Experts Predict Cryogenic Air Separation Units to Drive Air Separation Plant Market Innovation

Other |

2026-06-04 10:19:58

As organizations plan capital allocation and technology roadmaps for 2026, superconducting magnetometers are emerging from a niche research tool into a commercially relevant measurement platform across medicine, geophysics, and advanced scientific programs. Our latest PW Consulting market model shows the market expanding at a compound annual growth rate (CAGR) of 7.7% over the 2026–2032 forecast window. After growing from a modest base in the early 2020s, the industry reached an estimated global market size of 24.2 Million USD in 2025 and is projected to approach approximately 40.7 Million USD by 2032 under the principal scenario.

Superconducting Magnetometer Market

Timing: Capital and procurement cycles for specialized sensing equipment often span 12–36 months from specification to deployment. The 2026 planning horizon is therefore the tipping point for organizations that need to align budget approvals with vendor roadmaps.

Superconducting Magnetometer Market

Technology risk mitigation: The market is characterized by rapid advances in sensor design (LTS vs HTS approaches), cryogen-free systems, and miniaturization. Understanding where technology trajectories converge allows R&D and product teams to hedge between platform investments and licensing opportunities.

Superconducting Magnetometer Market

M&A and partnership signaling: The landscape shows a handful of established suppliers alongside agile specialist vendors. For corporates and private equity, the report’s actionable target selection criteria and vendor scorecards shorten due-diligence timelines.

Operational resilience: Supply-chain constraints—specialized superconducting materials and cryogenic expertise—translate into long lead times and margin pressure. Procurement strategies informed by scenario analysis reduce cost surprises in 2026.

Transparent market sizing and forecasting methodology, with base-year reconciliation and upside/downside scenarios for 2026–2032.

Buyer personas and procurement playbooks for clinical, exploration, and research customers to inform channel strategy and technical pre-sales.

Technology roadmap mapping (LTS vs HTS, cryogen-free cooling, portable sensors) with likely adoption curves and R&D investment levers.

Vendor scorecards and a three-tiered competitive matrix that assess product breadth, IP, manufacturing resilience, and services capability.

Supply-chain risk heatmaps, cost-driver decomposition and suggested mitigation actions (e.g., supplier dual-sourcing, vertical integration scenarios).

M&A target shortlists, with financial model templates and integration checkpoints tailored for acquirers and strategic partners.

Commercial templates: pricing ladders, service-contract models, and field-deployable test plans to accelerate go-to-market execution.

The market features a mix of legacy instrumentation manufacturers and lean specialist vendors. Industry concentration is meaningful: the combined share of the top three suppliers stands at 48.5%, and the top five account for 62.3% — a structure that creates defendable leader positions while leaving room for targeted disruption.

Quantum Design Inc. (San Diego, USA) — Known for its high-end SQUID magnetometer platforms supporting DC, VSM and AC modes with superconducting magnets. Its systems emphasize field range and multi-modal measurement, which makes it a natural choice for advanced materials and physics labs.

STAR Cryoelectronics LLC (Santa Fe, USA) — Supplies both LTS and HTS SQUID sensors plus readout electronics. The company’s breadth across sensors and electronics positions it as an integrator for biomedical and geophysical customers seeking turnkey solutions.

Tristan Technologies Inc. (San Diego, USA) — Focuses on custom systems and field-ready HTS models for geophysical exploration. Its emphasis on liquid-nitrogen-cooled solutions addresses customers prioritizing operating-cost reduction in the field.

Supracon AG (Jena, Germany) — Active in both LTS and HTS domains and notable for recent deployment partnerships that bring ultrasensitive sensors into mineral exploration projects.

Cryogenic Limited (London, UK) — Offers cryogen-free configurations with integrated superconducting magnets, catering to laboratories that need high sensitivity without the logistical burden of traditional cryogens.

Magnicon GmbH (Hamburg, Germany) — Specializes in low-noise SQUID electronics and bespoke systems for precision measurement, appealing to research institutions with demanding signal-to-noise requirements.

ez SQUID (Netherlands) — Has launched compact SQUID sensors optimized for portability and integration, representing the first wave of true field-portable magnetometer options.

Recent vendor activity signals two parallel trends: (1) higher sensitivity and integration for large laboratory systems, and (2) a push toward portability and lower operating cost in field systems. Examples include a deployment partnership for advanced mineral exploration announced by a European vendor in early 2024, and the market entry of compact, portable SQUID sensors from a Netherlands-based specialist in 2025.

Funding tailwinds — Public programs are nudging adoption in research and applied settings. Notably, the EU’s Horizon Europe program has allocated substantial funding to quantum technologies, which indirectly supports demand for superconducting sensing platforms.

