Pseudoboehmite Market 2026: Strategic Imperatives for Industrial Leaders — PW Consulting Preview

Executive summary

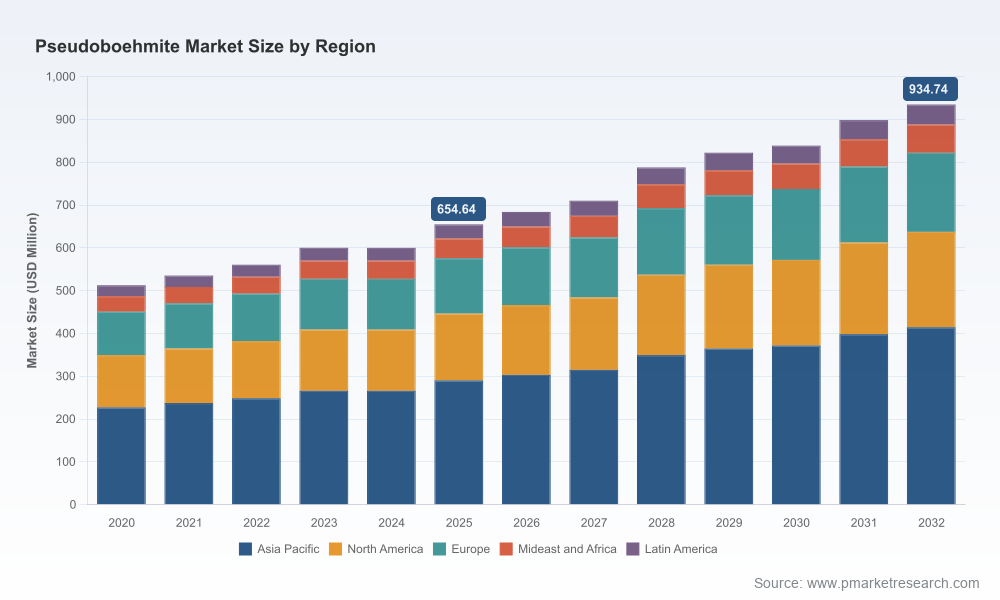

PW Consulting’s forthcoming Pseudoboehmite Market report (base year 2025; forecast period 2026–2032) synthesizes industry-grade intelligence to support board-level decisions, capital allocation, and product strategy in 2026. The global pseudoboehmite market has demonstrated steady expansion through 2020–2025 and is valued at approximately USD 654.6 Million in 2025. At a compound annual growth rate (CAGR) of roughly 5.22% across the forecast window, the market is projected to approach a broadly understood high-single-hundred million USD level by 2032. This preview outlines the report’s practical utility, major dynamics shaping near-term strategy, and the competitive footprints executives must factor into 2026 planning.

Pseudoboehmite Market

Why this matters for 2026 decision cycles

- Timing of capacity investments: With demand growth that is steady but not hyperbolic, spending windows for upstream expansions and advanced grade roll-outs must be calibrated to avoid mid-cycle overcapacity.

- Margin pressure from raw-material volatility: Feedstock pricing and regional input-cost differentials are already influencing conversion economics; procurement and hedging strategies will materially affect project IRRs.

- Regulatory and ESG scrutiny: Recent certification and environmental approvals for major projects signal that buyers and financiers will increasingly require traceability and compliance credentials as part of procurement and offtake agreements.

- Supplier concentration and partner selection: Market concentration metrics indicate that a relatively small group of suppliers captures a meaningful share of demand — creating both counterparty risk and opportunities for strategic sourcing partnerships.

Key market dynamics (what we show and what we intentionally withhold)

The report provides a data-led narrative of supply-demand balance, technology differentiation across product grades, and application trends such as catalysts, adsorbents, refractory formulations, and specialty ceramics. We integrate historical sizing (2020–2025) and detailed scenario models for 2026–2032 driven by industry-specific demand drivers.

Pseudoboehmite Market

To preserve the strategic incentive for stakeholders to consult the full report, this preview omits granular regional and application split figures. The full study, however, includes commensurate segmentation tables and downloadable spreadsheets for commercial due diligence and bid modeling.

Pseudoboehmite Market

Drivers, headwinds and near-term inflection points

- Feedstock and upstream cost trajectory: Aluminum hydroxide pricing has softened in key markets during early 2026, reducing near-term raw-material pressure for many producers. Europe has experienced modest declines, while Northeast Asia has seen a more pronounced pullback following weaker downstream demand. Bauxite and alumina feedstock dynamics remain a sensitive variable for operating cost curves.

- Downstream demand mix: Petrochemical catalyst demand continues to be a principal end-market, while engineered applications (adsorbents, desiccants, ceramics) contribute to diversification. End-market cyclicality in petrochemicals and polymers can cause episodic swings that require flexible commercial responses.

- Regulatory and ESG requirements: Major producers are pursuing environmental approvals and third-party audits tied to sustainability standards. These requirements are increasingly embedded into tender specifications for large refinery and chemical projects.

- Technology and product differentiation: High-purity and engineered porosity grades command strategic value for advanced catalysts and molecular-sieve precursors; producers investing in process control and product homogeneity are better positioned to capture premium pricing.

