Resistive Random-Access Memory (ReRAM) Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-04 10:31:13

PW Consulting’s newest market intelligence brief on the Portable Keratometer market captures a sector moving from niche portability to mainstream clinical relevance. Our analysis shows the market reaching approximately USD 73.15 Million in 2025 and, under current dynamics, tracking to roughly USD 115.5 Million by 2032 — a compound annual growth rate of about 6.75% across the 2026–2032 forecast window. The growth trajectory reflects both technology maturation and expanding clinical use-cases outside traditional clinic walls.

Portable Keratometer Market

This press-style preview highlights the report’s strategic value for 2026 decision-making: how to prioritize R&D, shape M&A pipelines, structure go-to-market models, and manage regulatory execution. The aim here is to provide clear, actionable perspective while reserving detailed segment-level tables and proprietary scenario outputs for the full report on PW Consulting’s portal.

Portable Keratometer Market

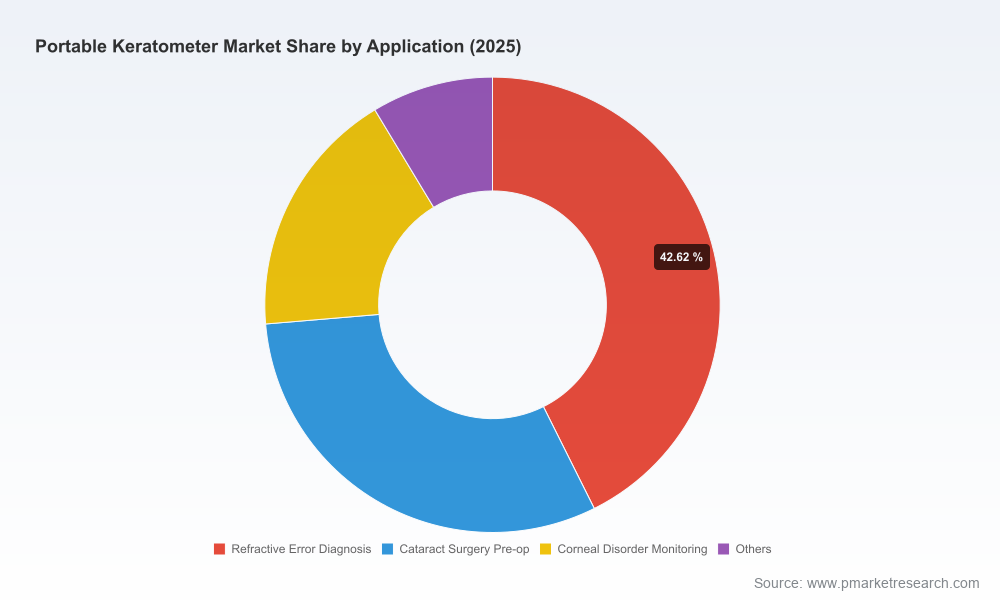

Shift from accessory to core diagnostic tool: Portable keratometers are no longer solely for outreach or low-resource environments. They are integrating into peri-operative workflows (e.g., cataract biometry), mobile refraction services, and tele-ophthalmology hubs—expanding addressable demand.

Portable Keratometer Market

Technology convergence: Handheld keratometers are converging with wavefront aberrometry, biometry suites, and cloud-enabled software platforms. This convergence creates product differentiation opportunities beyond hardware pricing—software, analytics, and service will drive share gains.

Consolidation and concentration: Market concentration is meaningful. The top three vendors account for roughly half of the market, and the top five approach two-thirds—creating a competitive dynamic where scale, channel reach, and portfolio breadth matter for 2026 winners.

Regulatory and standards pressure: Devices in this category are regulated as Class II under FDA guidance and fall under ISO 15004-series test expectations. In Europe, MDR conformity and post-market surveillance are non-negotiable. These regulatory realities materially affect go-to-market timelines and total cost of ownership.

Prioritize software-enabled differentiation: Buyers are increasingly valuing integrated workflows and analytics—products that reduce refraction cycle time or improve surgical planning win preference. Investing in companion apps, cloud data services, and APIs delivers defensibility.

Channel strategy refinement: The path to customer in 2026 is hybrid. Direct sales for high-complexity, bundled offerings; distributors and NGO partnerships for volume and outreach. Companies should model revenue by channel to avoid margin erosion as scale increases.

Regulatory-first product roadmaps: Given the Class II/IIa classifications and explicit standard requirements, embed regulatory submissions and post-market surveillance costs into product business cases from day one. A 510(k) roadmap can be a gating factor for time-to-market and pricing strategy.

