Buy Verified PayPal Accounts Superfast Delivery Guaranteed

Fitness |

2026-05-31 13:10:19

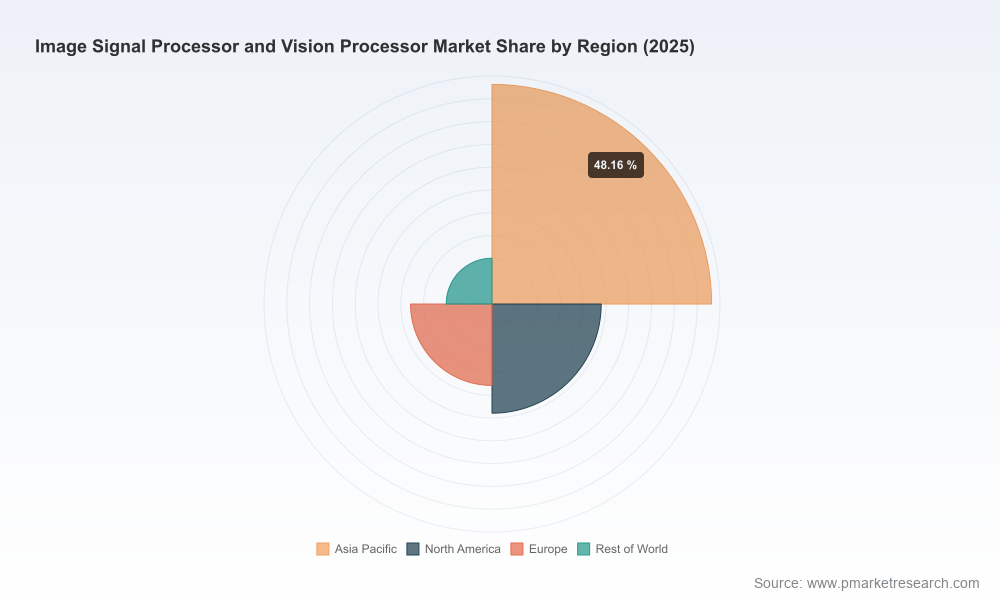

PW Consulting’s latest Image Signal Processor (ISP) and Vision Processor Market report (base year 2025; forecast period 2026–2032) shows the market at an inflection point. After steady expansion through the early 2020s, total industry revenue reaches USD 5,800.0 Million in 2025 and is forecast to exceed USD 10,700 Million by 2032, representing a compound annual growth rate (CAGR) of 9.16% across the 2026–2032 window. This trajectory is driven by accelerating edge AI adoption, higher video resolutions and multi‑sensor fusion in automotive and robotics, and the migration of image enhancement tasks from the cloud to the device edge.

Image Signal Processor And Vision Processor Market

This release is a strategic preview: it distils the report’s high‑value, actionable insights for corporate leaders and investors while intentionally withholding detailed sub‑segment tables and interactive model outputs to encourage direct access to the full report for transaction‑grade data.

Image Signal Processor And Vision Processor Market

Edge AI and the integration of ISP and vision AI. Suppliers are consolidating imaging pipelines into single SoCs or sensor‑level intelligent devices. The result: hardware inflection toward integrated ISPs with dedicated AI accelerators. Companies that combine high‑quality ISP chains with on‑chip neural engines gain architectural advantages for low‑latency inference and power efficiency.

Image Signal Processor And Vision Processor Market

Multi‑sensor and high‑resolution demand. OEMs are moving from single‑camera systems to multi‑stream architectures (surround view, sensor fusion for ADAS, industrial multi‑camera perception). This raises requirements for simultaneous multi‑stream processing, deterministic latency, and bandwidth‑efficient interconnects—factors that change SoC selection, thermal design and board‑level BOMs.

Regulatory and trade risk elevating procurement complexity. In early 2026, new U.S. measures (including a 25% ad valorem tariff under Section 232 on specified advanced computing chips and tightened export licensing) and heightened scrutiny on processed critical minerals have added near‑term cost risk and lead‑time uncertainty for global supply chains. Expect near‑term program impacts and longer‑term supplier reshoring or dual‑sourcing strategies.

Supply chain cadence and lead times. Select semiconductor lead times have trended toward 30–42 weeks for some IC families amid surging AI demand. This increases inventory carrying costs, prioritization conflicts, and the value of long‑lead contracting and capacity reservation mechanisms for vehicle programs and large OEMs.

Concentration and competitive dynamics. Market concentration is meaningful: the top three vendors account for roughly 42.5% of market revenue, and the top five control about 61.8%. This concentration accelerates the importance of vendor relations, partner ecosystems, and differentiated IP as sources of competitive advantage.

The vendor field is diverse: legacy silicon suppliers, image‑sensor incumbents, specialized ISP IP houses, and emerging AI‑first entrants. Below are the strategic postures we observe among core participants and the implications for customers and investors.

