Pancreatic Cancer Diagnostics Market Dynamics: Key Drivers and Restraints

Other |

2026-06-01 09:20:10

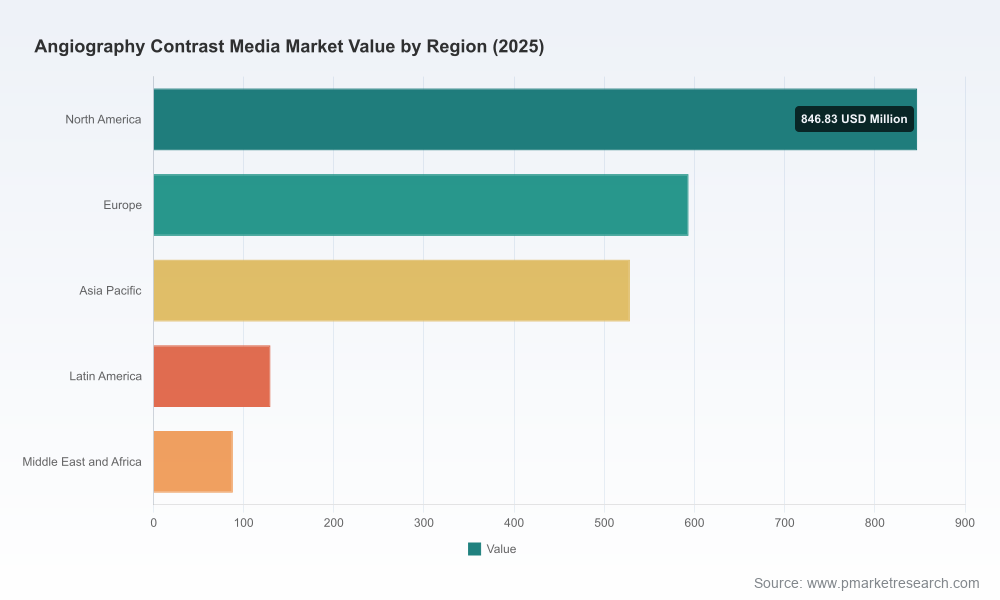

PW Consulting’s latest Angiography Contrast Media Market briefing (base year 2025; forecast 2026–2032) is designed to be a decision-grade intelligence asset for executives, corporate development teams, and investors preparing strategic moves in 2026. Our top-line market model shows a multi-year recovery and expansion following a dynamic 2020–2025 period, with the global market progressing from a mid‑single‑billion base in 2020 to an estimated USD 2,186.08 Million in 2025 and a projected trajectory to roughly USD 3,248.18 Million by 2032. The underlying compound annual growth rate for the forecast window is 5.82% — a growth profile that supports both defend-and-expand plays by incumbents and targeted entry strategies by challengers.

Angiography Contrast Media Market

Actionable market sizing you can trust: independent, reconciled topline figures and a transparent forecasting engine that synthesizes clinical adoption curves, procedure volumes, pricing dynamics, and regulatory/reimbursement scenarios to produce near-term (2026–2028) and medium-term (2029–2032) revenue pathways.

Angiography Contrast Media Market

Scenario-driven playbooks: three practical growth scenarios (conservative, base, upside) that translate macro assumptions into deal-oriented implications — e.g., pricing resilience under supply shocks, volume upside from CT angiography protocol shifts, and downside risks from tighter safety guidance on specific agent classes.

Angiography Contrast Media Market

Commercial due-diligence toolkit: ready-to-use frameworks and KPI dashboards for rapid validation of target assets, including supplier scorecards, margin sensitivity tests, and integration risk matrices tailored to contrast media portfolios.

Regulatory and reimbursement foresight: line-of-sight on how FDA guidance and 2026 CPT/CMS coding updates can change route-to-market economics for angiography procedures, with concrete recommendations for coding strategy, clinical evidence generation, and payer engagement.

The market’s 5.82% forecast growth masks a differentiated internal structure: demand elasticity is strongly tied to procedural mix (CT angiography vs. invasive angiography), technology-driven contrast delivery innovations, and local reimbursement environments. Two regulatory and reimbursement developments in late 2025–early 2026 are particularly material:

Device-compatibility clearances: manufacturers securing formal compatibility between contrast agents and high-performance injection systems (including recent FDA 510(k) clearances for injection platforms and contrast-management systems) are unlocking faster adoption of optimized angiography protocols in hospitals and imaging centers. This reduces operational friction and can be a basis for value-based contracting between contrast suppliers and large health systems.

Safety and coding guidance: continued FDA/ACC communications on renal safety for certain agent classes, paired with CMS/CPT coding updates effective 2026 for diagnostic angiography, create both compliance requirements and commercial opportunities. Providers that can operationalize safety screening and documentation will capture more favorable reimbursement and reduce complications-related costs.

