Regional Optical Brightener and Dye Hubs: Meeting Robust North American Demand for Crystalline Intermediates

Other |

2026-06-16 13:22:42

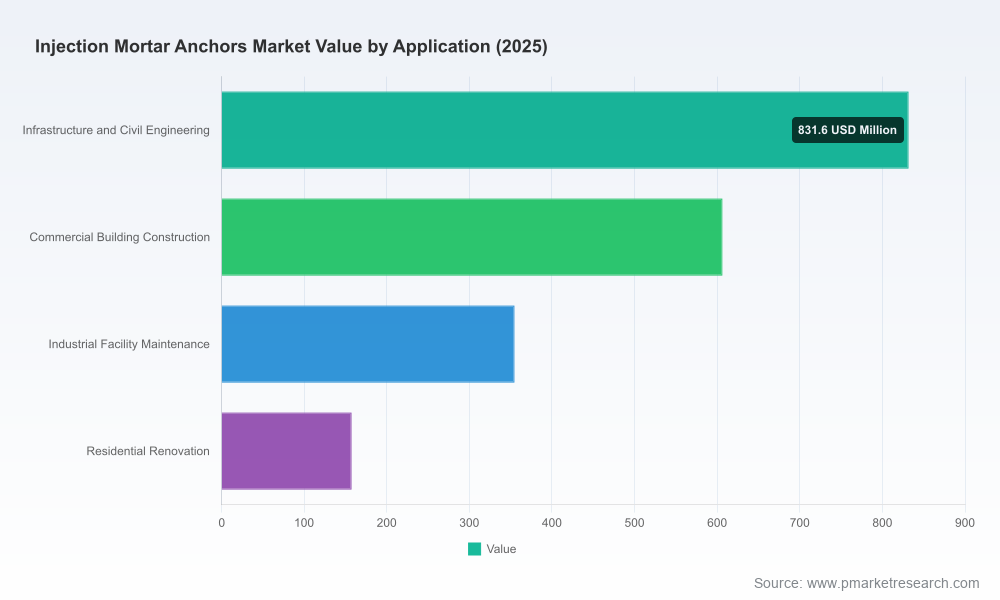

PW Consulting’s latest market study on Injection Mortar Anchors (base year 2025) synthesizes five years of historical performance (2020–2025) and delivers a practical, decision-ready forecast for 2026–2032. The market is entering a phase of steady expansion — our base-year estimate for 2025 stands at USD 1,950.0 Million (revenue, USD Million basis), and the model anticipates an average compound annual growth rate (CAGR) of 5.48% across the 2026–2032 forecast window. This briefing highlights why the 2026 planning cycle should make injectables a strategic priority and how executives can convert the report’s insights into tactical advantage.

Injection Mortar Anchors Market

Momentum and scale: After recovering from near-term volatility, the injection mortar anchor market shows sustained mid-single-digit growth. Our forecast sees the industry moving from a 2025 revenue base of roughly USD 1.95 billion to a materially larger market by the end of the forecast period, reflecting steady demand from retrofit, infrastructure, and high-load structural applications.

Injection Mortar Anchors Market

Structural tailwinds: Drivers include infrastructure renewal programs, accelerated retrofitting of aging assets, seismic and fire-resilience upgrades, and increasing specifications for high-load anchoring in both new builds and post-installed reinforcement projects.

Injection Mortar Anchors Market

Market structure: The sector exhibits moderate concentration. The top three suppliers account for a meaningful share of revenue, and the top five raise that to a clear majority — a dynamic that creates both competitive pressures and strategic opportunities for differentiation.

Procurement and margins: Raw-material volatility (notably epoxy resin) and logistics cost swings have a direct margin impact for manufacturers and distributors. Early-2026 feedstock observations showed regional price dispersion that requires procurement teams to adopt hedging and supplier diversification strategies.

Regulatory and approval risk: In Europe and many export markets, performance approvals (e.g., ETA under relevant EADs) remain the gating factor for structural and seismic use. Option 1 approvals and certifications for drinking water contact or low-emission indoor use (e.g., NSF/ANSI and styrene-free formulations) materially affect product acceptance on critical projects.

Product development inflection: Buyers increasingly demand combinations of fast-cure chemistry, stainless steel compatibility, and simplified installation workflows (dual-action cartridges, pre-measured systems). R&D and product roadmaps must prioritize time-to-cure, broadened substrate approvals, and installers’ ergonomics.

Distribution and service layering: Installation training, specification support, and warranty programs are becoming decisive sources of differentiation, especially for premium-priced systems on infrastructure and seismic projects.

M&A and portfolio plays: Given the concentration dynamics, mid-sized manufacturers and private-label producers remain attractive targets for scale-seeking players looking to accelerate geographic reach or add complementary chemistries.

