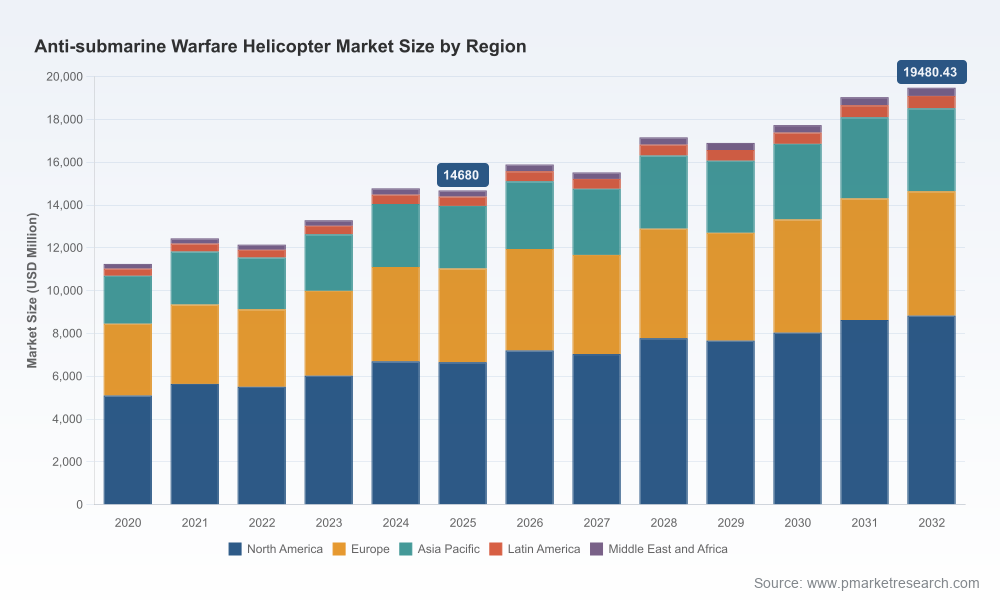

PW Consulting: Anti Submarine Warfare Helicopter Market Valued at USD 14,680 Million in 2025 as Nations Ramp Up Naval Air Capabilities

Other |

2026-07-02 12:36:53

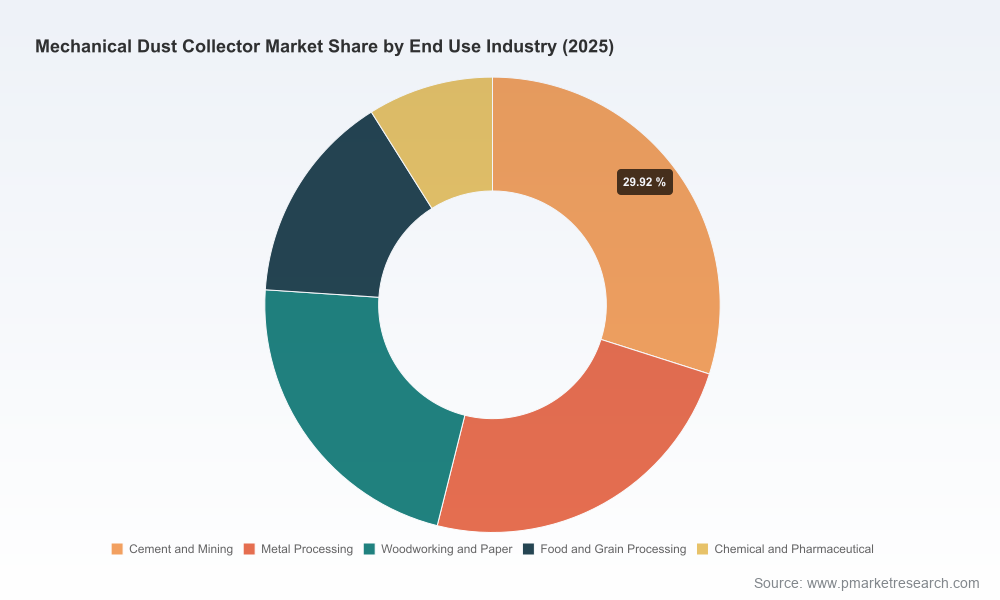

The mechanical dust collector market has returned to a steady growth trajectory following pandemic-related dislocations. Our latest market model shows the industry expanding from an estimated USD 648.2 Million in 2025 to nearly USD 900.0 Million by 2032, corresponding to a compound annual growth rate (CAGR) of approximately 4.8% over the 2026–2032 forecast window. PW Consulting’s Mechanical Dust Collector Market report (base year 2025; historical coverage 2020–2025; forecast 2026–2032) synthesizes this trajectory into practical guidance for manufacturers, industrial end users, investors, and policy-facing supply chain managers preparing for strategic moves in 2026.

Mechanical Dust Collector Market

Regulatory acceleration: Tightening emission and combustible dust standards are compressing technology timelines for customers in metal processing, cement, food & grain, and other dust-intensive industries. Firms that pre-position compliant, certifiable product lines will avoid costly retrofit cycles and capture outsized share of upgrade spend.

Mechanical Dust Collector Market

Capital allocation clarity: A mid-single-digit market CAGR belies pockets of above‑average growth driven by mandated upgrades, retrofit cycles, and aftermarket service demand. Companies that prioritize CAPEX for high‑efficiency filters and explosion-proof configurations will realize faster payback through service and spare-part annuities.

Mechanical Dust Collector Market

Fragmented competitive landscape: Market concentration remains low, with leading triads and quintets controlling a minority share of global revenue. This fragmentation creates M&A and bolt-on acquisition opportunities for scale players and strategic entrants seeking distribution, product breadth, or geographies.

