Genetic Engineering Plant Genomics Market Size, Share, Demand & Forecast Insights

Other |

2026-05-22 08:42:00

PW Consulting's latest market research on Disposable Alcohol Wipes frames 2026 as an inflection year for manufacturers, distributors, and strategic investors. After a period of turbulence between 2020 and 2023, the global market shows a clear recovery trajectory: total industry revenue moved from roughly USD 855 million in 2020 down into the mid-600s by 2023, rebounding to approximately USD 723 million in 2025. Our base-year analysis (2025) and forward-looking model forecast a compound annual growth rate (CAGR) of 5.48% across the 2026–2032 horizon, projecting an industry north of USD 1,050 million by 2032. These headline dynamics mask meaningful variation beneath the surface — variation that will determine winners in 2026 and beyond.

Disposable Alcohol Wipes Market

Revenue momentum and margin pressure are disentangled: growth is re-emerging, but input cost volatility and regulatory friction mean top-line growth will not automatically translate to margin expansion.

Disposable Alcohol Wipes Market

Product and channel strategies must shift from short-term volume plays to resilient portfolios that balance premium hospital-grade, regulated prep-pad products and lower-margin, high-volume personal care formats.

Disposable Alcohol Wipes Market

Supply-chain risk management and regulatory readiness are now strategic levers — not operational afterthoughts — when assessing new investments, contract manufacturing, or go-to-market moves in 2026.

The overall pattern across 2020–2025 shows an industry that contracted sharply during the pandemic tailwinds and supply disruptions, then rebalanced to a steadier growth path into 2025. In our forecast baseline, the market grows from about USD 755 million in 2026 and accelerates toward the forecast horizon, reaching approximately USD 1,050 million by 2032 under the central-case CAGR of 5.48%. This recovery is being supported by a mixture of renewed institutional hygiene investments, growing consumer hygiene awareness in key urban markets, and increased product innovation — especially around sustainable substrates and faster-acting disinfectant chemistries.

However, the headline growth conceals two persistent constraints. First, raw-material cost volatility is significant: isopropyl alcohol (IPA) comprises a very large share of raw-material cost and has experienced year-over-year price swings that can erode margins quickly. Second, substrate supply (non-woven polypropylene/polyester) remains sensitive to petroleum-price cycles and episodic supply disruptions. Together, these cost drivers mean manufacturers with stronger procurement strategies and vertically integrated sourcing will have disproportionate advantage in 2026.

Regulation is a de facto part of product strategy for alcohol wipes. Disinfectant wipes are regulated as antimicrobial pesticides in several jurisdictions and require registration when efficacy claims are made; certain alcohol-impregnated prep pads are governed under OTC drug or medical-device frameworks that impose sterility and manufacturing controls. Disposal and solvent-contaminated waste rules add complexity for large-scale institutional buyers and end-of-life claims.

For 2026 planning this means: anticipate multi-month registration timelines, bake compliance costs into product pricing models, and differentiate on verified environmental claims where regulators and large buyers demand verifiable disposal pathways. The regulatory environment also creates barriers to entry that can be selectively leveraged by incumbent suppliers with compliance infrastructure.

The market sits at a medium level of concentration: our analysis shows the top three suppliers together account for a meaningful minority of market share, and the top five consolidate further. This structure produces a competitive dynamic where scale and specialization coexist. Large branded players combine R&D, regulatory muscle, and route-to-market strength, while regional and contract manufacturers compete on cost and speed-to-shelf.

Nice-Pak Products: long-standing innovation track record in wet wipes and hospital-grade formats. Their historical first-mover advantages in disinfecting wipes create continued relevance for institutional procurement teams.

PDI Healthcare: focused specialization in infection-prevention products and medicated prep pads. Their deep clinical relationships and portfolio of germicidal wipes make them a default partner for healthcare systems prioritizing validated efficacy.

Clorox: brand strength, institutional lines (CloroxPro/Clorox Healthcare), and an established commercial footprint that supports premium pricing and proprietary formulation claims.

Ecolab: notable for recent sustainability-led innovation (e.g., a registered plastic-free, wood-pulp-based disinfectant wipe) and broad institutional penetration, making them a key bellwether for sustainable product adoption rates.

Kimberly-Clark, 3M, Cardinal Health: large, diversified players that can leverage distribution scale and private-label partnerships to protect volumes across healthcare and industrial channels.

Diamond Wipes & Zhejiang Aijian: contract/OEM capability that remains strategically important for private-label growth and rapid capacity scaling — a valuable option for brands balancing speed and capital.

Recent events reflect these dynamics: sustainability-focused product launches, portfolio expansion into natural-alcohol formats, and precautionary recalls tied to manufacturing compliance. Each event highlights how product innovation, supply-chain control, and regulatory rigor translate directly into commercial outcomes.

