Introduction to Limited Edition Labubu Canada Figures

Games |

2026-06-30 13:00:56

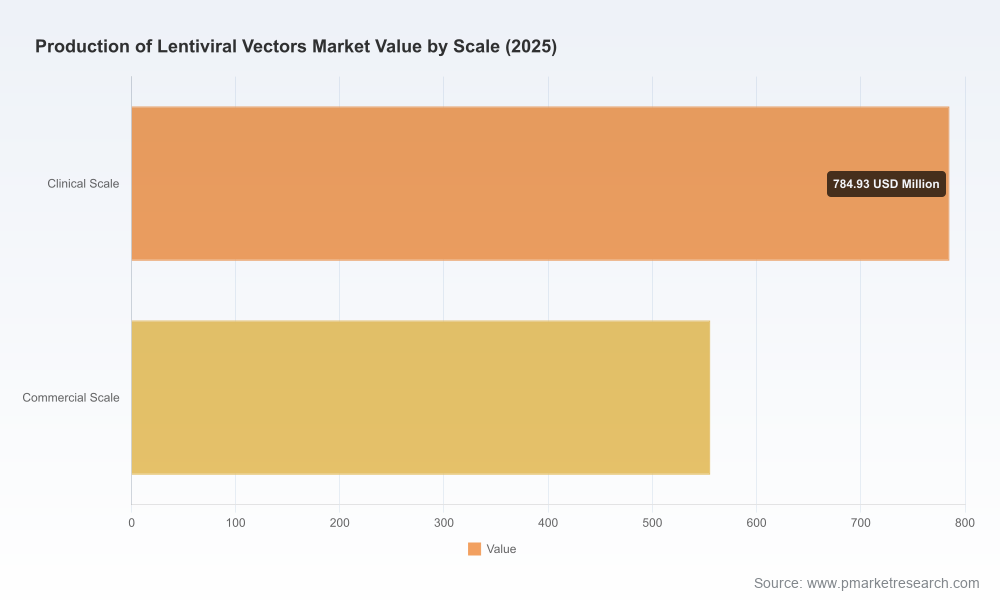

As cell and gene therapies advance from clinical promise toward commercial reality, the industrial backbone that supplies lentiviral vectors (LVVs) is entering a decisive growth phase. PW Consulting’s new Production Of Lentiviral Vectors Market study (base year 2025; forecast 2026–2032) synthesizes market-sizing, competitive intelligence and actionable playbooks that senior executives, strategy teams and investment committees must use to make defensible decisions in 2026. At the macro level, the market is poised to expand from roughly USD 1.34 billion in 2025 to approximately USD 4.40 billion by 2032 — a compound annual growth rate of 18.52% — reflecting rapid therapeutic maturation, scaling of commercial programs, and increased outsourcing to specialized CDMOs.

Production Of Lentiviral Vectors Market

Timing: 2026 is the inflection point for several late-stage CAR‑T and gene therapies moving toward commercial supply. Capacity choices made this year have multi-year consequences for time-to-market and margin.

Production Of Lentiviral Vectors Market

Market structure: The field is moderately concentrated; leading CDMOs hold meaningful share, but a cohort of specialized providers is expanding capacity and capability rapidly. Competitive footprints are changing through facility acquisitions, greenfield builds and strategic collaborations.

Production Of Lentiviral Vectors Market

Regulatory and analytical inflection: Recent regulatory guidance introduces greater flexibility to accelerate early‑phase programs but simultaneously raises the bar for demonstrating fit‑for‑purpose analytical methods at IND initiation and robustness for later phases.

Scale-up imperative: At an ~18.5% CAGR across the forecast window, throughput demand will outpace incremental facility availability unless sponsors and CDMOs synchronize capacity planning and technology transfer timelines.

Concentration impacts: With a sizeable proportion of capacity concentrated among a relatively small set of large CDMOs, sponsors should anticipate supplier negotiation dynamics that favor early engagement and multi-year commitments for priority slots.

Cost and material economics: GMP plasmid inputs represent a substantial portion of raw material spend; transient four‑plasmid systems remain the industry default upstream approach, keeping plasmid sourcing and costs centre-stage in supply chain risk analyses.

The vendor map is evolving into tiers: large integrated CDMOs that offer end‑to‑end development and commercial GMP, specialist CDMOs focused exclusively on LVV capabilities, and nimble regional players that exploit localized demand or regulatory speed-to-market.

Oxford Biomedica: Demonstrates a strategy of commercial-scale positioning and blue-chip partnerships. Their recent multi‑year commercial supply agreement with a major pharma partner and acquisition of an FDA‑approved commercial site in North America underscore a deliberate push to lock in demand and geographic redundancy ahead of commercial launches.

Thermo Fisher (Patheon), Lonza, Catalent, FUJIFILM and WuXi ATU: These integrated CDMOs remain the go-to partners for programs seeking global supply chain continuity, validated tech transfer pathways and large-scale fill/finish capability.

