Hadron Therapy Market Insights 2025–2031 | Global Growth Trends, Segment Analysis & 14.3% CAGR

Health |

2026-03-05 07:58:28

PW Consulting’s latest Ballistic Protection Market briefing synthesizes hard market facts with forward-looking strategic guidance designed to inform leadership decisions through 2026 and beyond. Built on a comprehensive base year of 2025 and an extended forecast window to 2032, this preview translates macro trendlines—including a robust compound annual growth rate (CAGR) for the forecast horizon—into actionable options for defense primes, material suppliers, system integrators and capital allocators. The analysis demonstrates where value pools will expand, where risk is concentrated, and which moves matter now to secure advantage as certification standards, materials science and procurement priorities converge.

Ballistic Protection Market

Market trajectory: The global ballistic protection market shows a clear upward trajectory from the 2025 baseline into the 2026–2032 forecast window, driven by defense modernization, border security investments and elevated first-responder requirements. Our modeled forecast reflects a mid-single-digit CAGR over the projection period, affirming steady growth with episodic acceleration tied to procurement cycles and standards updates.

Ballistic Protection Market

Regulatory inflection: The transition to updated certification standards has accelerated replacement cycles for legacy systems and introduced new product design constraints—most notably with the evolution of NIJ testing protocols and selected NATO standard revisions. These changes are forcing portfolio reviews across manufacturers and pushing OEMs to prioritize certification-ready designs in 2026.

Ballistic Protection Market

Material substitution and cost pressure: Advances in ultra-high molecular weight polyethylene (UHMWPE) and new unidirectional laminates are reshaping trade-offs between weight, protection level and cost. At the same time, aramid feedstock cost volatility has tightened margins for players dependent on traditional fibers, creating opportunities for differentiated materials and vertical integration strategies.

Proprietary market sizing and scenario-based forecasts calibrated to procurement cadences—enabling finance and strategy teams to stress-test revenue and capital plans under multiple demand and price scenarios.

Competitive heatmaps and supplier scorecards that assess technology stack, certification readiness, manufacturing scale and aftermarket capability for the leading suppliers across personnel, vehicle, aircraft and marine protection segments.

Technology-readiness and materials playbooks that compare ceramics/composites, metals, aramid fibers, UHMWPE solutions and specialty ballistic glass across weight, cost, manufacturability and lifecycle replacement cost metrics.

Procurement playbooks: a practical three-horizon action plan for defense and law-enforcement buyers that aligns certification timelines, test programs and inventory refresh programs to budget cycles and threat assessments.

Supply-chain risk maps identifying concentration points for critical feedstocks, tooling and single-source components, plus mitigation options ranging from dual-sourcing to near-shore capacity expansion.

M&A and partnership frameworks that highlight where bolt-on acquisitions, licensing arrangements and JV structures create rapid access to materials, certifications or regional sales channels—complete with valuation heuristics and integration risk checklists.

The market is characterized by a mix of large defense primes and specialized material suppliers. Our concentration analysis indicates a market where the top three players account for a meaningful portion of demand while the top five further increase concentration—suggesting a competitive space with dominant platform suppliers complemented by nimble niche players. This structure favors both scale-driven investment in integrated systems and targeted innovation by smaller firms that can exploit material or form-factor advantages.

Key strategic implications:

Scale matters for vehicle and platform armor programs—larger primes retain advantage through integrated system offerings and long-term defense contracts.

Specialization wins in personnel protection—lightweight materials and modularity create premium niches, especially where new certification requirements impose fit and gender-specific design constraints.

Material suppliers with proprietary fibers or high-performance unidirectional laminates are positioned to capture outsized value if they can secure stable feedstock and scale manufacturing.

Our proprietary company assessments (detailed in the full report) evaluate firms along four dimensions: product breadth & integration capability, material & manufacturing control, certification & regulatory readiness, and commercial footprint. Highlights of publicly observable positioning include:

BAE Systems plc — strong systems integration capability across personnel and platform armor; advantage lies in end-to-end survivability solutions and established defense contracting pipelines.

Point Blank Enterprises — deep expertise in both soft and hard body armor with established channels into law enforcement and certain export markets; responsiveness and customization are core strengths.

DuPont de Nemours — material technology leader with legacy intellectual property in aramid fibers; faces strategic choices on feedstock risk exposure and downstream partnerships.

Avon Protection & Galvion — focus on helmets and personal protective systems; recent product introductions demonstrate the importance of modularity and weight reduction for first responders and infantry units.

Rheinmetall AG — positioned in vehicle armor and survivability modules; benefits from platform-level integration alongside established defense client relationships.

Honeywell, Teijin, Avient (Dyneema) — material innovators supplying Spectra, para-aramid and UHMWPE offerings. Recent launches and material innovations are shifting competitive boundaries toward lighter, higher-performing laminates.

