Foot Orthotic Insoles Market: Size, Share, and Future Growth

Other |

2026-06-08 14:36:31

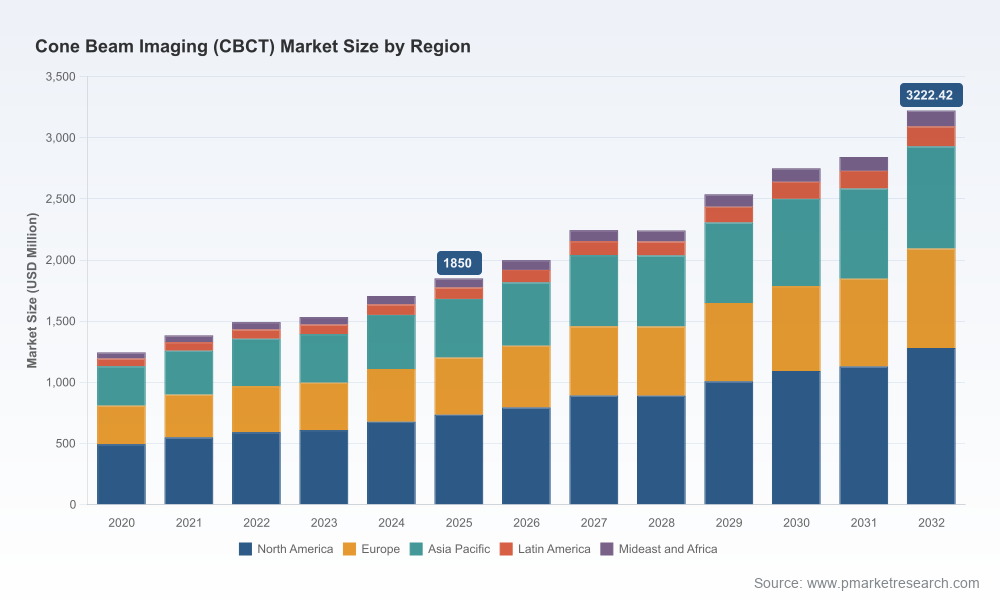

PW Consulting presents a focused industry brief based on our forthcoming Cone Beam Imaging (CBCT) Market report. As organizations prepare capital allocations and product strategies for 2026, CBCT is shifting from a point-solution into a platform-driven imaging category—driven by steady market expansion, accelerating AI software validation, and persistent downstream trade-offs between clinical value and reimbursement. Our model shows the global CBCT market expanding from USD 1,244.61 Million in 2020 to USD 1,850.0 Million in 2025, and forecasts growth to USD 1,999.08 Million in 2026 and USD 3,222.42 Million by 2032 at a compound annual growth rate (CAGR) of 8.25% over the forecast horizon. Market concentration remains material (CR3: 58.4%; CR5: 79.2%), signaling continued vendor consolidation and scale advantages for incumbent OEMs.

Cone Beam Imaging Cbct Market

Capital allocation: Providers and hospital systems will have to weigh CBCT investments against other imaging priorities. Our analysis identifies where unit economics and utilization thresholds justify acquisition vs. shared-service models.

Cone Beam Imaging Cbct Market

Product strategy: OEMs should prioritize modular platforms that enable AI-enabled software uptakes, multi-field-of-view (FOV) flexibility, and workflow integration to preserve value in competitive procurement scenarios.

Cone Beam Imaging Cbct Market

M&A and partnership timing: With a concentrated vendor set and accelerating software validation, 2026 is a strategic inflection point to evaluate tuck-ins (software/AI) and strategic alliances that capture cross-selling opportunities.

Regulatory and reimbursement playbooks: FDA clearances for AI diagnostic modules are reducing regulatory ambiguity, but reimbursement policies lag—affecting uptake curves and capital recovery timelines.

Our full report is structured to be directly actionable for C-suite and business development teams. Highlights include:

Top-down and bottom-up market sizing with scenario modeling (base year 2025; historical window 2020–2025; forecast 2026–2032) — including sensitivity tests across utilization, pricing, and reimbursement scenarios.

Vendor playbooks and product-matrix mapping — comparative assessment of hardware platforms, software ecosystems, AI-readiness, service models, and price positioning.

Commercial go-to-market frameworks — segmentation of buyer personas (private dental groups, hospital radiology departments, ambulatory surgical centers, specialty orthopedics), procurement triggers, and recommended commercial KPIs for 12–36 month rollout plans.

CapEx optimization tools — ROI and payback calculators that factor device utilization, per-scan billing variables, maintenance contracts, and staffing costs.

Regulatory & reimbursement intelligence — a roadmap for navigating Class II FDA pathways for hardware and 510(k) clearances for software modules, plus a payer engagement checklist to accelerate coverage discussions.

M&A & partnership diagnostic — identification of capability gaps across hardware and AI, valuation heuristics, and integration risk matrices tailored for strategic acquirers and financial sponsors.

Note: To preserve our clients’ commercial advantage, detailed segment-level tables (regional splits, application-by-application pricing ladders, and granular market-share cells) are summarized in the paid report and not reproduced here.

