PW Consulting: Balanced-armature Magnetic Speakers Market — USD 54.77M (2025), 1.5% CAGR

Other |

2026-07-12 03:42:16

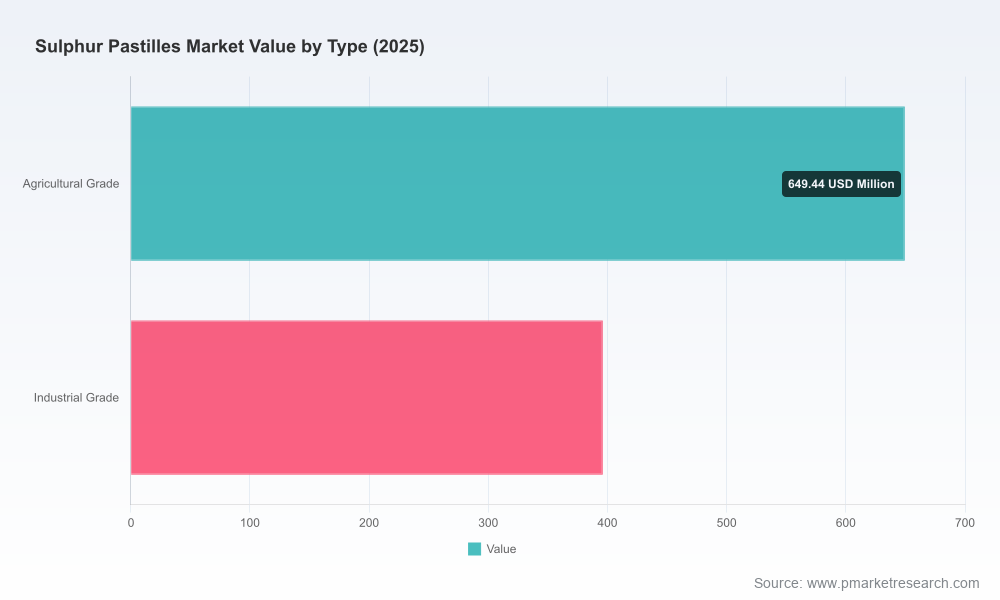

PW Consulting today releases an executive briefing derived from our full Sulphur Pastilles Market report (base year 2025, forecast 2026–2032). The briefing synthesizes the commercial imperatives senior executives and trading, procurement, and corporate development teams must act on in 2026. The global market recorded approximately USD 1,045.5 Million in 2025 and is projected to expand to roughly USD 1,386.96 Million by 2032, reflecting a compound annual growth rate (CAGR) of about 4.12% across the forecast window. This briefing highlights the strategic questions the full report answers, the competitive dynamics shaping supplier choices, and the practical playbooks we provide — while reserving granular regional and application splits for the full dataset available from PW Consulting.

Sulphur Pastilles Market

Pricing & procurement: Raw sulphur price volatility in early 2026 has materially changed cost pass-through and hedging calculus for buyers and manufacturers. Near-term supplier selection and contract structures will determine margin resilience through 2027.

Sulphur Pastilles Market

Supply‑chain resilience: Transportation classification and formed‑sulphur handling rules reduce certain compliance burdens in many jurisdictions, but logistics capacity and storage practices remain critical operational levers.

Sulphur Pastilles Market

Portfolio positioning: Demand from agricultural formulations, industrial processing, and specialty applications requires differentiated product mixes and route‑to‑market strategies (bulk vs. packaged pastilles).

Capital allocation & M&A: Moderate market concentration and stable mid‑single‑digit growth point to four commercial plays — scale expansion, vertical integration, product differentiation, and geographic diversification.

Price environment: Sulphur spot and regional FOB/CIF levels in early 2026 have seen significant movement; industry trackers documented sharp month‑on‑month and year‑on‑year increases in certain markets (source: Trading Economics; Analysts Insights). These swings affect short‑cycle buyers and can create transient arbitrage opportunities for traders and regional processors.

End‑use demand drivers: Fertilizer production, chemical processing and rubber/vulcanization use continue to underpin steady baseline demand, while specialty agricultural formulations and micronutrient blends are sources of incremental premium demand.

Regulatory & logistics context: Formed sulphur (pastilles/prills) typically benefits from relaxed transport classification in non‑bulk packaging under several major jurisdictions (PHMSA DOT interpretation and ADG Code equivalencies). This reduces handling complexity for packaged trade lanes but does not remove labeling, packaging quality and storage risk management responsibilities.

Supply‑side evolution: Manufacturers are deploying multiple forming technologies (drop‑form, rotoform and prilling variants) and optimizing plant footprints to balance feedstock access, labor and freight economics. These technology and location choices materially affect product quality, dust/fines characteristics and downstream processing compatibility.