Ambarella — positioning as a high‑performance edge AI SoC supplier. Its recent CV7 product (announced January 2026) targets multi‑stream 8K video and integrates an advanced ISP plus AI accelerator on an advanced process node. Strategic implication: Ambarella is competing on highest‑end compute and multi‑stream throughput, which makes it attractive for premium security, robotics, and certain automotive applications where performance/watt is a gating factor.

onsemi — focused on dedicated ISP co‑processors and deep integration with CMOS sensors for automotive and industrial. Their orientation toward safety‑critical and industrial segments reduces direct exposure to consumer cyclical risk, but increases emphasis on long-term program qualification and supply continuity.

Qualcomm and other SoC platform houses — offering broader vision intelligence platforms with integrated ISPs and AI fabrics targeting IP cameras, IoT and edge AI. These suppliers compete on ecosystem breadth (software stacks, cloud integration) as much as raw imaging performance.

NXP, Renesas, STMicroelectronics, Texas Instruments — leveraging automotive and industrial processor portfolios, partner ecosystems, and functional safety capabilities. Their strength is in system‑level integration, long lifecycle programs and compliance with automotive qualification flows.

indie Semiconductor and OmniVision — niche specializations: indie on automotive vision processors with concurrent multi‑sensor throughput; OmniVision on companion ISP chips for sensor pairing. These firms play to customers needing tailored imaging stacks for vehicle architectures and surround‑view systems.

Chips&Media — emerging as a disruptive IP and software play with the world’s first full AI‑based ISP pipeline announced in early 2026. Such software‑defined imaging approaches can commoditize parts of the traditional ISP chain while creating new opportunities in post‑capture enhancement licensing.

Sony Semiconductor Solutions — moving ISP intelligence closer to the sensor with intelligent vision sensors, altering tradeoffs between sensor selection and downstream processing requirements.

Ambarella’s January 2026 CV7 launch signals continued node‑level competitiveness and a push for premium, multi‑stream edge AI markets.

Chips&Media’s AI‑defined ISP pipeline demonstrates a shift toward software‑defined image enhancement that can be licensed across OEMs, compressing time‑to‑market for advanced video features.

indie’s multi‑input vision processors (announced earlier) validate that automotive OEMs are demanding higher concurrent throughput under constrained latency and safety requirements.

Re‑baseline your semiconductor roadmap: Update BOM models to reflect tariff scenarios, possible passthrough costs, and extended lead times. Prioritize components subject to export control risk for alternative sourcing or early allocation.

Architect for modularity: Favor software‑defined pipelines and modular ISP/AI stacks where feasible to reduce lock‑in and accelerate feature rollouts across model lines.

Hedge supplier concentration risk: Given the ~42.5% CR3 and ~61.8% CR5 concentration, build multi‑tier supplier strategies, leverage long‑term purchase commitments for critical parts, and consider local content or dual‑sourcing to mitigate regulatory exposure.

Negotiate capacity and quality commitments: Secure forward allocation or co‑development arrangements for advanced process nodes that underpin next‑generation vision SoCs.

Invest in imaging IP and software: In an environment where AI‑driven ISP innovation can be licensed, owning or partnering for key algorithms and pipelines is a defensible source of differentiation.

Run scenario planning and TCO analyses: Use scenario frameworks that include tariffs, lead‑time shocks and second‑order effects (software validation cycles, supplier qualification) to inform sourcing and go‑to‑market timing.

Prioritize safety and compliance for automotive programs: The automotive share for leading vision suppliers is material; ensure that supplier selections align with functional safety, cybersecurity, and long lifecycle requirements.

An interactive market model (USD Million) with historicals (2020–2025) and a 2026–2032 forecast, scenario toggles and sensitivity blocks based on tariff, lead‑time and technology adoption inputs.

Vendor benchmarking: technology maps, product timelines, go‑to‑market fit, and a strategic vendor scorecard covering performance, ecosystem, supply resilience and partner openness.

Go‑to‑market playbooks for OEMs and semiconductor vendors: procurement levers, partnership contracts, licensing approaches and IP protection recommendations.

Supply chain risk heatmap and procurement negotiation templates tailored to imaging and vision silicon categories (including recommended contractual clauses for capacity, warranty and export‑compliance).

Capital expenditure and TCO models for in‑vehicle and edge deployments, including BOM sensitivity to imaging resolution, multi‑sensor counts, and on‑chip versus off‑chip processing choices.

M&A and investment radar highlighting strategic targets, valuation approaches and integration playbooks for both horizontal ISP IP and vertical sensor‑to‑software consolidation opportunities.

The next 12–18 months will determine which suppliers and OEMs capture disproportionate share in a market poised to roughly double by the end of the decade. Technology choices made now—platform vs. companion chips, in‑sensor intelligence vs. SoC integration, licensing vs. ownership of AI pipeline software—will lock in cost, performance and upgrade paths for multi‑year programs. PW Consulting’s market model and actionable playbooks are built to support executive decisions on sourcing, R&D prioritization, M&A timing and regulatory risk mitigation.

For access to the full dataset, interactive models, and the complete vendor profiles and tables omitted in this preview, please visit the PW Consulting report page or contact our industry desk for a briefing. This preview intentionally omits detailed sub‑segment tables and downloadable financial models to ensure you engage directly with our secure, versioned report delivery for transaction‑grade detail.

For detailed analysis of this topic, please visit the official page:Image Signal Processor And Vision Processor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com