Get Immediate Help With the Sage 50 Canada Support Number

Other |

2026-06-23 11:13:49

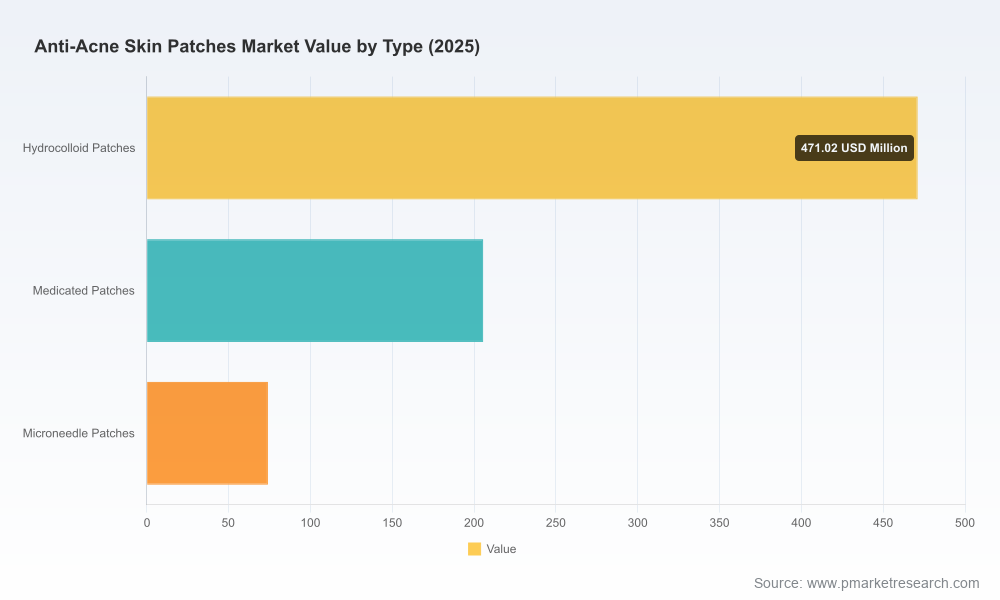

PW Consulting’s latest market study on Anti-Acne Skin Patches frames a pragmatic, decision-ready narrative for executives planning resource allocation and go-to-market moves in 2026. The market has evolved from a niche dermatological adjunct into a resilient consumer-health category: our compiled data show the market expanded materially through the early 2020s and reached an estimated USD 750.6 Million in 2025. Under the assumptions and scenarios modeled in this report, the category is projected to continue growing at a compound annual growth rate (CAGR) of 8.5% over the 2026–2032 forecast window, delivering a pronounced upside for first movers and well-capitalized incumbents.

Anti Acne Skin Patches Market

Timing: 2026 is a structural inflection point — the category is transitioning from product-led novelty to platform-oriented routines (skincare-as-a-service, subscription fulfillment, integrated OTC regimens). Executives must reconcile short-term demand signals with medium-term platform investments.

Anti Acne Skin Patches Market

Capital allocation: The growth profile supports both brand expansion and manufacturing-capacity investments, but the risk-reward varies by strategic posture (brand-owner vs. contract manufacturer vs. private label partner).

Anti Acne Skin Patches Market

Regulatory clarity: Evolving interpretations of device vs. drug classification, and expectations for GMP and establishment registration where active ingredients are present, mean regulatory strategy should be embedded into product roadmaps early.

Historically, the category demonstrated robust expansion—our dataset traces growth from the early 2020s into mid-decade as consumers adopted discreet, evidence-backed spot treatments. From a base of roughly half a billion USD in the early 2020s, the market climbed to an estimated USD 750.6 Million in 2025. Projecting forward with an 8.5% CAGR through 2032, we expect meaningful scale expansion to continue, driven by higher-frequency usage, broader retail availability, and new product formats (including medicated and micro-delivery systems).

For strategy teams, these top-line dynamics translate into three immediate implications: prioritize SKU rationalization to capture repeat-purchase behavior; integrate digital channels into demand forecasting; and plan manufacturing flexibility to support rapid reformulation cycles.

The category today is characterized by a mixed ecosystem: digitally native brands that own consumer mindshare, legacy personal-care conglomerates leveraging distribution scale, and a global network of contract manufacturers and private-label specialists enabling rapid commercialization. Market concentration is moderate: leading players hold a meaningful share of sales, but a long tail of regional and OEM brands sustains innovation and price competition.

Brand leaders and challengers: Companies such as Hero Cosmetics, COSRX, Rael, Starface, ZitSticka, Peace Out Skincare, and established personal-care firms have built distinctive brand propositions — from clinical credibility to playful design and targeted actives. Their playbooks differ on product claims, ingredient stacks, and channel focus.

Institutional players and scale: Multinational manufacturers and consumer-health businesses (e.g., major personal-care portfolios) use their distribution clout and regulatory experience to defend shelf space and enter adjacent categories.

Manufacturing and private label: Contract manufacturers and OEM/ODM specialists (including medical-grade hydrocolloid producers and microneedle-capable firms) create an industry backbone. Their certifications (ISO 13485, GMP, FDA registrations) and capacity footprints materially affect customer lead times and quality controls.

