PW Consulting: Optical Circuit Switches Market to Expand at 20.5% CAGR, Reaching USD 2.77 Billion by 2032

Technology |

2026-07-02 10:56:32

PW Consulting’s latest Black Beer Market study delivers an actionable intelligence package designed to shape decisions across strategy, sourcing, brand portfolio, and M&A in 2026. This preview summarizes the report’s strategic takeaways and the high-level market trajectory — enough to inform boardroom debate and immediate tactical moves while reserving detailed segment-level tables and scenarios for the full report.

Black Beer Market

The global black beer market — encompassing stouts, porters, dark lagers and related dark ales — is on a clear growth path from our 2025 base year. After recovering from mid-decade volatility, total market value rose from a roughly USD 10.2 billion baseline in 2020 to USD 12.5 billion in 2025 and is forecast to reach approximately USD 17.0 billion by 2032. Our modeled compound annual growth rate through the forecast window is 4.52% (2026–2032), reflecting a mix of premiumization, craft innovation and uneven regional demand recovery.

Black Beer Market

Investment prioritization: The report identifies where incremental returns are most likely across premium SKUs, limited-release barrel-aged programs, and on-trade experiences — enabling capital allocation between brand marketing, contract brewing capacity, and barrel-aging infrastructure.

Black Beer Market

Sourcing and price risk: We provide procurement scenarios tied to raw-material dynamics (barley pricing trends and malting availability) so procurement teams can quantify hedging strategies, supplier concentration risks, and cost pass-through levers.

Channel playbooks: For commercial leaders, we outline near-term tactical mixes across on-trade activations and off-trade distribution that maximize margin capture while preserving brand equity.

M&A and partnership screening: The study includes a prioritization framework for tuck-ins, craft-capacity buys, and co-packing partnerships, aligned with ROIC thresholds relevant to 2026 financing conditions.

This is not a descriptive market brief. The full report contains:

A verified historical dataset (2020–2025) and a transparent forecasting model (2026–2032) delivered in an editable Excel workbook so teams can run sensitivity tests against price, volume and channel mixes.

Scenario playbooks (three probability-weighted growth paths) with triggers and lead times for capacity, marketing spend, and SKU rationalization.

Go-to-market templates for major trade channels, including pricing ladders, promotional cadence, and account-level margin modeling for both on-trade and off-trade.

Raw material and input-cost heatmaps that tie barley and adjunct cost scenarios to SKU-level profitability and suggested hedging approaches.

Competitive dashboard with strategic positioning, product pipelines, and a short list of potential acquisition targets filtered by capacity, brand equity and distribution reach.

Regulatory and trade risk matrix — export/import constraints, excise dynamics, and trade-policy sensitivities mapped to likely demand impacts.

The market displays moderate concentration: the top three and top five players together command a material share of global value, underscoring a landscape where global brand incumbents coexist with highly innovative craft operators. This structure matters because it creates distinct strategic pathways for market participants: scale-based defensive plays (supply chain optimization, route-to-market control) versus differentiation plays (limited editions, barrel programs, experiential partnerships).

Key global and craft players remain central to shaping category dynamics. Our report provides a tactical read of six core competitors and what their moves imply for market entrants and incumbents:

Diageo (Guinness) — The Guinness franchise remains the global touchstone for stout identity. Its scale and brand equity make it the default partner for route-to-market co-branding and a benchmark for consumer expectations around texture and roast profile. Strategic implication: medium and large brewers should plan product-tiering that differentiates from heritage global brands while leveraging similar sensory cues where premium margins exist.

Anheuser‑Busch InBev — Through craft subsidiaries and seasonal programs, AB InBev continues to deploy innovation at scale (example: barrel-aged Bourbon County line refreshes). Strategic implication: expect continued aggregation of craft assets and periodic limited releases used to defend premium shelf space and festival mindshare.

Sierra Nevada & Brooklyn Brewery — Craft leaders are capitalizing on ingredient storytelling, barrel-aging expertise and small-batch scarcity. Their agility drives category excitement but also raises the bar for authenticity. Strategic implication: larger players should consider partnership or controlled incubation to access craft credibility without eroding core brand value.

Heineken & Carlsberg — Global brewers are deploying dark variants through portfolio extension and selective craft investments, signaling that dark beer is a strategic category to maintain shelf penetration. Strategic implication: multinational players will prioritize scale efficiencies and global supply chain resilience while experimenting with local flavor adaptations.

Two patterns have become clear from late-2024 through 2025 launches: (1) barrel-aged and limited-run imperial stouts continue to be the primary driver of press and consumer excitement; (2) seasonal launches timed around events (holidays, festivals) amplify premium price realization. Notably, a major Bourbon County family refresh in mid‑2025 and an uptick in craft November seasonal releases validated the value of scarcity-led pricing and cross-channel storytelling.

