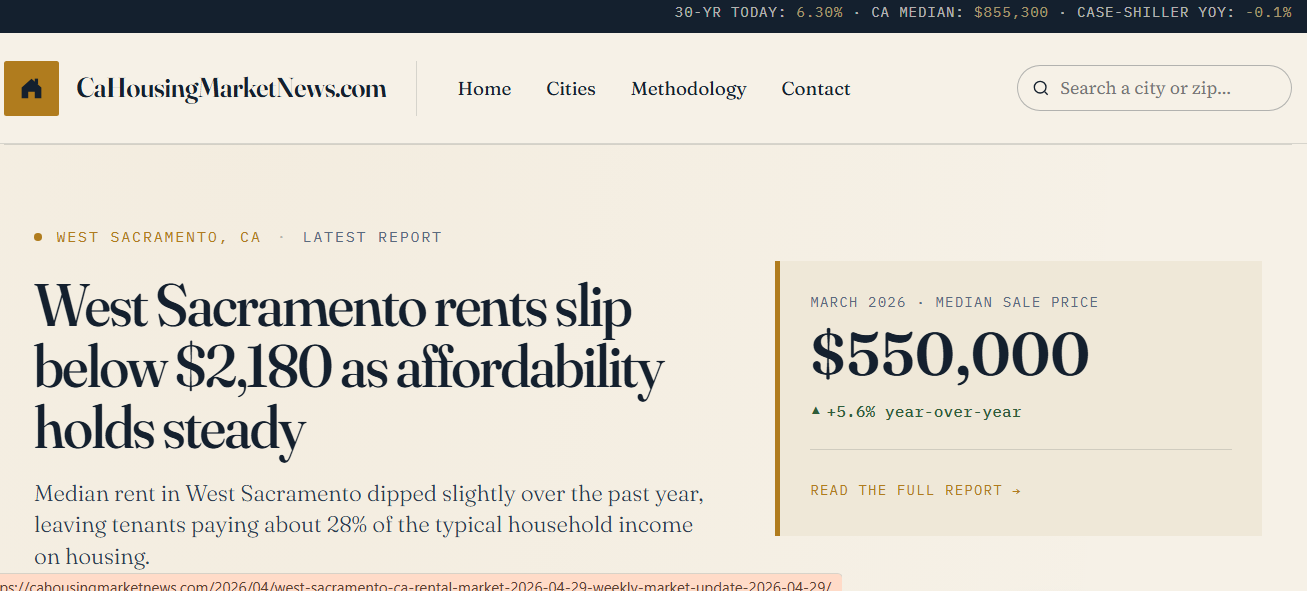

Virus Filtration Market Forecast: North America Leading Innovation in Bioprocessing