Regulatory posture is a non-trivial driver of product design and go-to-market speed. Non-medicated hydrocolloid patches in many jurisdictions can be positioned under medical device or cosmetic frameworks, while patches containing actives such as salicylic acid may fall under OTC drug monographs and carry additional data, labeling, and establishment requirements. Operationally, manufacturers and brand owners should assume that active-ingredient claims will trigger drug-like expectations: establishment registration, GMP adherence, and enhanced stability and safety documentation.

Because reimbursement pathways are limited—most offerings are OTC consumer products—commercial planning must ground itself in retail and DTC economics rather than in payer negotiations.

Securing resilient supply chains requires balancing three vectors: formulation complexity (hydrocolloid chemistries vs. microneedles vs. medicated matrices), regulatory compliance, and cost-to-serve. Recent vendor activity demonstrates two structural trends: (1) continued investment by contract manufacturers to expand medical-grade hydrocolloid capacity and (2) European and Asian manufacturers scaling private-label capabilities to serve global brand demand.

Operational checklist: Prioritize suppliers with relevant certification (ISO 13485 / ISO 9001 and FDA registration where applicable), validated GMP processes, and traceable raw-material sourcing for medical-grade polymers.

Manufacturing flexibility: Design launch programs with tiered supplier backups—an incumbent brand should expect to qualify at least two geographically diversified partners during product development.

Innovation is not only about novel actives. It also includes packaging that preserves adhesive performance, micro-delivery formats for cystic lesions, and consumer-facing ergonomics that increase wear compliance. Our advisory suggests a two-track product roadmap for 2026:

Core repeat-purchase SKUs: Clinically credible hydrocolloid patches with optimized adhesion and clear instructions to drive high-frequency usage and low returns.

Specialty and premium SKUs: Microneedle or medicated variants positioned at a premium for users with higher unmet clinical need; these require more rigorous regulatory and manufacturing pathways but offer higher margin potential.

Winning in 2026 means aligning product, channel, and message to three buyer archetypes: routine self-care users, performance-seeking consumers, and clinical referral channels (for higher-acuity products). Tactical recommendations include:

Channel mix optimization: Invest in e-commerce capabilities to capture repeat buyers while preserving selective brick-and-mortar presence for new-customer discovery.

Subscription and replenishment mechanics: Design bundles and auto-replenish models with clear savings to improve LTV and reduce customer acquisition payback periods.

Clinical and influencer evidence: Combine lightweight, reproducible clinical endpoints with authentic social proof to accelerate trial and conversion.

Expect continued product line extensions from consumer-facing brands, targeted R&D by microneedle specialists aiming at more clinically impactful delivery, and selective consolidation among contract manufacturers to secure scale and certification depth. Private-label and white-label supply will remain a dynamic battlefield as retailers seek margin capture and brand partners pursue rapid scale.

Our full report is designed as an operational toolkit for leaders making 2026 decisions. It includes:

Top-down and bottom-up market forecasts with scenario modeling for multiple adoption curves and pricing environments.

A validated supplier matrix and capability map for OEM/ODM partners, focusing on certifications, capacity, and formulation specialties.

Regulatory pathway decision trees for conventional hydrocolloid, medicated patches, and micro-delivery systems, plus a compliance checklist for market entry.

Commercial playbooks covering channel economics, subscription models, and retail partnerships—plus example ROI models to stress-test investment cases.

Competitive profiles that synthesize brand positioning, innovation levers, and go-to-market tactics of market participants—from digitally native challengers to legacy consumer-health firms.

To maintain investigative integrity and to serve executive needs, the report presents granular segmentation and supplier-level data behind a secure access point. Our “trailer” approach here communicates strategic direction and tactical priorities while reserving the segmented numerical models and supplier scoring for report subscribers and licensed clients.

Manufacturing investment continues: Major contract manufacturers have signaled capacity expansion and product-line upgrades to meet growing demand for medical-grade hydrocolloid products.

Product catalog expansions: Select regional manufacturers reported new-generation hydrocolloid products targeted at brand customers and private-label partnerships.

Regulatory environment: Firms should track device vs. drug classification updates and prepare for the operational implications of active-ingredient claims (establishment registration, GMP, and labeling).

Clarify your strategic role: Decide whether to play as a premium brand, a scale retailer-private-label supplier, or a specialized contract manufacturer. Each path requires distinct investment profiles and risk tolerances.

Embed regulatory and supplier diligence into early R&D: For any SKU with actives or novel delivery systems, allocate program time and budget for drug-like documentation and third-party audits.

Prioritize repeat-purchase economics: Optimize packaging, dosing per unit, and subscription mechanics to maximize customer lifetime value and compress CAC payback.

PW Consulting’s Anti-Acne Skin Patches Market report is intentionally hands-on: it gives strategy teams the models, checklists, and vendor intelligence required to convert market growth into profitable, defensible business models. For executives seeking the full datasets, supplier scores, and segmented forecast tables that underpin our conclusions, please access the complete report on our website or contact your PW Consulting account representative for a tailored briefing and license options.

For detailed analysis of this topic, please visit the official page:Anti Acne Skin Patches Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com