PW Consulting: Diesel Injection Market to hit USD 109,400M by 2032 at 5.5% CAGR

Other |

2026-07-08 09:14:21

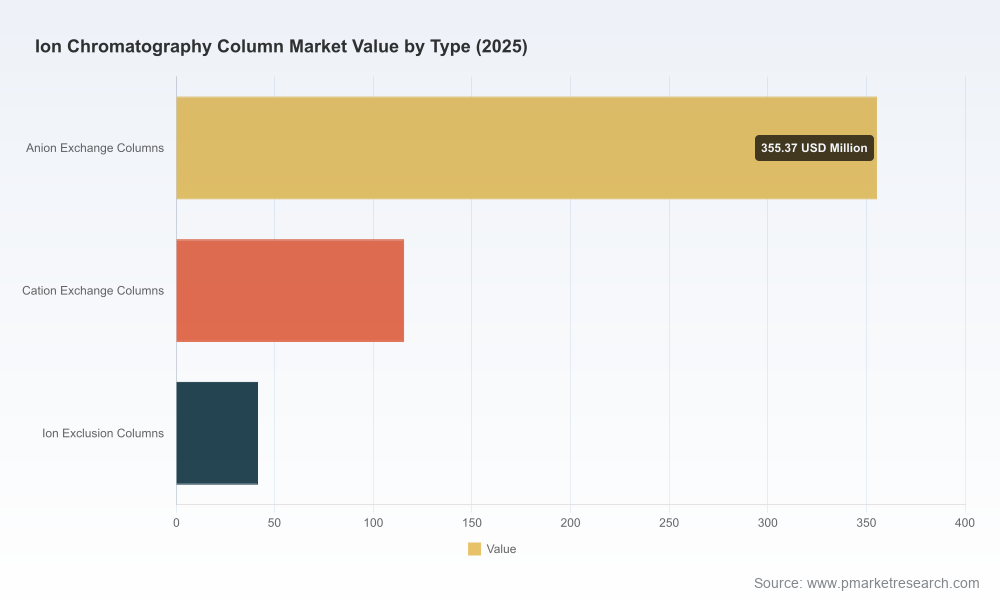

The global ion chromatography (IC) column market is entering a decisive inflection for enterprise strategy in 2026. PW Consulting’s latest market model places the industry at approximately USD 512.5 Million in 2025, with a forecast trajectory that reaches roughly USD 833.8 Million by 2032 — reflecting a compound annual growth rate of 7.24% through the 2026–2032 forecast window. Historical performance from 2020 to 2025 demonstrates steady expansion, driven by recurring consumable demand, regulatory-driven laboratory upgrades, and accelerating uptake of automated IC platforms.

Ion Chromatography Column Market

Note: the full report contains granular segmentation (by region, column type, and application) and price-point matrices. Those detailed splits are intentionally restricted in this briefing to preserve the full report’s strategic value and to direct readers to the source for complete datasets and downloadable tools.

Ion Chromatography Column Market

Demand drivers are converging: heightened environmental monitoring standards, broader compendial acceptance of ion chromatography in pharmaceutical testing, and expansion of food-safety protocols are all increasing laboratory throughput and recurring column consumption. On the supply side, advances in polymer-based media, microbore/high-efficiency column formats, and integrated automated platforms are shifting buyer preferences toward vendor ecosystems that can deliver validated workflows, software compliance and ongoing service.

Ion Chromatography Column Market

The market concentration metrics underline a structurally consolidated landscape: the top three suppliers command a meaningful share of industry revenue, and the five largest vendors account for an even larger proportion. This concentration creates both barriers and strategic openings — incumbents benefit from scale and channel reach, while challengers can compete by specializing in cost leadership, patented chemistries, or differentiated service models. For buyers, concentrated supplier power means negotiation leverage is context-dependent: high-volume consumables can be bundled for discounts, whereas validated, regulated workflows restrict rapid switching.

Recent vendor activity underscores a dual trend: platform innovation (Shimadzu’s Nexera IC) alongside catalog refreshes that codify product breadth (Metrohm and Shodex catalog releases in 2025). Competitive advantage in 2026 will accrue to vendors who combine validated workflows, software compliance, and reliable aftermarket supply.

Regulatory momentum is structurally altering procurement rationales. USP-NF modernization that recognizes ion chromatography in compendial chapters increases pharma’s willingness to adopt IC for compendial assays — but also raises the bar for method validation. Public-environmental standards (EPA methods and ISO references) and FDA expectations for data integrity mean that instrument-software ecosystems must support 21 CFR Part 11 controls and audit trails. These requirements create an opportunity for vendors that can demonstrate turnkey compliance packages, and raise switching costs for laboratories that invest in validated workflows.

Our Ion Chromatography Column Market report is structured to move organizations from insight to execution. Subscribers receive the full market model, downloadable vendor scorecards, negotiation playbooks, and workshop modules that we use with executive teams to translate findings into 90-day and 18-month operational plans. For firms considering M&A, we provide diligence-ready checklists and synergy estimates; for commercial leaders, we supply go-to-market scripts and pricing simulations tuned to the 2026 competitive landscape.

To preserve the actionable advantage of the research, this briefing omits the granular regional, type- and application-level splits and price-point matrices contained in the full report. Those segment-level datasets — which underpin supplier selection, SKU-level margin analysis, and regional prioritization — are available through our report portal.

For senior leaders planning 2026 investments, the PW Consulting Ion Chromatography Column Market report provides the data, frameworks, and practical tools to make defensible decisions within 30–90 days. Access to the full dataset, downloadable scenario engine, and bespoke advisory engagements is available through our report page. Contact PW Consulting for an executive briefing or to commission a tailored workshop that applies the report’s tools to your specific product, procurement, or M&A questions.

For detailed analysis of this topic, please visit the official page:Ion Chromatography Column Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com