The report is designed as a boardroom-to-shop-floor playbook. It translates market sizing and trend analysis into executable initiatives rather than only descriptive commentary. Key deliverables include:

Decision-ready financial models — sensitivity-tested revenue and margin scenarios across three regulatory and commodity-price pathways for 2026–2032.

M&A target shortlist and valuation frameworks — tactical profiles of acquisition candidates filtered by technology fit, aftermarket potential, and integration risk.

Go-to-market playbooks — segmented commercial strategies for OEMs, distributors, and service providers that prioritize retrofit projects and long-term service contracts.

Operational readiness checklists — manufacturing and supply-chain contingency plans addressing raw‑material volatility and labor-cost pressure.

Compliance and certification roadmap — stepwise product-design and testing milestones aligned to shifting national and regional emissions standards, with estimated timelines for 2026 procurement cycles.

Aftermarket monetization blueprints — pricing, SLA structures, and remote-monitoring packages that convert one-time equipment sales into recurring revenue streams.

Three dynamics will disproportionately shape capital deployment and competitive positioning in 2026:

Regulation-driven upgrades: Recent rulemaking has heightened minimum efficiency and safety thresholds for dust collectors, with some jurisdictions specifying near-total particulate capture for certain metal processing operations. This creates a time-limited window for vendors that can demonstrate certified compliance to capture mandated retrofit spending.

Input-cost and supply-chain pressure: Fabrication inputs such as carbon steel experienced meaningful price volatility in late 2025, increasing fabricator cost bases and shortening the runway for price stability. Strategic firms will need supplier-lock agreements, flexible bill-of-material designs, and pricing guardrails to maintain margin under cost stress.

Labor and service economics: Rising industrial maintenance wage rates are shifting customer preference toward lower-touch systems and predictive maintenance contracts. Vendors that combine higher-efficiency media with remote diagnostics will command premium service margins while reducing total cost of ownership for buyers.

The sector is characterized by strong specialist players alongside regional fabricators. Our report profiles leading companies and decodes the strategic implications of their recent moves:

Donaldson Company, Inc. — continues to invest in performance media and modular platforms aimed at metal fabrication and heavy industrial customers. Their trade‑show demonstrations in 2025 signaled a push toward higher-throughput, lower-maintenance units engineered for automated metalworking environments.

Camfil APC — product launches in late 2025 emphasized cartridge and fine-dust technologies for cleanroom-adjacent end uses, indicating a focused play on high-margin specialty segments such as pharma and food processing.

Nederman — recent exhibits prioritized energy efficiency and system integration, aligning with buyers seeking lower lifecycle energy footprints. Expect Nederman to pursue partnerships that extend their reach into factory automation projects.

RoboVent, Wheelabrator (Archetype), Ceco Environmental, Schust Engineering, Aget Manufacturing — each firm brings distinctive strengths, from high-efficiency particulate removal and aerospace-grade solutions to heavy-duty, high-temperature filter systems and agri/woodworking specialization. Collectively, they create a landscape where technology differentiation, service models, and channel relationships determine local leadership.

Product & R&D — Prioritize filter media and sealing technology that meet the next wave of particulate-efficiency standards while reducing pressure-drop to lower energy cost. Modular designs that enable in-field upgrades will shorten procurement cycles and increase attach rates for service contracts.

Commercial & Go-to-Market — Reframe sales incentives toward retrofit and service contracts rather than capital equipment discounts. Target prescriptive procurement triggers (regulatory compliance windows, plant modernization budgets) and equip field teams with quantified TCO calculators.

Operations & Supply Chain — Lock-in steel and filter media supply through hedges and multi-sourcing. Design BOMs to tolerate material swaps without re-certification where possible to avoid production stoppages amid commodity shocks.

M&A & Partnerships — Use acquisition to secure aftermarket distribution, accelerate geographic reach, or acquire niche filtration IP. Smaller, specialized fabricators make valuable targets for rapid capability buildouts at modest valuation multiples in a fragmented market.

Digital & Services — Embed sensors and remote diagnostics to reduce on-site service time and convert maintenance into subscription revenue. Field-service digitization is a high-leverage route to improve customer retention while offsetting rising labor costs.

Regulatory timing risk — If rule implementation lags, retrofit spending may defer; mitigate with flexible product roadmaps that allow staggered investment and optional certification packages.

Raw‑material price shocks — Use collars or medium-term purchase agreements for key inputs and create value-engineered SKUs that maintain compliance at lower cost points.

Integration risk for acquirers — Prioritize cultural and systems compatibility in M&A selection; plan for 100‑day integration sprints to capture synergies without disrupting aftermarket commitments.

For executive teams preparing 2026 budgets and strategic priorities, the report functions as a toolbox: an evidence-based market sizing and scenario engine, a prioritized list of near-term commercial initiatives, and a tactical M&A and product roadmap. Use it to:

Set FY-2026 R&D and service revenue targets consistent with modeled demand curves.

Stress-test procurement and pricing assumptions against commodity and regulatory scenarios.

Build a 12–24 month M&A/partnership pipeline focused on aftermarket scale and technical differentiation.

PW Consulting’s Mechanical Dust Collector Market report blends proprietary modelling, primary interviews, and on-the-ground supplier intelligence to deliver decision-ready insight. Because we intentionally reserve granular segmentation tables and transaction-level datasets for the full report, we invite strategic leaders to review the complete findings and downloadable spreadsheets on our website to unlock market-by-market, product-by-product analytics and valuation appendices needed for board-level approvals.

Contact PW Consulting to schedule a briefing with our lead analysts and receive a tailored extract that aligns the research to your 2026 planning horizon.

For detailed analysis of this topic, please visit the official page:Mechanical Dust Collector Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com