Health |

2026-06-26 13:02:07

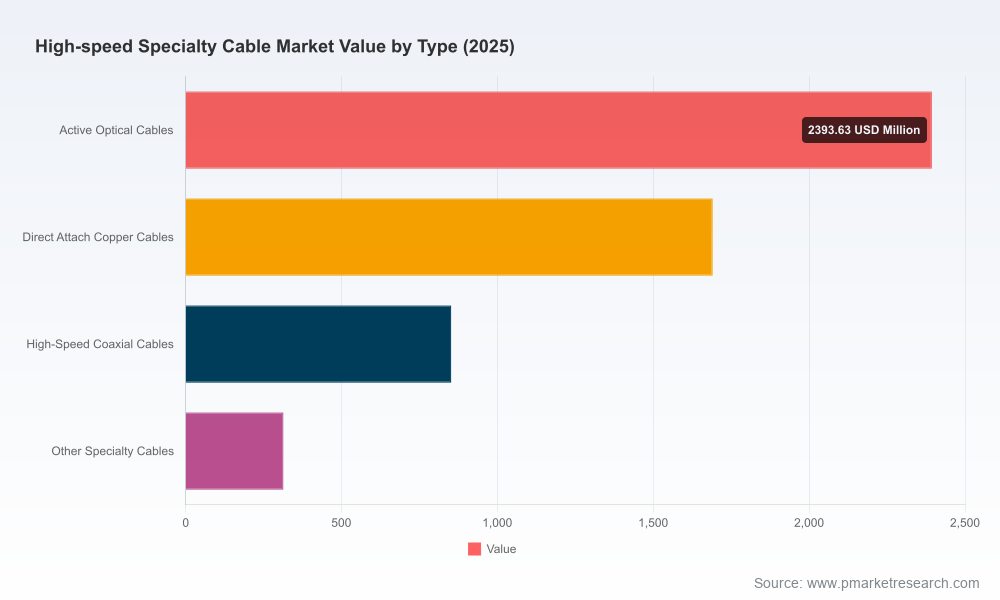

PW Consulting’s new High Speed Specialty Cable Market study (base year 2025; historical 2020–2025; forecast 2026–2032) reframes how procurement, product, and corporate strategy teams should approach high-throughput cabling decisions heading into 2026. The market has scaled rapidly over the past half-decade — rising from roughly USD 3.45 billion in 2020 to an estimated USD 5.25 billion in 2025 — and our scenario-driven forecasts show continued acceleration through the 2026–2032 horizon at a compound annual growth rate (CAGR) of 9.21%. By 2032 the market is expected to approach a near-doubling of 2025 scale.

High Speed Specialty Cable Market

Timing of investments: The convergence of stronger demand for high-density data links and new telecom deployments means capital allocation decisions in 2026 will shape competitive positioning for the rest of the decade. Delaying capacity expansions or technology refreshes can result in missed windows where pricing power and availability both favor the supplier or integrator who acted early.

High Speed Specialty Cable Market

Supplier selection and resilience: Supply-side concentration is material — the market exhibits a mid-level consolidation profile with the top three vendors controlling a meaningful share and the top five commanding over half of market revenues. That concentration creates both opportunities for scale players and risks for buyers who rely on a narrow supplier set.

High Speed Specialty Cable Market

Margin and cost management: Raw-material dynamics (notably copper and associated laminates) and policy shifts have elevated input cost volatility and created new pass-through decisions for manufacturers and their channel partners. Pricing discipline and sophisticated cost-indexing will be essential in 2026 to preserve margins.

Technology substitution and product mix: Adoption of optical assemblies and advanced cable interconnects for high-throughput computing and edge networking continues to accelerate. Product roadmaps that prioritize density, thermal behavior, and support for next-generation interface standards will command premium placement in customer RFQs.

Input-cost volatility: The supply chain is experiencing episodes of sharp raw-material price movements and sustained inflationary pressure on cable-specific inputs. These trends have lengthened supplier lead times and forced strategic buyers to rethink inventory strategies and hedging approaches.

Trade and regulatory friction: New trade measures and export-control tightening, particularly around copper-intense and electronic component value chains, have introduced jurisdictional sourcing and compliance overheads that must be baked into procurement and legal risk assessments in 2026.

Serviceable addressable market expansion: Growth in hyperscale data centers, the rollout of advanced telecom infrastructure, and rising adoption of high-reliability cabling in industrial and medical applications are expanding the commercial footprint for specialty high-speed cable suppliers.

For OEMs and hyperscalers: Prioritize supplier integration programs that lock down capacity and accelerate qualification cycles. Build co-development arrangements for higher-margin optical assemblies and cable-integrated modules to differentiate at the systems level.

For tier-1 cable manufacturers: Use 2026 to invest selectively in automation and high-density fabrication lines. Focus R&D on thermal management, miniaturization (micro-distribution), and interoperability to capture higher-value segments. Consider pricing policies that reflect pass-through mechanisms for volatile copper and laminate inputs.

For private equity and strategic investors: The sector’s mid-level consolidation and robust growth profile create carve-out and roll-up opportunities. Value creation will depend on buying disciplined manufacturing playbooks and accelerating digital customer channels for configuration and aftermarket services.

For procurement and supply-chain leaders: Reassess single-source agreements, create multi-sourcing corridors across geopolitical domains, and introduce procurement instruments tied to index-based cost adjustments and capacity release clauses.

