Adopting HCM Software Market: Strategic Imperatives for 2026 — PW Consulting Insight Preview

Executive summary

As organisations rethink workforce strategy after successive waves of remote/hybrid work, privacy regulation tightening, and rapid AI feature maturation, the Human Capital Management (HCM) software market is entering a pivotal phase. PW Consulting’s new Adopting HCM Software Market report—anchored on a 2025 base year and a 2026–2032 forecast horizon—shows sustained expansion driven by cloud adoption, AI-enabled talent workflows, and rising demand for compliance-first architectures. The market is projected to continue growing at a compound annual growth rate (CAGR) of 9.24%, reflecting both steady replacement cycles and accelerated refresh activity among mid-to-large enterprises.

Adopting Hcm Software Market

Market trajectory and 2026 inflection points

After a period of steady recovery and investment, total industry revenues reached USD 31,520.45 Million in 2025 and are forecast to exceed USD 34,600 Million in 2026. Beyond the headline growth, two dynamics mark 2026 as a decision-making inflection year for buyers and vendors alike:

Adopting Hcm Software Market

- Regulatory acceleration: New privacy obligations — notably changes to CCPA effective January 2026 and ongoing GDPR expectations — raise the bar for automated decision-making governance in HR contexts. Organisations must now reconcile automated selection, assessment, and profiling workflows with demonstrable privacy risk assessments and DPIAs.

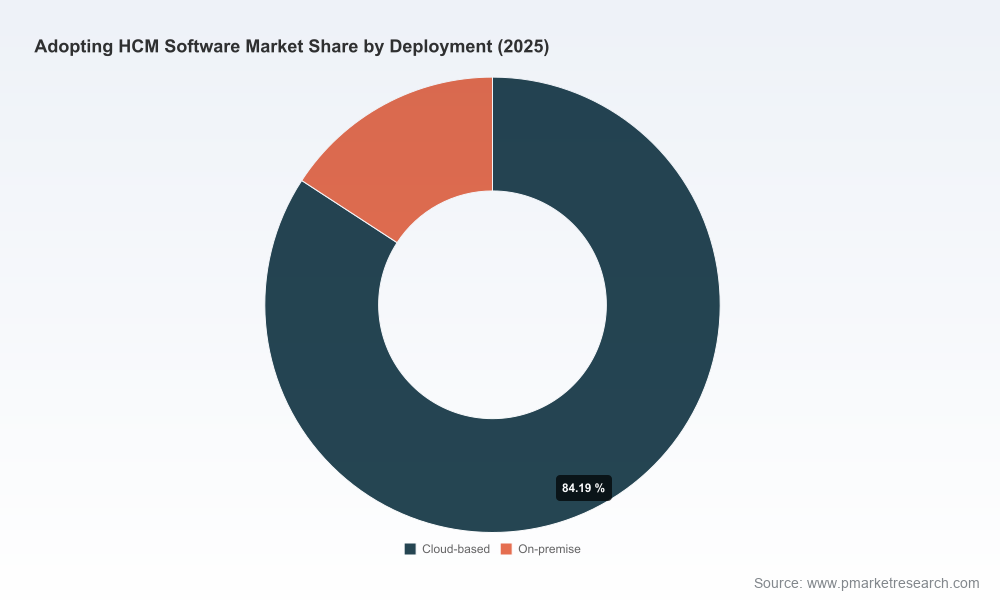

- Value-realisation pressure: Organisations report material waste in cloud spend and persistent gaps between deployed functionality and realised business outcomes. Combined with evidence that cloud deployments materially reduce infrastructure costs versus on-premise alternatives, procurement is shifting from “feature checklists” to measurable TCO, cloud efficiency, and ROI guarantees.

What the report delivers — practical, actionable intelligence

This report is deliberately operational. It goes beyond vendor ranking to deliver tools that procurement, HR leaders, and CIOs can use immediately to shape 2026 initiatives:

Adopting Hcm Software Market

- Validated market sizing and bottom-up forecasts (2020–2032) with scenario variants for macroeconomic sensitivity and accelerated AI adoption.

- A buyer’s playbook that aligns procurement objectives with technology economics — encompassing TCO models, break-even timelines, and risk-adjusted ROI templates.

- Implementation roadmaps and integration patterns for common enterprise environments, including identity management, payroll feeds, and learning-management systems.

- Regulatory compliance checklists and AI governance frameworks tailored to HR use cases — privacy impact templates, documentation requirements, and audit-ready controls.

- Cloud cost-optimization prescriptions: vendor-agnostic diagnostics to recover wasted SaaS spend and governance guardrails for rightsizing, subscription management, and multi-cloud hosting choices.

- Organisational change templates — stakeholder maps, training curricula, and adoption KPIs that tie platform deployment to measurable people outcomes.