Charles River and other strategic collaborators: Academic collaborations and targeted partnerships remain a low-cost route to build capability and access novel programs, as illustrated by recent alliances to support CAR‑T vector supply for hematologic oncology programs.

Specialists (VIVEbiotech, AGC Biologics, ViroCell, Genezen, ProBio, Expression Manufacturing, Rentschler, Yposkesi, SK pharmteco, Miltenyi): These players are executing focused strategies—expanding cleanroom capacity, launching dedicated LVV platforms, and offering tailored process development. The aggregate effect is more options but also more complexity for sponsor selection.

Commercial supply agreements and site acquisitions signal that a subset of CDMOs expects rapid conversion to commercial demand; sponsors should treat announced capacity as a leading indicator for contracting timelines and potential premium pricing for prioritized slots.

New large-scale facilities and “centres of excellence” coming online mean greater geographic diversification of supply. This reduces single‑point dependency risk but increases the importance of harmonized quality systems and regional regulatory strategies.

Expanded service toolboxes (process development, integrated analytics, regulatory support) are differentiators beyond sheer capacity — increasingly the locus of competition will be speed and predictability of tech transfer and release testing.

Prioritize supplier diversification with staged engagements: secure lead slots with a primary CDMO while qualifying a secondary provider for risk mitigation and negotiation leverage.

Lock in plasmid supply early and explore pooled‑buy or strategic sourcing models to smooth price volatility given plasmids’ outsized share of raw material spend.

Evaluate transient versus stable production strategies: transient four‑plasmid HEK293 workflows remain dominant today, but sponsors must model the long-term cost and timeline benefits of investing in stable producer cell lines for pivotal/commercial programs.

Invest in analytical readiness: ensure assays are fit‑for‑purpose at IND submission and have a roadmap for later‑phase qualification; this reduces regulatory friction and accelerates lot release timelines.

Design commercial launch agreements that balance price, capacity reservation, and performance SLAs — include clear provisions for tech transfer, change control, and IP governance.

Supply chain risk — mitigation: multi-sourcing, strategic inventory buffers for critical consumables (notably plasmids and critical reagents), and supplier financial/operational stress testing.

Regulatory risk — mitigation: early engagement with authorities, rigorous analytical validation plans, and regulatory intelligence monitoring to leverage new flexibilities while meeting quality expectations for later phases.

Operational scale-up risk — mitigation: accelerated process characterization, parallel validation runs, and contingency capacity agreements tied to commercial milestones.

Competitive risk — mitigation: use market intelligence to inform M&A, JV or capacity reservation strategies; consider in‑licensing of platform technology to lock advantage.

Robust market model and scenario analysis that projects demand and capacity requirements across 2026–2032, enabling capital allocation tradeoffs and contingency planning.

Supplier scorecards and benchmarking: operational capabilities, regulatory track record, geographic footprint, time-to-slot, and partnership economics (teaser: our proprietary scoring differentiates high‑certainty partners from opportunistic players).

Commercial contracting playbook: term sheets, sample milestones, and risk allocation templates to preserve optionality during scale-up.

Technology and process decision matrices: decision trees comparing transient vs stable production, single-use vs stainless infrastructure, and critical analytical checkpoints.

Procurement and supply chain tools: raw material costing guides, checklist to evaluate plasmid sourcing strategies, and supplier qualification templates.

Regulatory readiness checklist aligned to recent guidance: IND‑stage fit‑for‑purpose assay expectations and a phased qualification roadmap for pivotal/commercial submissions.

Portfolio prioritization: use the demand scenarios to sequence clinical programs that optimize manufacturing capacity utilization and minimize launch risk.

Outsourcing strategy: define an “80/20” mix of CDMO and internal capability — where core value drivers (e.g., sensitive IP, proprietary cell lines) may justify in‑house investment while commoditized batch supply is outsourced.

M&A and partnership signals: deploy the vendor scorecards and market scenarios to size bolt‑on plays or to inform strategic minority investments in specialized CDMOs.

Regulatory and commercial readiness: map analytics and quality control investments to the IND-to-commercial transition to avoid launch bottlenecks.

Executives entering 2026 face a compressed window to secure capacity, shore up raw material reliability, and align regulatory pathways that will materially affect 2027–2029 launch outcomes. Our analysis shows a high‑growth market with tangible winners among providers who combine scale, analytical rigor and partner-centric commercial models. However, the path from lab to market is not deterministic: choices made this year on supplier selection, manufacturing approach, and analytical readiness will determine who captures durable commercial value.

PW Consulting’s full Production Of Lentiviral Vectors Market report provides the granular intelligence, operational templates and decision frameworks necessary to act with confidence. For the complete dataset, supplier profiles, model access and tailored advisory support, please visit the PW Consulting report page or contact our industry team to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Production Of Lentiviral Vectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com