Our competitive analysis synthesizes public filings, recent product launches, and facility investments to map who is positioned to lead the next wave of growth, and why.

Amphenol Corporation — with strong organic expansion in IT/datacom and interconnects, recent quarters show Amphenol leveraging scale to accelerate market share gains in high-speed interconnect solutions. Their investments in PCIe-capable and high-throughput cable architectures make them a partner of choice for systems integrators seeking end-to-end connectivity roadmaps.

Prysmian Group — a global breadth player with expansive manufacturing and service footprints, well-suited for infrastructure-scale projects. Their capability across fiber and specialty copper positions them to capture large telecom and energy-linked orders where end-to-end delivery is valued.

Nexans, Sumitomo Electric, and Furukawa Electric — each combines engineering strength with targeted product lines for high-frequency and fiber-centric applications. Expect competition in bespoke, high-reliability segments such as industrial and aerospace cabling.

Regional and niche specialists like LS Cable & System, Proterial Cable America, Southwire, SCC, and Samtec are executing differentiated plays: product innovation (micro-distribution fibers, Category 6A launches), near-market manufacturing, and specialty mil-spec or data-center-focused portfolios. These players will be attractive partners for customers needing speed-to-deployment and customization.

Large public companies reported outsized demand and record sales driven by datacom and high-speed interconnect lines, underlining a strong revenue runway for suppliers focused on IT and networking.

Targeted product introductions — from category upgrades to micro-distribution fiber families — show the industry is prioritizing density and backward-compatible performance improvements, which will matter in procurement specifications in 2026.

Selective facility expansions and capital commits in specialty wire emphasize an industry pivot to reshoring and capacity redundancy against trade-policy friction and raw-material bottlenecks.

Price shocks and trade measures observed in recent quarters have turned theoretical supply risks into executable operational levers. Our recommended 90‑to‑180 day actions for leadership teams:

Institute layered sourcing strategies that combine global and nearshore suppliers to mitigate tariff and export-control exposure.

Adopt dynamic pass-through clauses in long-term supplier agreements and pilot index-linked contracts to stabilize margin outcomes without losing competitiveness on bids.

Accelerate qualification protocols for secondary suppliers and maintain strategic buffer inventory for components subject to the steepest price and lead-time volatility.

This report is designed as an operational playbook, not only a market overview. It contains:

Scenario-driven demand models (base, upside, downside) and an accessible financial model for 2026 planning, with sensitivity toggles for input-cost and demand shocks.

Supplier scorecards and risk matrices that combine capacity, technology readiness, and geopolitical exposure into actionable shortlists for sourcing teams.

Commercial negotiation templates, recommended pricing pass-through clauses, and an MRO-to-CapEx prioritization framework tailored to cable manufacturing realities.

Technology roadmaps and product-pocket guidance (optical assemblies, high-speed copper variants, micro-distribution) that translate standards trajectories into procurement and R&D requirements.

Investment and M&A heatmaps identifying niches where consolidation will create outsized returns, together with valuation benchmarks and integration risk checklists.

Consistent with the “trailer” principle, this release highlights strategic findings while reserving the report’s granular split tables, supplier-level revenue estimates, and downloadable models for the full publication. Those deliverables include regional and application-level breakdowns, product-type revenue curves, and a downloadable Excel model that decision teams can use directly in Board and CapEx reviews.

Entering 2026, the high speed specialty cable market presents a clear but complex growth opportunity: robust end-market demand and favorable technology trends intersect with raw-material volatility and geopolitical constraints. Organizations that treat 2026 as the year to lock capacity, diversify supply, and invest in higher-value product capabilities will harvest structural advantages as the market expands toward the end of the decade.

For a guided briefing, proprietary access to the report, or to request the interactive model and supplier scorecards, visit our report page or contact PW Consulting’s High Speed Specialty Cable team. Our analysts are scheduling limited executive briefings through Q3 2026 to translate findings into bespoke procurement and M&A execution plans.

For detailed analysis of this topic, please visit the official page:High Speed Specialty Cable Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com