Desiccant Caps and Closures Market: Strategic Intelligence to Guide 2026 Decisions

PW Consulting’s latest market study on Desiccant Caps and Closures provides corporate leaders with the evidence-based foresight necessary to shape product, procurement, and M&A strategies in 2026. The market narrative is clear: a steady, mid-single-digit compound annual growth path, intensifying regulatory and material-cost pressures, and rapid product innovation by incumbents are reshaping competitive advantage. This release summarizes the report’s strategic takeaways while intentionally omitting the granular segment tables—our purpose is to demonstrate analytic depth and tactical relevance while directing decision-makers to the full report for the underlying segment-level intelligence and model outputs.

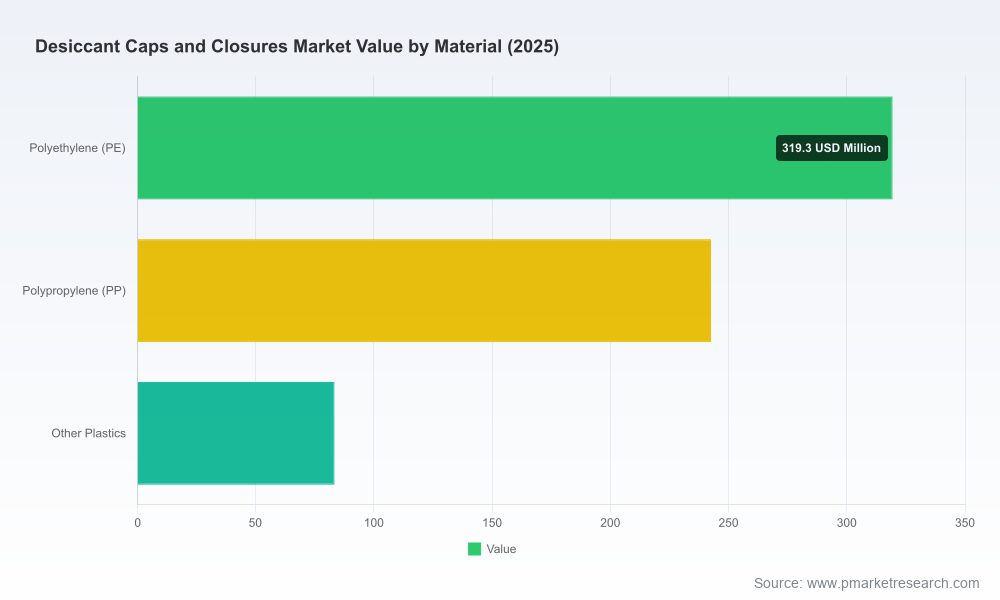

Desiccant Caps And Closures Market

Market trajectory at a glance

Between 2020 and 2025 the global desiccant caps and closures market expanded consistently, reflecting growing demand from pharmaceutical, nutraceutical, diagnostic, and moisture-sensitive packaging applications. PW Consulting’s base-year sizing (2025) and forward-looking model point to a continuation of that trend across the 2026–2032 forecast window at a compound annual growth rate of approximately 5.45%.

Desiccant Caps And Closures Market

The trajectory we model shows the market moving from a mid‑hundreds‑million USD industry in the early 2020s to a near‑billion‑dollar opportunity by the end of the next forecast cycle. This growth is not uniform—drivers include drug and nutraceutical oral solid-dose growth, expansion of point-of-care diagnostics, retrofit demand for improved moisture control, and substitution of loose desiccants with integrated closures for convenience and compliance. Our scenario analysis quantifies the relative contribution of these drivers and stress-tests them against commodity and regulatory shocks.

Desiccant Caps And Closures Market

What the PW Consulting report delivers — practical, actionable content

- Robust market-sizing and forward model: scenario- and sensitivity-based revenue forecasts covering 2026–2032, with clear assumptions and a replicable model you can run under alternate price, raw material, and adoption outcomes.

- Supply‑chain and cost‑curve analysis: detailed breakdown of manufacturing cost drivers, resin and desiccant input volatility, and margins by manufacturing archetype (captive vs. outsourced). The model integrates recent producer-price signals for plastics resins to quantify margin compression risk under realistic input-cost shocks.

- Regulatory and circularity impact matrix: policy-driven scenario mapping (including EU recyclability mandates and expanding US extended producer responsibility regimes) and practical design-for-recyclability checklists for closures and caps.

- Customer adoption playbooks: go-to-market segmentation (by end-use and procurement archetype), value-proposition templates (for pharma OEMs, CPGs, contract packagers), and a commercial risk checklist for switching costs and validation timelines.

- Competitive benchmarking and M&A screening: supplier scorecards across technology, IP, regulatory readiness, and manufacturing footprint; identification of likely consolidation targets and divestiture candidates for strategic or financial buyers.

- Technology and innovation brief: evaluation of integrated desiccant closures, tamper-evident/desiccant hybrids, breathable media approaches, and early signals on smart/IoT-integrated moisture monitoring systems.

- Implementation roadmaps: prioritized tactical moves for procurement, product development, and regulatory teams—time-sequenced 6–18 month initiatives aligned to a two‑year decision cycle.

Note: this release highlights the report’s structure and strategic levers; the full report contains the anonymized customer demand matrices, supplier cost models, and downloadable forecasting workbook required to operationalize these recommendations.

Competitive landscape — who’s shaping the market

The market is characterized by a mix of specialized closure manufacturers, legacy packaging houses, and desiccant technology providers. Market concentration is moderate: our CR3 and CR5 measures indicate that the top three players control a meaningful share of demand while the top five strengthen that position—enough to influence standards and procurement dynamics, but not so concentrated as to preclude new entrants with superior cost or design propositions.