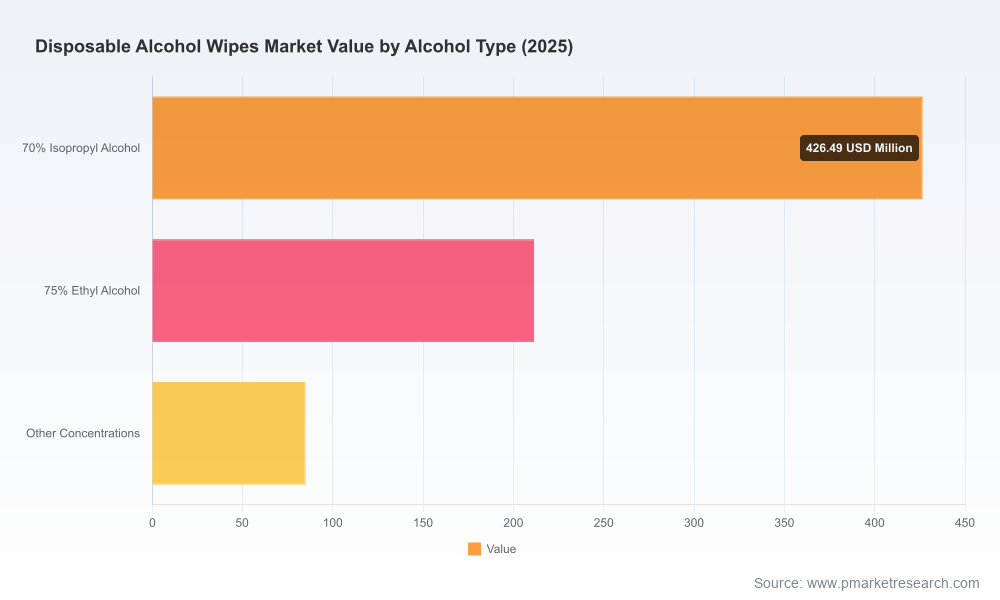

The full report contains granular segmentation by region, alcohol concentration, substrate type, and application channel, alongside channel economics (branded vs. private label, institutional tender dynamics, and online/retail pricing elasticity). In the spirit of this preview we outline directional takeaways without reproducing the underlying splits: growth is heterogeneous across channels, sustainable and low-plastic formats are commanding premium placement in institutional procurement, and private-label penetration varies by geography and buyer sophistication. The report supplies the detailed splits, supplier-by-segment maps, and channel-margin ladders required for 2026 strategic planning.

Hedging and supplier diversification: Scenario models in our report show that securing multi-sourced IPA and alternative solvent syllabi, combined with contractual floor/ceiling pricing, materially reduces margin volatility.

Vertical partnerships: Building relationships with substrate manufacturers or pursuing tolling agreements can mitigate exposure to polymer cycles and lead time shocks.

Sustainability and circularity: Investment cases around plastic-free substrates and compostable formats are improving, but require validated end-of-life claims and pilot institutional deployments to avoid greenwash risk.

Re-segment your portfolio: Define distinct playbooks for regulated medical prep pads, hospital-grade disinfectants, and higher-volume personal-care wipes; each requires different regulatory, quality, and go-to-market investments.

Prioritize procurement resilience: Lock multi-year contracts for critical solvents, maintain safety-stock policies, and adopt real-time commodity monitoring to act quickly on price inflection points.

Invest in regulatory capital: Fast-track registrations and third-party efficacy validation where buyers demand hospital-grade claims; conversely, curate consumer-facing claims to avoid unnecessary regulatory friction.

Evaluate M&A and contract manufacturing options: Moderate market concentration and mid-market fragmentation create acquisitive and partnership opportunities to capture scale advantages while preserving nimble product innovation.

Commercialize sustainability credibly: Use product performance studies and certified end-of-life pathways as a differentiator in institutional procurements and large retail accounts.

Validated market sizing and a 2026–2032 forecast model with scenario sensitivity (commodity shocks, regulatory tightening, sustainability adoption curves).

Segment-level playbooks (go-to-market strategies, pricing ladders, and margin models) for manufacturers, private-label partners, and institutional distributors.

Supplier and competitor heatmaps, including capability matrices for formulation, registered claims, and manufacturing compliance.

Procurement and inventory playbooks with recommended KPIs, supplier scorecards, and contract templates to mitigate IPA and substrate volatility.

Regulatory checklist and pre-submission roadmaps for EPA/FDA registration strategies across major jurisdictions.

Actionable M&A and partnership screening criteria, with integrated financial sensitivities tied to raw-material scenarios.

Beyond the report, PW Consulting provides tailored advisory services: scenario-based strategic planning workshops, supplier negotiation support, regulatory submission coaching, and post-deal integration planning for M&A. Our clients use these services to convert market insight into executable 12–24 month plans that protect margin, accelerate product qualification, and secure strategic channels.

2026 will be a year of choices for players in the disposable alcohol wipes market. The macro numbers point to renewed growth and attractive mid-term upside, but the path to profitable scale is conditioned on handling raw-material swings, meeting tightening regulatory expectations, and credibly addressing sustainability. The firms that succeed will combine disciplined procurement, targeted product segmentation, and regulatory readiness with the commercial muscle to capture institutional and premium retail opportunities.

For executives preparing 2026 budgets and go-to-market plans, PW Consulting’s full Disposable Alcohol Wipes Market report supplies the granular data, scenario models, and implementation playbooks necessary to de-risk decisions and capitalize on recovering demand. Access the complete study for detailed segment tables, regional models, and supplier-level intelligence not published in this preview.

For detailed analysis of this topic, please visit the official page:Disposable Alcohol Wipes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com