Validated market model: Historical quantification (2020–2025) and a detailed, scenario-based forecast (2026–2032) with sensitivity testing for raw-material shocks and regulatory shifts.

Go-to-market playbooks: Channel strategies for manufacturers and distributors, pricing levers segmented by project type (infrastructure, commercial, industrial, renovation), and specification-influence tactics for engineering firms and owners.

Regulatory & approvals roadmap: Checklist and timelines for achieving option-grade approvals and key certifications that unlock seismic, fire, and potable-water use cases.

Procurement & cost toolkit: Component-level cost-builders, epoxy-resin exposure analysis, and recommended hedging/contracting structures to mitigate feedstock volatility.

Competitive benchmarking: Vendor scorecards, technology positioning maps, capability matrices, and a distilled view of concentration metrics to inform partnership, alliance, and M&A decisions.

Installation risk & training framework: On-site quality controls, installer training syllabi, and warranty design that reduce performance risk for high-value projects.

The market blends global system leaders, specialty formulators, and regional/private-label manufacturers. The report’s vendor analysis focuses on technology leadership, approval portfolios, channel strength, and recent go-to-market moves — all elements that will determine winners in 2026.

Hilti Corporation — A technology and channel leader with a broad injectable portfolio and a recent push into stainless-steel, dual-action systems. Hilti’s emphasis on installer convenience and integrated system solutions strengthens its position on high-value structural and industrial projects. Its product updates signal continued premium positioning and patent-driven differentiation.

fischerwerke — Strong on approvals and specialty chemistries, with recent enhancements to vinyl ester hybrid systems and positioning for post-installed rebar. Fischer’s ETA-focused approach and engineering support make it a default choice for projects where regulatory acceptance and seismic performance are prioritized.

Sika AG — Leverages a wide adhesive portfolio and approvals for demanding use cases (seismic, fire, potable-water). Sika’s AnchorFix family underscores the company’s strategy of coupling product breadth with global distribution and specification influence.

Simpson Strong-Tie — Focused on hybrid chemistries and fast-curing adhesives targeted at the North American structural and construction connector market. Recent product introductions emphasize performance in extreme environments, catering to retrofit and cold-climate installations.

Private-label & specialty formulators (e.g., 2K Polymer Systems, Good Use, Fosroc, ATC, Klimas, CELO, MKT, Rawlplug, Bossong, DEWALT) — These vendors compete on cost, niche approvals, export reach, and tailored formulations. The presence of agile formulators and national champions keeps pricing competitive and accelerates local adoption where international suppliers face approval or logistics barriers.

Strategic implication: With the top three and top five suppliers controlling notable portions of market revenue, larger players can exert price discipline and set standards, but there remains room for nimble specialists to capture specification-led niches — particularly where approvals, stainless performance, or sustainability credentials matter.

Manufacturers: Prioritize accelerated certification pathways (Option 1-style approvals where applicable), invest in fast-cure and stainless-compatible formulations, and bundle installer training and specification support to justify premium pricing on complex projects.

Distributors: Build technical sales teams that can navigate approvals and project specifications; adopt service-based offers (on-site training, calibration, warranty management) to win long-term contracts with infrastructure owners.

Project owners & engineers: Require clear approval matrices and third-party validation in procurement documents; evaluate total installed cost — including downtime risks linked to cure times — not just unit cost.

Investors & M&A teams: Target bolt-on acquisitions that add approval breadth, stainless chemistry capability, or regional logistics hubs; use the report’s vendor scorecards to fast-track diligence.

Procurement chiefs: Implement multi-sourcing strategies for epoxy feedstocks, explore long-term purchasing agreements, and build pass-through clauses for rapid resin-price moves to stabilize margins.

Think of the study as a toolbox: validated forecasts to justify capital allocation, scenario analyses to stress-test procurement assumptions, and vendor scorecards to prioritize partnerships. The report deliberately surfaces the implications of raw-material price dispersion, standards-driven market access, and the premium attached to fast-cure and stainless systems — while preserving segment-level detail and proprietary vendor shares for subscribers who need exhaustive, transaction-grade data.

This brief is a strategic trailer designed to demonstrate the report’s practical depth and the immediate decisions it supports in 2026. For full segment-by-segment data, granular regional and application-level models, downloadable financials, and complete vendor market-share tables (including segmented revenue breakdowns and price curves), access the full Injection Mortar Anchors Market report on PW Consulting’s website or contact our industry practice for a tailored briefing and licensing options.

In an environment of steady demand growth, regulatory complexity, and raw-material pressures, companies that align product portfolios to approvals, lock in resilient procurement channels, and translate technical superiority into installer-facing value will define market leadership through 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Injection Mortar Anchors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com