Regional and niche manufacturers — firms such as MKU, NP Aerospace, Morgan Advanced Materials and TenCate inject regional agility and materials specialization into the market, often serving as acquisition targets for scale players.

Product and material innovations: New unidirectional hard ballistic materials and ultra-light helmet launches during 2024–2026 have demonstrated meaningful weight reductions, which materially affect soldier load management and platform payload considerations.

Manufacturing investments: Select firms announced capacity expansions and new tooling investments in early 2026—an indicator that domestic production and assembly scalability are strategic priorities for procurement partners.

Contract flow: Targeted contract awards to regional suppliers for Indo-Pacific operations underscore the importance of geopolitical demand corridors in shaping near-term purchasing.

Certification pressure: The transition to updated testing standards is generating a wave of re-certification and upgrade programs; manufacturers unprepared for the new test protocols risk being excluded from major recompetes.

90 days: Conduct a certification gap analysis. Align product roadmaps and test plans to the updated NIJ/NATO requirements; prioritize women‑specific fit testing and modular add-ons that accelerate re-certification.

365 days: Secure material supply lines. Hedge exposure to aramid feedstock volatility via long-term purchase agreements, diversified suppliers, or investment in UHMWPE/UD laminate partnerships. Implement pilot production runs for new material stacks.

1,000 days: Evaluate M&A and strategic partnerships. Pursue bolt-on targets that provide unique material IP or regional manufacturing footholds. Integrate aftermarket services and analytics to extend revenue per platform through life‑cycle maintenance and upgrades.

Upside drivers: accelerated procurement in strategic theaters, breakthrough cost reductions from new laminates, and scale-based price compression in high-volume vehicle programs.

Principal risks: feedstock cost shocks, certification delays, and manufacturing bottlenecks for advanced fiber layup and ceramic supply chains. Geopolitical shifts can also rapidly reorient demand to specific regions.

Executives will find the report actionable in three ways: it prioritizes investments based on return-on-protection (a lifecycle-adjusted metric we build into every forecast), it provides supplier due-diligence templates tailored to ballistic materials and certification risk, and it delivers a playbook for blending organic R&D with targeted acquisitions to secure material advantages.

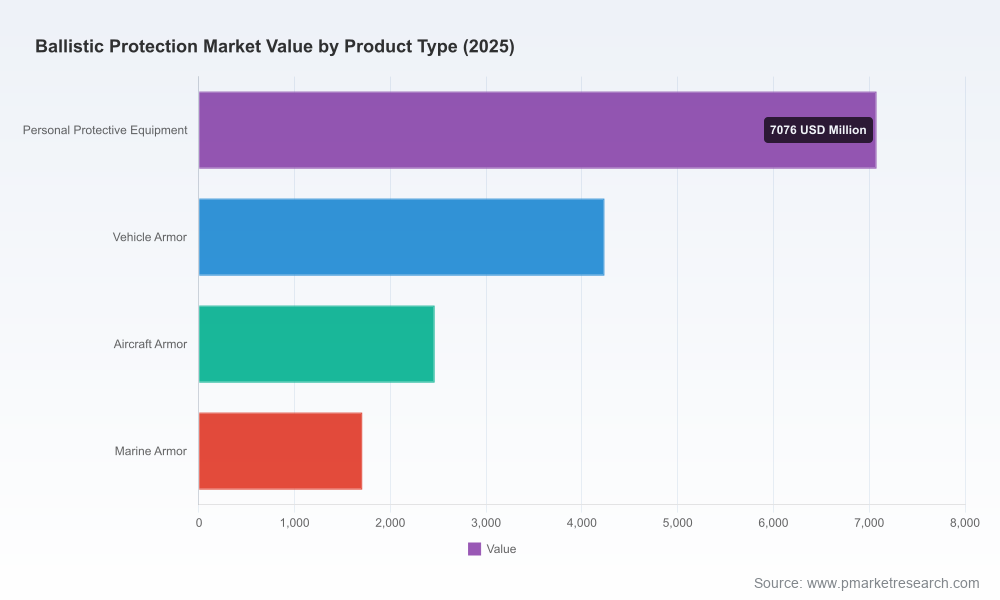

Because the full decision value often resides in segment-level sizing, supplier scorecards and procurement timetables, we have intentionally withheld granular splits from this public preview. The complete report includes detailed regional and application-level analysis, downloadable data tables, manufacturer benchmarking, and model files that allow you to run your own scenarios.

For senior leaders seeking the full intelligence pack—including interactive financial models, supplier scorecards and a prioritized list of M&A targets—reach out to PW Consulting to arrange access to the complete Ballistic Protection Market report and a tailored strategy workshop for 2026.

PW Consulting’s market and technology specialists remain available to review how these trends intersect with your product roadmaps, procurement cycles and capital planning. The window to secure certification-ready designs and resilient supply chains is now—firms that act in 2026 will define the competitive landscape for the next decade.

For detailed analysis of this topic, please visit the official page:Ballistic Protection Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com