Input-cost pressure — The specialized materials and manufacturing processes for superconductors remain a high-cost factor. This affects both unit economics and the feasibility of large-scale commoditization in the near term.

Labor and expertise scarcity — Skilled talent in cryogenics and superconducting fabrication commands a premium, creating barriers for new entrants and driving outsourcing or regional centers of excellence.

Policy nudges — U.S. programs promoting advanced energy and grid modernization create downstream use cases for superconducting technologies, which can broaden addressable markets beyond traditional research and exploration customers.

Prioritize hybrid investments: Combine funding for flagship laboratory systems with small-batch development of portable HTS-enabled prototypes to capture both premium and field markets.

Adopt a supplier-risk mitigation program: Identify single-source dependencies for superconducting materials and institute dual-sourcing or inventory buffers for critical components.

Invest in services and aftermarket: Given lead times and specialized maintenance needs, service contracts and calibration offerings can deliver differentiated, recurring revenue streams.

Pursue targeted acquisitions: Look for sensor IP, cryogenics expertise or field-deployable system integrators to accelerate time-to-market and broaden application reach.

Forge research partnerships: Leverage public funding streams and university consortia to co-develop application-specific configurations that can be commercialized with lower R&D cost exposure.

Differentiate through total cost of ownership (TCO): Position cryogen-free and HTS-based solutions on operating-cost metrics—not just sensitivity—to appeal to budget-constrained field customers.

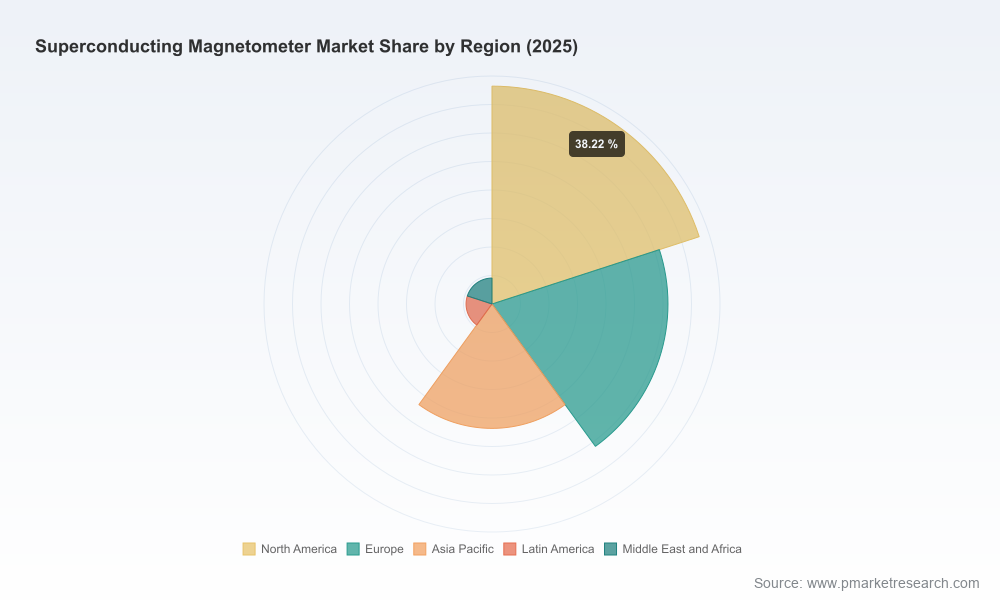

To preserve the commercial value of the full intelligence product, this release intentionally omits the report’s granular regional and application-level splits, detailed company market shares, and downloadable financial models. The full report contains proprietary segmentation tables, primary interview transcripts, and downloadable datasets that are essential for transaction-level decision-making. These assets are available via the PW Consulting report portal for organizations seeking actionable, exportable analytics and customizable models.

Our advisory offerings for the superconducting magnetometer sector in 2026 include bespoke strategy workshops, custom financial and sensitivity models, vendor due diligence, and M&A target screening. Clients engage us to translate market-level forecasts into executable plans—whether that’s a capital procurement decision, an R&D pivot, or a bolt-on acquisition to secure sensor IP and manufacturing capability.

For executives preparing budgets and strategic plans for 2026, this report functions as both an early-warning system and an execution playbook: it quantifies the growth runway (7.7% CAGR through the forecast horizon), maps technology and competitive inflection points, and prescribes practical moves to capture asymmetric value. To obtain the full dataset, vendor scorecards and scenario models, visit the PW Consulting report page or contact our industry team for a briefing and tailored roadmap.

For detailed analysis of this topic, please visit the official page:Superconducting Magnetometer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com