Competitive landscape — what executives must know

The industry features a blend of multinational incumbents with integrated alumina and catalyst ecosystems, specialty chemical houses, and regional vertically-integrated producers. Market concentration metrics indicate that the top three suppliers capture a significant portion of demand, with the top five widening that share further — a structure that favors incumbent-scale advantages while still leaving room for specialized entrants.

- Sasol Limited — Leveraging alkoxide-hydrolysis capabilities, Sasol’s high-dispersion, high-purity pseudoboehmite portfolio (including established brand lines) is focused on catalyst carriers for heavy refining and petrochemical processing. Their value proposition centers on process reproducibility and integration with downstream catalyst formulation.

- CHALCO / Chalco Shandong Advanced Material — A major industrial-scale producer that has recently progressed a significant production upgrade for hydrocracking-grade pseudoboehmite and undergone related environmental and social assurance processes. Their project steps underline the importance of certification and project-level ESG diligence in current procurement practices.

- Honeywell UOP — Offers a family of engineered alumina powders positioned for adsorbent and catalyst intermediate markets. UOP’s strength lies in application engineering and alignment with large petrochemical and refining OEMs.

- Nabaltec AG, Almatis GmbH, BASF SE — These specialty and materials-focused companies compete on premium grades and technical support for flame retardants, catalysts, and advanced materials. Their service-oriented commercial models and R&D linkages provide higher switching costs for key customers.

- Regional and specialty manufacturers (multiple Chinese producers; select North American and Japanese suppliers) — A cohort of focused producers supplies tailored grades for domestic industries and niche export flows. These firms often compete on cost and speed-to-market for commodity-type grades while some are developing higher-purity variants.

Recent developments that influence 2026 strategy

- Certification and major line approvals: A prominent producer advanced environmental approvals and underwent a third-party sustainability audit tied to a multi-thousand tonne per annum upgrade aimed at hydrocracking applications. Such actions increase the commercial value of production assets when selling into regulated value chains.

- Raw-material price movements: Aluminum hydroxide and upstream bauxite trends in early 2026 have introduced a window of easing input costs in several regions; procurement teams should evaluate short-term contract renewals and optionality to capitalise on this movement.

- Shifts in buyer requirements: Large refinery and catalyst buyers are formalizing supplier ESG checks and requesting lifecycle data — a change that has contractual implications for supply continuity and pricing.

What the PW Consulting report contains (practical, executable components)

- Commercial playbook: Supplier due-diligence checklists, term-sheet templates, and a procurement scorecard for grade selection, lead-time risk, and ESG compliance.

- Financial modeling toolkit: A configurable model with base-case, upside, and downside scenarios (supply shocks, raw-material volatility, cyclical demand shifts) calibrated to the 2026 planning horizon.

- Technology and product matrix: Comparative analysis of production routes (including alkoxide hydrolysis and alternative process technologies), typical property ranges, and application fit maps for catalysts, adsorbents, refractories, and specialty ceramics.

- Competitive dossiers: Executive profiles, capacity footprints, recent project and certification timelines, and strategic assessment of potential M&A targets and JV candidates.

- Risk register and mitigation playbook: Contractual provisions, inventory strategies, and contingency options for rapid feedstock or demand shocks.

Strategic recommendations for 2026

- Adopt staged capacity strategies: Favor modular investments and tolling arrangements when expanding into advanced grades to balance time-to-market with demand uncertainty.

- Lock in feedstock optionality: Use a mix of short-term and indexed contracts for aluminum hydroxide and bauxite-linked inputs to reduce margin exposure while preserving upside participation.

- Prioritize certified suppliers for large-scale projects: Buyers increasingly prefer suppliers with independent environmental and social assessments; this reduces contractual friction and financing risk.

- Invest in application engineering: Players that pair product development with downstream formulation expertise will capture premium pockets in catalyst and adsorbent markets.

- Consider strategic partnerships: JVs with catalyst formulators, or toll-manufacturing arrangements with regional producers, can accelerate market entry without full greenfield capital outlays.

How to use this report in corporate planning

Boards and strategy teams can use the report as a basis for: capital expenditure prioritization; supply-chain resilience programs; tender and procurement frameworks; and M&A screening. The packaged financial models are designed for direct use within investment committees and commercial negotiations. Because the full report contains the granular segmentation and downloadable datasets omitted here, it should be treated as a primary resource for transaction due diligence and multi-year budgeting.

Methodology and data transparency

Our analysis combines proprietary demand modeling, primary interviews with producers, consumers, and technical experts, and triangulation against public filings and recent third-party audits. Market sizing is reported in USD (Million) with a historical series and scenario-based forecasts to 2032. Concentration indicators and supplier profiles are derived from production capacity assessments and validated against multiple field sources.

Conclusion and next steps

For executives shaping 2026 strategies, the pseudoboehmite market presents a measured-growth environment with clear value differentiation between commodity and engineered grades. The interplay of feedstock cost movement, regulatory scrutiny, and supplier concentration makes disciplined procurement and selective investment essential. PW Consulting’s full report delivers the granular segmentation, supplier economics, and downloadable models necessary to convert these insights into executable plans.

To access the complete dataset, regional and application breakdowns, and the financial model templates referenced in this preview, please consult the full Pseudoboehmite Market report on PW Consulting’s publication page.

For detailed analysis of this topic, please visit the official page:Pseudoboehmite Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com