Field performance and lifecycle economics: For many buyers (NGOs, outreach clinics, mobile surgical units), ruggedness, battery life, and calibration uptime matter more than marginal accuracy gains. Companies optimizing total cost of ownership will command procurement preference.

Selective consolidation and alliances: With concentrated market share at the top, medium-sized vendors should evaluate bolt-on M&A to acquire software capabilities, access to reimbursement channels, or to expand into complementary diagnostic categories.

Our competitive analysis profiles incumbent OEMs, emergent specialists, and regional innovators. Highlights include:

Micro Medical Devices (United States): Known for portable biometry and keratometry probes (e.g., PalmScan PRO and K2000), the company is demonstrating the operational value of integrated portable biometry, shown in mission deployments that validate field reliability and workflow efficiency.

PlenOptika (United States): A technology-driven challenger, offering handheld solutions that combine wavefront aberrometry and keratometry. Recent software platform upgrades (early 2025) underscore the importance of mobile software ecosystems as a competitive lever.

NIDEK (Japan) and Marco (United States): These established ophthalmic manufacturers are leveraging brand credibility and distribution networks to position portable ARK/keratometry products for peri-operative and mobile-use cases. Their strategic advantage lies in portfolio breadth and clinician trust.

Devine Meditech (India) and regional entrants: Cost-competitive handheld instruments from Asia are driving affordability, widening global adoption in emerging markets and mission-driven care models.

Reichert (AMETEK) and Huvitz: As part of broader diagnostic portfolios, these players present bundling and service-guarantee value propositions that are compelling for multi-device purchasers.

Recent industry moves corroborate our thesis. Product upgrades that focus on companion apps and analytic workflows (e.g., PlenOptika in early 2025) and real-world mission deployments (e.g., Micro Medical Devices in late 2025) are practical proof-points: buyers want durability plus smart workflows, not just compact hardware.

FDA 510(k) dynamics: Portable keratometers are regulated under Class II guidance frameworks. For vendors targeting the U.S. market, premarket strategy and predicate selection materially affect approval timelines and capex burn. Engage regulatory specialists early and plan for iterative submissions.

ISO and test protocols: Compliance with ophthalmic instrument standards (e.g., ISO 15004-series) is both a market access and procurement differentiator. Vendors must align design verification to recognized tests to expedite approvals and facilitate hospital procurement.

EU MDR implications: For European market continuity, maintain robust technical files, vigilance systems, and post-market studies. Noncompliant firms face extended time-to-market and reputational risk among purchasing groups.

This press preview distills strategic direction; the full report is designed for executable planning in 2026. Core deliverables include:

Market sizing and calibrated forecasts with scenario splits that model demand under divergent adoption curves and price erosion paths across the 2026–2032 window.

Competitor product and capability matrix capturing form factor, measurement modalities, software features, and channel footprints—intended to inform product roadmaps and acquisition screens.

Procurement playbooks for hospitals, NGOs, and mobile clinics that outline selection criteria, total cost of ownership templates, and service contract benchmarks.

Regulatory and standards checklist with estimated timelines and cost buckets for key geographies and submission strategies for incremental feature updates.

Go-to-market scenarios and a partnership map recommending distributor archetypes and clinical trial partners tailored to mid-size and large vendors.

For product leaders: Lock in a software roadmap that prioritizes interoperability and cloud analytics. Differentiate on clinician workflow impact rather than marginal hardware specs alone.

For commercial leaders: Design a hybrid channel strategy and pilot bundled offers (device + service + analytics) in at least two markets to test elasticity before scaling.

For M&A teams: Target assets that add software IP, mobile deployment capabilities, or regional distribution—these accelerate share gain faster than greenfield scale-up.

For regulatory and quality teams: Prioritize post-market surveillance tooling and plan for ongoing conformity assessments under MDR and recognized ISO standards to avoid time-to-market disruptions.

For investors: Use concentration metrics and product differentiation as core filters—companies with strong software ecosystems and validated field deployments offer better defensibility in an increasingly concentrated market.

Portable keratometers are at an inflection point: the market is expanding, concentration is rising, and non-hardware capabilities are becoming the decisive battleground. For 2026, executives should treat portable keratometer strategy as both a product and platform decision—align R&D, regulatory, and commercial investments to the cross-cutting demand drivers outlined here.

PW Consulting’s full Portable Keratometer Market report (base year 2025; historical 2020–2025; forecast 2026–2032) provides the granular segment analyses, competitor benchmarking, and executable templates necessary to convert these insights into 2026 action items. Download the complete study from our report page to access the proprietary regional and application breakouts, price and unit forecasts, and vendor-by-vendor product matrices that support immediate strategic moves.

For detailed analysis of this topic, please visit the official page:Portable Keratometer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com