Supply-side factors — manufacturing scale for iodinated agents, regional API sourcing, and short-cycle injectors — remain critical. Our analysis identifies supplier concentration as a structural feature of the market: the three largest firms account for a high share of the market (CR3 ~68.5%), while the top five firms capture roughly 82.1% (CR5 ~82.1%). High concentration amplifies the strategic value of partnerships, long-term supply agreements, and selective capacity investments in 2026.

We assessed capabilities, recent moves, and competitive positioning for the primary market participants to surface near-term vectors for share gains and defensive responses. Highlights include:

GE HealthCare — incumbent portfolio strength and channel reach. GE’s comprehensive iodinated product set, presence in CT ecosystems, and customer relationships make the company a natural anchor for bundled imaging solutions. Strategic priority for competitors: differentiate on injector compatibility, evidence of safety in special populations, or service economics to dislodge entrenched purchasing patterns.

Bayer AG — regulatory momentum and systems integration. Recent regulatory clearances linking contrast agents to established injection systems underscore Bayer’s dual emphasis on product compatibility and systems thinking. Competitors should expect Bayer to pursue integrated offerings and partnerships with device OEMs to defend premium positioning.

Bracco Imaging and Guerbet — European strongholds with targeted innovation. Both firms combine established iodinated portfolios with an emphasis on interventional and diagnostic imaging channels. Their regional depth is a go-to-market advantage but also a platform for selective global expansion via licensing or co-marketing.

Lantheus Medical Imaging — niche and cross-modal positioning. Lantheus remains active across vascular and cardiac imaging niches; strategic moves will likely center on clinical differentiation and value-based contracting with cardiology centers.

ulrich GmbH & Co. KG — injector and contrast-management leverage. As injectors and management systems gain regulatory OK for angiography-grade pressures, firms that can couple delivery hardware and consumables create lock-in effects. Expect increased co-marketing and certification programs tied to device suppliers.

Regional manufacturers (Taejoon, J.B. Chemicals, Sanochemia) — price and supply-availability plays. These players are important in tender markets and private hospital segments; their strategic options include stepping up quality certifications, local partnerships, and targeted capacity expansion to capture displacement opportunities during supply shocks.

Executive summary with investment thesis and decision heatmap for 2026–2028.

Market model (Excel) covering 2020–2025 historicals and 2026–2032 forecasts, with transparent assumptions and scenario toggles for pricing, procedure growth, and substitution trends.

Regulatory & reimbursement playbook: actionable steps to align clinical positioning with FDA/ACR safety guidance and CMS/CPT 2026 coding changes.

Competitive profiles and tactics: go-to-market strategies, R&D posture, device compatibility, and partnership matrices for listed companies.

M&A and partnership shortlist: target archetypes, indicative valuation ranges, and integration risk checklists for acquirers and PE investors.

Commercial templates: supplier RFP language, long-term supply contract clauses, price-protection models, and tender-response playbooks.

Primary research appendix: interview summaries with radiology directors, procurement leads, and OEM engineering teams; methodology and sample frame documentation.

Note: to preserve the strategic value of the research and in keeping with our pre-release policy, granular subsegment tables (regional, agent-type, and application-level percentage splits) are omitted here. These detailed segment-level drivers and the full numeric dataset are included in the licensed report package available on the PW Consulting site.

Week 1–3: Quick triage — use our executive heatmap to prioritize 2–3 commercial initiatives (e.g., device compatibility certifications, targeted hospital tenders, or premium evidence generation) that can be mobilized in 90 days.

Month 1–2: Evidence & contracting — assemble a cross-functional team (clinical, regulatory, procurement, legal) to fast-track any necessary labeling or compatibility submissions and to pilot updated supply contracts incorporating price-protection clauses we provide.

Month 2–3: Market activation — deploy targeted field engagements with top accounts identified in the report, launch bundled value propositions with injector OEM partners, and initiate payer dialogues where coding changes enable improved reimbursement capture.

Invest in device and protocol compatibility: secure formal compatibilities and co-marketing arrangements with injector OEMs to reduce procurement friction and enable premium positioning.

Prioritize safety evidence for vulnerable populations: publish and operationalize renal-safety protocols and premedication algorithms to preserve procedure volumes and reduce payer pushback.

Pursue selective M&A to fill capability gaps: given market concentration, smaller portfolios with regional manufacturing can yield near-term margin accretion and tender access if integrated quickly.

Negotiate long-term supply arrangements now: with concentrated suppliers and potential API bottlenecks, secure multi-year agreements or dual-sourcing strategies to stabilize volumes and pricing.

Align commercial teams with coding changes: update clinical documentation workflows to capture new CPT pathways and avoid revenue leakage from missed documentation opportunities.

PW Consulting’s full Angiography Contrast Media Market Report includes the complete numeric model, granular segmentation, and proprietary supplier scoring necessary to act decisively in 2026. For licensing, bespoke secondary research, or a rapid strategy workshop that translates the report’s findings into an executable 90-day plan for your organization, visit our report page or contact PW Consulting’s industry leads. The full report is the only place where we publish the detailed subsegment tables and the downloadable Excel model referenced above.

For detailed analysis of this topic, please visit the official page:Angiography Contrast Media Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com