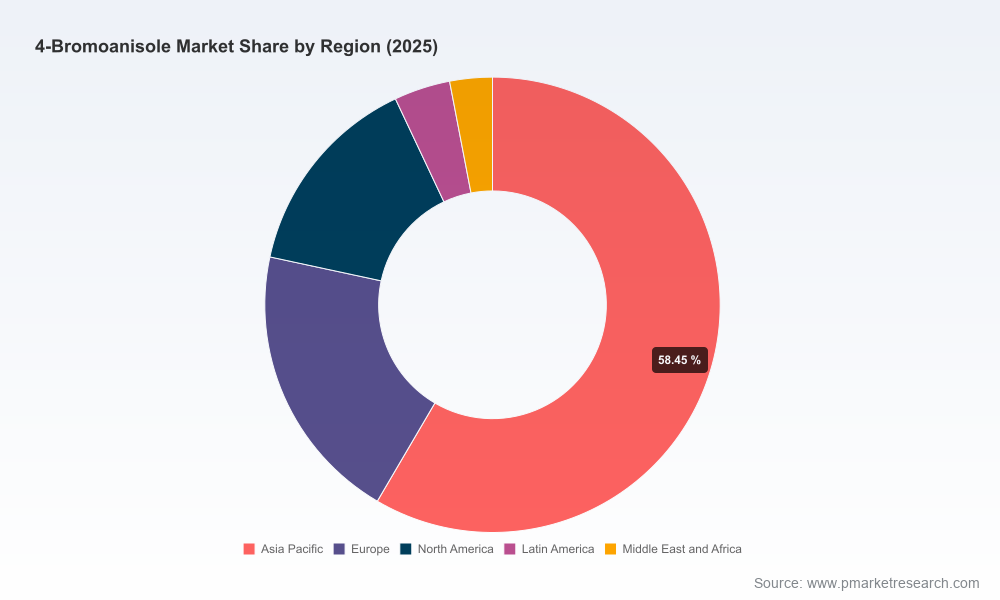

To provide maximum utility at the board and operational level while preserving the competitive value of the research, this press summary intentionally omits granular regional and application split percentages and the detailed, cell‑level market tables. These sectional breakdowns — which include region‑by‑application rollups, price elasticities, and customer size buckets — are available in the full report and the accompanying dataset. That granular layer is essential for transaction teams, procurement heads, and country managers who need to tailor negotiation tactics or investment cases to specific markets.

We designed the report as a decision support toolkit for the coming 12–18 months. Use it to:

PW Consulting is offering a modular licensing option for the full 4‑Bromoanisole Market report that includes the Excel model, supplier scorecards, and a one‑hour briefing workshop with the lead analyst. For teams that require deeper validation, we provide tailored deep‑dive engagements — from procurement program redesign to target diligence for M&A. Access to the full dataset and the segmented intelligence is available on the report landing page.

For executives planning their 2026 strategy: use the topline trajectories and scenario logic presented here as a framework for immediate planning, and consult the full report to operationalize supplier tactics, regulatory timing, and transaction roadmaps. PW Consulting will support implementation with pragmatic, measurable next steps.

For detailed analysis of this topic, please visit the official page:4 Bromoanisole Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com