Artificial Intelligence Operations Platform Market Overview: Key Drivers and Challenges

Other |

2026-04-13 04:20:44

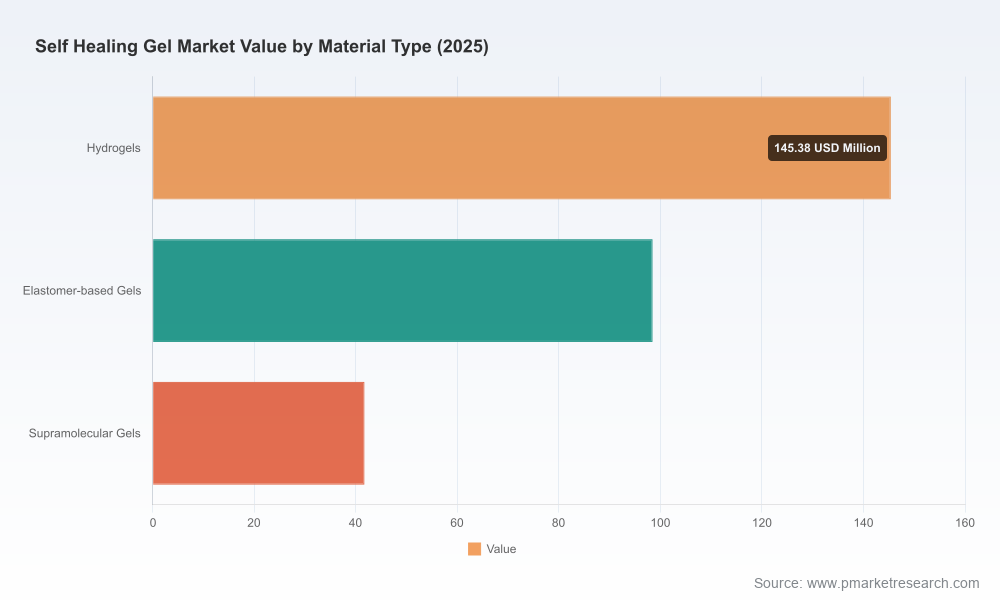

The self-healing gel market is transitioning from a research-driven niche into a commercially viable growth sector. Our latest market model shows a sustained compound annual growth rate (CAGR) of 9.85% across the 2026–2032 forecast window, building on a trajectory that saw the global market expand from the mid‑three‑digit USD million range in 2020 to a substantially larger footprint by the 2025 base year. This trajectory accelerates in the near term and is projected to more than double market value by 2032. For corporate leaders planning 2026 strategic moves—R&D prioritization, manufacturing scale decisions, commercialization timing, and M&A targeting—these dynamics alter risk-reward profiles and execution timetables. This brief distills the report’s strategic value without disclosing the detailed segment-level figures (available in the full PW Consulting report).

Self Healing Gel Market

Commercial readiness: Regulatory pathways and select real-world evidence (RWE) are shortening time-to-market for clinically focused self-healing hydrogels and related matrices. Accelerated regulatory routes in certain jurisdictions are enabling faster commercialization for advanced wound-care and device-coating applications—advantageous for firms with robust early-stage clinical programs.

Self Healing Gel Market

Technology convergence: Breakthroughs in biomimetic design, supramolecular chemistry and polymer engineering reported through 2024–2025 are reducing previous performance trade-offs (mechanical strength vs. self-repair kinetics). This closes critical gaps between laboratory prototypes and production-grade formulations suitable for medical, sensor and soft-robotics use cases.

Self Healing Gel Market

Capital and competition timing: As private and strategic investors increasingly view self-healing gels as an adjacent play to regenerative medicine and wearable sensors, 2026 will be a window to capture scale benefits. Companies that delay may face higher entry costs as manufacturing and raw material supply chains tighten.

Using a 2025 base and the 2026–2032 forecast horizon, our top-down model integrates primary interviews, supplier pricing trends and clinical adoption curves to generate a forward view. The market’s near‑term uplift reflects accelerating clinical adoption and nascent industrial applications; the medium term is driven by broader use in soft robotics, sensing, and next‑generation wound care products. At a nearly 10% CAGR through 2032, incumbents and new entrants should anticipate a multi‑year runway for commercial scale and should calibrate investment to capture first-mover advantages in commercialization and supply resilience.

Market sizing and scenario models — base‑case and sensitivity runs calibrated to regulatory timelines, raw material cost shocks and clinical adoption curves (2026–2032 forecast period).

Segment architecture — material typologies, application buckets and commercialization maturity ladders (note: this public brief omits segment figures; the full report provides the detailed split and unit economics).

Value chain map — supplier nodes, critical input dependencies, processing steps, and bottlenecks that influence COGS and scale‑up cadence.

Go‑to‑market playbooks — clinical field trial design, reimbursement navigation, and channel strategies for medical vs. industrial clients.

Competitive and partnership framework — profiles of incumbent and emerging players, IP landscape highlights, and acquisition target scoring guidelines.

Risk register and mitigation matrix — regulatory, raw material volatility, reimbursement headwinds and quality/scale risks with pragmatic responses tied to investment thresholds.