AI validation and regulatory acceptance: 2025–2026 saw multiple clearances for AI modules supporting 3D dental analysis. These approvals materially reduce integration risk for vendors and create new monetizable software revenue streams tied to subscription and per-use models.

Clinical demand and modality substitution: CBCT continues to displace select conventional imaging uses where 3D detail materially improves diagnostic confidence—implantology, orthodontics, endodontics, and certain maxillofacial indications—altering service-line revenue mixes for clinics that adopt earlier.

Reimbursement friction: A persistent patchwork of limited, procedure-specific reimbursement remains a headwind. Providers should run conservative utilization assumptions and actively engage payers to translate clinical utility into billable codes.

Hospital CapEx and shared-service adoption: Larger institutions are investing in scalable, high-capacity CBCT units as part of imaging modernization; for OEMs, selling into hospital systems requires enterprise-grade service, cybersecurity, and integration assurances.

Consolidation and competitive pressure: With CR3 at 58.4% and CR5 at 79.2%, scale economies in production and service deliver meaningful margins. Niche specialists and software-first entrants will need differentiated value propositions or alignment with incumbents to scale.

The CBCT vendor ecosystem combines large dental OEMs with specialized imaging and software firms. Key companies we assess (selected examples) include:

Dentsply Sirona (Charlotte, NC, USA): Established OEM with integrated 3D platforms and treatment-planning software. Strengths lie in channel breadth and established dental consumables relationships that facilitate cross-sell.

Planmeca Oy (Helsinki, Finland): Known for low-dose Viso and ProMax series with integrated facial scanning and strong workflow tools. Recent launches target North American expansion, underscoring product localization strategies.

VATECH Co., Ltd. (Hwaseong-si, South Korea): Competitive on cost-to-feature trade-offs, with auto-switching and high-resolution options appealing to price-sensitive clinical buyers.

Carestream Dental (Atlanta, GA, USA): Focused on multi-FOV scanners and AI-enhanced imaging, suitable for clinics that require flexible field sizes and software-augmented diagnostics.

J. Morita MFG. CORP. (Kyoto, Japan) & PreXion (Japan): Both emphasize high-resolution imaging and clinical use-cases (endodontics, radiology) where image fidelity is a purchase driver.

Cefla S.C. (NewTom, Imola, Italy): Offers CBCT lines across dental and medical niches with emphasis on diagnostic quality and cross-specialty applications.

CurveBeam AI, Ltd.: Specialist in orthopedic and weight-bearing CBCT, combining device differentiation with AI for extremity imaging—illustrating the value of focus versus scale.

Asahi Roentgen Ind. Co., Ltd. (Japan): Compact and reliable systems targeting practices where footprint and uptime are critical procurement criteria.

Strategic implication: incumbents must protect hardware margins while building recurring-software revenue. New entrants can win by specializing (e.g., weight-bearing extremity imaging) or by delivering best-in-class AI that demonstrably improves throughput and outcomes.

Multiple AI approvals (2025–2026): Several vendors secured FDA 510(k) clearances for AI tools that analyze 3D datasets—lowering a key barrier for clinical deployment of AI-assisted workflows.

Product launches and market entries: Notable device launches targeting the North American market are reshaping procurement conversations and increasing competitive intensity at the high end.

Clinical platform consolidation: Increasingly, clinics evaluate CBCT as part of a broader digital ecosystem (intraoral scanning, practice management, and AI analytics)—favoring vendors that offer integrated solutions or open APIs.

Prioritize AI-enabled product roadmaps: Allocate R&D and commercial focus to interoperability and validated AI tools that improve diagnostic throughput and billing justification.

Negotiate bundled service agreements: For large buyers, create multi-year service and upgrade contracts that reduce procurement friction and secure recurring revenue.

Engage payers proactively: Build evidence dossiers (health-economic models, utilization studies) to support coverage and coding discussions—this materially shortens adoption cycles in reimbursement-constrained markets.

Target hospital shared-service deployments: Focus enterprise sales teams on integrated solutions (cybersecurity, IT integration, service SLAs) where procurement decisions are centralized.

Pursue targeted M&A and partnerships: Software and AI capabilities represent the most immediate leverage points; smaller acquisitions can accelerate go-to-market and expand addressable use-cases.

Adopt staged-capex models for buyers: Use our ROI tools to evaluate phased deployments (single-unit trial → fleet roll-out) to reduce adoption risk and improve brand referenceability.

Think of the full report as a playbook: it supplies the granular market splits, price curves, regional and application-level demand matrices, and vendor scorecards you need to build investment memos, go-to-market plans, or M&A thesis documents. In keeping with our “trailer” approach, this preview intentionally omits detailed segment-level cells and proprietary supplier-by-supplier market-share percentages. Subscribers and clients receive the full dataset, model files (editable), and an executive workshop to translate findings into an operational roadmap for 2026.

For board-level briefings, tailored market-entry scenarios, or access to the complete dataset and modeling tools, contact PW Consulting’s medical imaging practice. Our team will run a rapid-read workshop and deliver a customized decision package aligned to your strategic horizon for 2026.

For detailed analysis of this topic, please visit the official page:Cone Beam Imaging Cbct Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com