Integrated US processors with logistics capability: North American producers with multiple domestic processing hubs and downstream sulphur product portfolios are leveraging proximity to feedstock and established distribution networks to defend industrial channels and large commercial fertilizer off‑takers.

Global specialty suppliers: Firms that combine industrial‑grade pastilles with value‑added products (e.g., sulphur bentonite blends, micronutrient‑enhanced pastilles) are capturing premium segments and establishing technical partnerships with formulators and food‑grade processors.

Regional champions in Europe, Middle East and Asia‑Pacific: Longstanding manufacturers using rotoform or drop‑form technologies maintain reliable local supply positions and can scale big‑bag and outdoor stock systems for industrial customers; they are attractive partners for companies seeking rapid market entry without building greenfield capacity.

Smaller, agile suppliers and traders: Niche operators that control certain routes or customer relationships (e.g., agricultural packers, regional distributors) can exploit short‑term arbitrage and expedite specialty orders; they are often targets for bolt‑on acquisitions by larger firms seeking market share or channel access.

Across these archetypes, the competitive narrative is not solely about scale. Product forming technology, dust/fines profile, moisture control, packaging options and warehouse footprint frequently determine the premium or discount a seller can command in differentiated channels. Our full report includes a supplier matrix profiling manufacturing technologies, typical lead times, storage practices (e.g., big bags vs. outdoor stockpiles), and go‑to‑market models for the principal producers in the market.

Demand model to 2032: A probabilistic forecast at global and major regional levels with scenario variants for fertilizer cycles, industrial slowdown/acceleration, and specialty uptake.

Price‑sensitivity and cost‑curve analysis: Inputs and pass‑through models tying sulphur feedstock price movement to finished pastilles margins across processing routes.

Supplier due‑diligence templates: Standardized scorecards to evaluate manufacturing technology, quality controls, logistics capability, and counterparty financial health.

Commercial playbooks: Negotiation checklists for short‑term spot purchases, rolling term contracts and inventory financing structures to protect margins during price shocks.

M&A and partnership screening: Criteria and an initial target list for acquisitions or JV partners by strategic intent (scale, geographic access, technology, specialty product capability).

Risk heatmaps and mitigation planning: Freight bottlenecks, regulatory changes, price volatility scenarios and recommended operational mitigations.

Methodology and data annexes: Sources, model assumptions, historical time series (2020–2025) and the full scenario dataset for client due diligence.

0–90 days (stabilize): Run a price‑shock simulation using our pass‑through template; prioritize counterparty risk checks and secure staggered term volumes with performance clauses. Audit finished‑goods packaging and labeling to ensure continuing transport classification compliance.

90–180 days (optimize): Implement supplier scorecards to rebalance the supply base toward partners offering low‑fines, moisture‑controlled pastilles for your key applications. Negotiate freight and storage commitments aligned with expected seasonal demand swings.

180–360 days (invest): Evaluate targeted bolt‑on acquisitions of regional pastille producers or long‑term tolling arrangements to de‑risk feedstock access and capture margin uplift from product differentiation (micronutrient blends, food‑grade lines).

Price volatility: Rapid moves in raw sulphur pricing observed in early 2026 can compress margins for natively long or short positions; active hedging and contract flexibility are essential (source: Trading Economics; Analysts Insights).

Regulatory shifts: While formed sulphur benefits from non‑bulk transport classifications in many jurisdictions today, regulatory interpretations evolve — track national equivalents and labeling rules closely.

Quality and handling: Fines, moisture and particle shape materially affect downstream performance in fertilizer blending and industrial processes; specifications and on‑site QA can be the difference between premium and commodity pricing.

For teams building commercial plans, negotiating supplier agreements, performing M&A screens or establishing procurement playbooks, PW Consulting’s Sulphur Pastilles Market report provides the analytic foundation and modular tools to act in 2026 with confidence. The full package contains the complete dataset used for our projections, detailed regional and application splits, company profiles and annexed supplier scorecards — information we intentionally withhold in this briefing to preserve the investigative value of the full report.

Request the full report and dataset to access regional/application disaggregation, supplier-level volume estimates and annexed financial modeling templates.

Engage PW Consulting for a tailored session: we can run a bespoke 48‑hour scenario review customizing the demand and price models to your supply contracts and geographies of interest.

Contact your PW Consulting account representative or visit our report page to download the executive summary and arrange a briefing. The complete report contains the granular intelligence required to translate the headline market trajectory into defensible commercial decisions for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Sulphur Pastilles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com