The market remains relatively fragmented at the top, with a small group of established medical device and material firms and several specialized innovators competing across clinical and industrial use cases. A concentration analysis indicates that the leading three and five companies together capture a modest portion of total market activity—enough to set standards on quality and regulatory expectations, but not sufficient to create entrenched monopolies. This fosters an environment where differentiated technology or superior go‑to‑market execution can rapidly translate to material commercial gains.

Advanced Medical Solutions Group PLC (UK) — A seasoned player in advanced wound care. For 2026 planning, their core strength in clinical channels suggests potential to expand hydrogel portfolios via adjacent formulations and strategic licensing rather than greenfield manufacturing.

Axelgaard Manufacturing Co. Ltd. (USA) — Known for AmGel hydrogels and diversified medical applications. Axelgaard’s manufacturing know‑how positions it to be a preferred partner for device OEMs seeking supply continuity and scale; they should lean into co-development agreements that embed their gels in sensing and stimulation platforms.

Cardinal Health (USA) — As a major distributor and device manufacturer, Cardinal’s role is pivotal for channel access and commercial rollout in clinical settings. Strategic options for Cardinal include exclusive commercialization partnerships or bundling hydrogel dressings with procedural consumable portfolios.

Hydromer Inc. (USA) — Specializes in hydrophilic coatings and self-healing functionality for devices. Their IP and coating capabilities make them a candidate for licensing and OEM supply relationships, particularly in applications where device biocompatibility and antifouling properties are paramount.

Gel4Med Inc. (USA) — An agile innovator delivering peptide‑based biomimetic matrices, with recent FDA 510(k) clearance and positive RWE publications. Gel4Med’s regulatory head start and clinical evidence base present a strategic playbook: accelerate selected clinical programs, lock downstream distribution partnerships, and selectively pursue capacity augmentation to meet hospital demand.

Alliqua Biomedical and Contura International — Both have focused hydrogel offerings. For these firms, the choice is between deepening clinical differentiation through outcome-driven trials or pursuing niche industrial applications where reimbursement constraints are less relevant.

Smith & Nephew and 3M — Large diversified manufacturers with significant channel reach. Their strategic advantage is rapid global deployment when integrating new gel formulations into existing wound‑care and medical device ecosystems; they also have the balance sheet to vertically integrate production where needed.

Clinical validation and commercialization: Gel4Med’s FDA clearance and subsequent RWE from a major academic medical center validate the path from bench to bedside for biomimetic hydrogel matrices. Firms with clinical-stage assets should prioritize pragmatic, outcomes-oriented trials to convert adoption into reimbursement conversations.

Materials science breakthroughs: Academic teams have reported self‑healing hydrogels with markedly improved mechanical performance, narrowing the gap between synthetic matrices and native tissue mechanics. This raises the bar for incumbents and creates opportunities for licensing or collaborative research agreements.

Innovative formulations for smart delivery: Work on stimulus-responsive polysaccharide gels highlights potential for combination products that deliver actives responsively—an attractive proposition for wound healing and controlled-release therapeutic strategies.

Regulatory and reimbursement friction: While accelerated pathways exist, stringent approvals and non-uniform reimbursement policies persist in major markets. Firms must budget for extended regulatory interactions and develop payer evidence dossiers in parallel with clinical adoption.

Raw material volatility: Price swings in polymers and specialist biomaterials can materially impact gross margins during scale-up. Hedging strategies, dual-sourcing and supplier development programs should be part of any 2026 manufacturing plan.

Quality and scale: Translational risk remains high. Laboratory-grade self-healing behavior does not automatically translate to reproducible manufacturing yields. Early investment in process development and quality systems reduces commercialization risk.

Prioritize clinical differentiation earlier: Convert laboratory performance into clinical endpoints that matter to payers and clinicians (e.g., time‑to‑closure, infection rates, device longevity). Use focused, pragmatic trials that generate usable health economic data.

Lock supply and optionality: Begin supplier qualification and long‑lead procurement in 2026. Where feasible, secure capacity options or toll‑manufacturing agreements to avoid ramp shocks.

Choose partnership models by channel: Medical device incumbents can pursue exclusive distribution or co‑branding; material innovators should evaluate licensing vs. bolt-on M&A depending on capital availability and strategic fit.

Invest in regulatory and reimbursement capability: Treat market access as a parallel investment to R&D. Early payer engagement and health economic modeling materially shorten the commercial adoption curve.

Scan for targeted acquisitions: Look for technology platforms that deliver differentiated mechanical performance or enable smart-release capabilities; these will have outsized strategic value as applications diversify beyond wound care.

For executives and investors, the PW Consulting Self-Healing Gel Market report translates scientific progress into rigorous near‑term commercial implications. It quantifies the growth runway, identifies where execution risk concentrates, and prescribes pragmatic moves to capture early market share while managing cost and regulatory complexity. The full report contains the detailed segment and regional intelligence, actionable financial scenarios, and supplier and partner scorecards required to operationalize plans in 2026.

For the complete dataset, segmented forecasts, and our bespoke implementation templates, access the full PW Consulting report and schedule a strategic workshop. Our advisors will walk through tailored scenarios for your portfolio and recommend a 12–24 month roadmap calibrated to your risk tolerance and capability set.

For detailed analysis of this topic, please visit the official page:Self Healing Gel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com