- Sanner Group (Germany): A technology-focused incumbent with integrated desiccant closures and systems tailored to pharma and nutraceuticals. Sanner’s product portfolio—ranging from desiccant closures with tamper-evident features to container systems—positions it well for customers seeking validated, pharmacopeia-aligned solutions. Their emphasis on system pairing (closures + glass/aluminum containers) reduces buyer complexity and increases switching costs.

- Colorcon (United States): Known for integrated all-in-one closures, Colorcon’s recent product launch of a cap that eliminates separate sachets highlights a defensive move to capture value from customers seeking single-component moisture solutions. Their strengths lie in regulatory know-how and established pharma relationships.

- WiseSorbent Technology (United States): Focused on capsule and breathable-media solutions, WiseSorbent competes on configurable formats appealing to health-care OEMs and specialty packaging buyers who prioritize custom desiccant loading and sterile handling pathways.

- Xinfuda Group (China): A high-volume screw-cap and container integrated-cap manufacturer, Xinfuda combines cost-competitive manufacturing with multiple desiccant chemistries. Their scale makes them a natural player for global CPG and regional pharma supply chains seeking price-optimized components.

- Nutraplast and Baltimore Innovations: Niche specialists focusing on test-strip and high-performance medical packaging respectively, leveraging domain expertise to win design-specific contracts and maintain premium margins.

- ALPLA Pharma and other European players: Strong in tamper-evident and regulatory-compliant closure systems, with capabilities that cater to regulated pharmaceutical markets.

- Airnov and other desiccant systems providers: Their strategic developments center on reducing component counts and simplifying assembly for pharma customers; integration partnerships with closure producers are a recurring theme.

Recent vendor moves—Colorcon’s 2026 all-in-one closure, Sanner’s TabTec CR development, and industry discourse on smart desiccants—signal a market where product innovation, regulatory alignment, and ease of validation will define winners. For buyers and investors, that means evaluating suppliers not only by price and capacity but by their product validation timelines, documentation readiness, and capacity to deliver mono-material or tethered-cap designs under emerging recyclability rules.

Market dynamics and risk factors

- Raw material pressure: Desiccant closures rely predominantly on polypropylene (PP) and HDPE resins combined with silica gel or molecular sieves. Recent producer price indices for plastics suggest elevated volatility; procurement strategies must account for pass-through mechanisms and hedging where possible.

- Regulatory and circularity constraints: The EU’s packaging rules and a growing number of US state EPR laws are driving design-for-recyclability requirements (tethered caps, mono-material closures). Firms that proactively redesign closures to align with eco-modulated fees will avoid margin erosion and capture sustainability-driven procurement contracts.

- Pharmaceutical validation burden: Pharmaceutical-grade closures must meet FDA, EMA, and relevant 21 CFR expectations. Companies offering validated, pharma-ready closures shorten customers’ adoption cycle and command a pricing premium.

- Innovation trajectory: Integration of desiccant media into closures, reduction of component counts, and nascent smart packaging concepts (IoT-enabled moisture monitoring) are technology paths that will bifurcate supplier economics—those able to scale integrated closures will capture broader share.

Strategic imperatives for 2026 decision-makers

Executives allocating CAPEX, negotiating supplier agreements, or evaluating M&A targets in 2026 should prioritize the following actions:

- Embed regulatory foresight into design cycles: mandate recyclability and mono-material compatibility in new product specs now to avoid redesign and EPR penalties later.

- Validate suppliers beyond price: require documented regulatory and validation packages (stability, interaction, extractables), especially for pharma and nutraceutical customers where time-to-market matters.

- Diversify sourcing with cost-insurance: balance lower-cost regional suppliers with validated, higher-cost partners that reduce qualification lead time for regulated customers.

- Invest in integrated solution pilots: run 6–9 month trials with suppliers offering all‑in‑one closures to quantify OPEX reductions from eliminated sachets and lower assembly complexity.

- Monitor input-cost indices and embed indexation clauses: link pricing agreements to resin indices or pre-negotiated hedging instruments to protect margins during commodity swings.

- Scan the M&A landscape for capability fills: targets with validated pharma dossiers, unique closure geometry patents, or mono-material manufacturing processes offer faster route-to-compliance than greenfield programs.

- Prepare commercialization roadmaps for smart desiccant concepts: track early IoT integration pilots and intellectual property; consider partnerships with sensor providers and contract packagers.

How PW Consulting helps

Our Desiccant Caps and Closures report couples a transparent forecasting engine with supplier scorecards, regulatory compliance playbooks, and executable commercial plans. For firms needing rapid prioritization, we offer a tailored decision workshop: a two-week rapid assessment that maps your current supplier base, quantifies failure modes under regulatory scenarios, and delivers a prioritized 12‑month action list with expected cost and time-to-benefit estimates.

To access the complete intelligence—including anonymized segment revenues, end‑use adoption curves, supplier-level P&L proxies, and the downloadable forecasting model—visit the full report page or contact PW Consulting’s industry team. The detailed data and model are essential to convert the strategic imperatives above into measurable 2026 KPIs and to safeguard investment decisions against material, regulatory, and validation risk.

Closing

The desiccant caps and closures market in 2026 is not a simple volume story: it is a convergence of drug-market growth, regulatory inflection points, material-price volatility, and supplier innovation. Companies that act now—by redesigning for recyclability, validating integrated closure formats, and embedding cost‑risk protections—will capture the disproportionate share of value as the market advances toward the next decade. PW Consulting’s research provides the empirical foundation and operational roadmaps to make those choices with confidence.

For detailed analysis of this topic, please visit the official page:Desiccant Caps And Closures Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com