Raw-material trends are a near-term constraint for some strategies. US barley farm prices and global barley price trends have shown volatility through 2025 and into early 2026. At the same time, US malting-barley usage for beer has trended lower, reflecting broader shifts in brewing volumes and downstream demand. For procurement and operations teams this translates into three imperatives:

Embed price-scenario sensitivity into SKU P&Ls and prioritize flexible contracts for malt and key adjuncts.

Evaluate vertical integration or long-term offtake agreements with malting houses where ROIC supports reduced input cost volatility.

Design small-batch programs that tolerate higher input cost per unit through scarcity pricing and targeted distribution to premium channels.

Portfolio clarity: Rationalize SKUs where low-velocity, low-margin dark variants dilute core brand equity; redeploy savings to limited-release, high-margin barrel-aged lines that support premiumization.

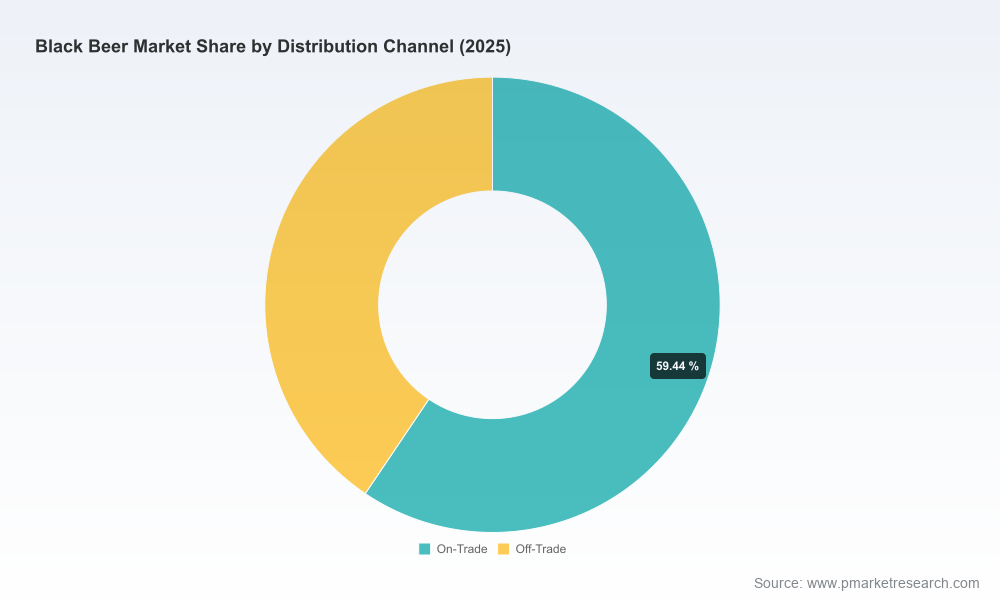

Channel differentiation: Adopt asymmetric strategies for on-trade vs. off-trade — experiential, draft-first launches in on-trade; premium multipacks and collector packaging for off-trade.

Sourcing resilience: Execute a two-year procurement plan that uses blended fixed and variable contracts for malts and barrels; run supplier concentration stress tests as part of annual supply-chain risk audits.

Capability buys: Prioritize micro-acquisitions that buy barrel-aging capacity, unique yeast/fermentation know-how, and validated craft distribution networks rather than broad geographic expansion alone.

Analytics-first commercialization: Use point-of-sale micro-splits and limited pre-launch A/B tests to refine price elasticity and promotional depth before full rollouts.

Boards, strategy teams, and commercial leaders should use the full PW Consulting Black Beer Market report as both a diagnostic and an execution kit. The editable forecast model and scenario playbooks are designed to be plugged into corporate planning cycles and investor materials. For M&A teams, the companion competitive dashboard narrows an initial deal funnel based on acquisition multiple tolerance and integration cost profiles.

This preview intentionally summarizes the strategic implications while withholding granular regional, channel and type split tables, sample SKU P&Ls, and the full competitor financial deep-dive. Those segment-level matrices and executable templates are preserved in the full report to protect the competitive value of the underlying intelligence and to provide clients with the detailed inputs necessary for transaction-level decisions.

To access the complete dataset, editable models, and the full suite of commercial playbooks and M&A screening tools, download the full Black Beer Market report from PW Consulting’s publications page or contact our industry team for an executive briefing tailored to your strategic needs.

For detailed analysis of this topic, please visit the official page:Black Beer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com