Competitive landscape — how to read vendor intent and capability in 2026

The HCM vendor field remains a mix of large, integrated suite providers, specialised talent platforms, and nimble mid-market entrants. Market concentration indicates that top-tier vendors continue to command notable scale while a second wave of focused players competes on speed, usability, or vertical specialization. Understanding vendor intent—product roadmaps, go-to-market focus, and partnership strategies—is now as important as feature parity.

- Workday, Inc. — Market leader posture reinforced by deep investments in AI for employee experience and specialty government capabilities. Recent product launches targeting federal HR workflows and an AI-driven recognition partnership signal an aggressive push into verticalized, high-complexity deployments where workflow automation and compliance matter.

- SAP SE — SuccessFactors continues to play to SAP’s strengths around global compliance and integrated enterprise suites. SAP’s value proposition is strongest where customers require broad global payroll and local compliance coverage embedded into ERP-led landscapes.

- Oracle Corporation — Oracle’s cloud HCM offerings emphasize scalability and convergence with broader enterprise data stacks. Expect Oracle to pitch unified data models and AI-enabled talent insights as differentiators for complex, international enterprises.

- ADP, Inc. — ADP’s consolidation of workforce management and payroll into a unified suite reflects a strategic focus on payroll-centric workloads and multinational payroll complexity — an attractive option for organisations prioritising global payroll consistency.

- UKG, Ceridian, Paycom and other payroll/WM specialists — These vendors underscore strong capabilities in time and attendance, payroll accuracy, and workforce optimisation. They are contenders for organisations where operational workforce management drives the primary business case.

- Mid-market and SMB-focused vendors (BambooHR, Rippling, Zoho, Paylocity) — Compete on speed of deployment, UX, and integration with modern IT toolchains. They are particularly compelling where time-to-value and lower implementation complexity are priorities.

- Platform plays (Microsoft, Infor, Cornerstone) — These vendors leverage adjacent enterprise suites, learning ecosystems, and industry-specific configurations to attract customers seeking cross-product synergies.

PW Consulting’s vendor analysis in the full report pairs capability mapping with procurement scenarios — showing when a best-of-breed layered approach outperforms vendor consolidation, and when suite consolidation is the lower-risk path for 2026 budgets.

Recent vendor activity to watch (context for procurement teams)

- Workday’s 2025/2026 releases demonstrate a pattern of rapid feature expansion and targeted verticalisation — expect more role-specific AI agents and outcome-focused modules.

- ADP’s unified workforce suite rollout signals intensified competition in global payroll orchestration and workforce analytics.

- Across the vendor landscape, partnerships and micro-acquisitions are increasingly used to close capability gaps (recognition, learning, analytics) rather than building end-to-end modules in-house.

Priority recommendations for 2026 decision-makers

Our strategic recommendations are built for leaders with finite budgets and high expectations for measurable workforce outcomes.

- Define outcome-first success metrics before vendor selection. Map desired business outcomes (time-to-hire, turnover reduction, payroll error rates) to short- and medium-term KPIs and require vendors to commit to baseline metrics in pilot contracts.

- Treat AI and automation as governed capabilities, not optional add-ons. Require DPIAs and algorithmic accountability clauses during procurement; include periodic independent audits in SLAs where automated decisions affect hiring, promotion, or remuneration.

- Pursue cloud efficiency diagnostics as part of any renewal. With majority adoption clearly in cloud deployments, recoverable waste in SaaS subscriptions and hosting explains a significant portion of unrealised value—allocate budget to immediate optimisation before committing to new modules.

- Use scenario-based contracting. Include flexible capacity and modular termination clauses to avoid overcommitment; this is especially important as feature sets evolve rapidly and workforce strategies pivot.

- Align IT, HR, and Procurement on integration and data governance requirements up-front. Integration failures remain the most common source of delayed ROI.

How to use this report in your 2026 planning cycle

PW Consulting’s report is structured to be a working document for your 2026 planning cycle:

- Executive briefings and board-ready slides summarise strategy implications and investment priorities.

- Procurement-ready templates and RFP scorecards shorten vendor evaluation timelines while increasing negotiation leverage.

- Implementation blueprints and vendor-specific contingency plans reduce deployment risk and provide measurable adoption milestones.

Next steps — access to the full intelligence

This preview highlights strategic takeaways and operational imperatives without disclosing the granular splits, proprietary vendor scoring, and region-by-region models that procurement teams need when signing 2026 contracts. The full PW Consulting Adopting HCM Software Market report contains those datasets, interactive TCO models, and vendor playbooks — essential for teams that must choose and mobilise an HCM platform this year.

To obtain the complete report, data tables, and scenario workbooks, visit the PW Consulting report landing page or contact our advisory team for a tailored briefing and implementation workshop. PW Consulting will support rapid translation of report insights into procurement RFPs, TCO negotiations, and compliance-ready deployment plans for 2026.

For detailed analysis of this topic, please visit the official page:Adopting Hcm Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com