Cultured Wheat Market Outlook 2035: Valuation Expected at USD 1,350.6 Million

Food |

2026-04-28 18:25:17

PW Consulting presents a focused strategic briefing drawn from our full C9 Petroleum Resin Market report. This executive preview synthesizes the market’s macro trajectory, competitive structure, feedstock dynamics, and the high‑leverage decisions company leaders must make in 2026. Our intention is to demonstrate the depth and practical readiness of the full study while preserving proprietary segment-level detail that is available in the complete report on our website.

C9 Petroleum Resin Market

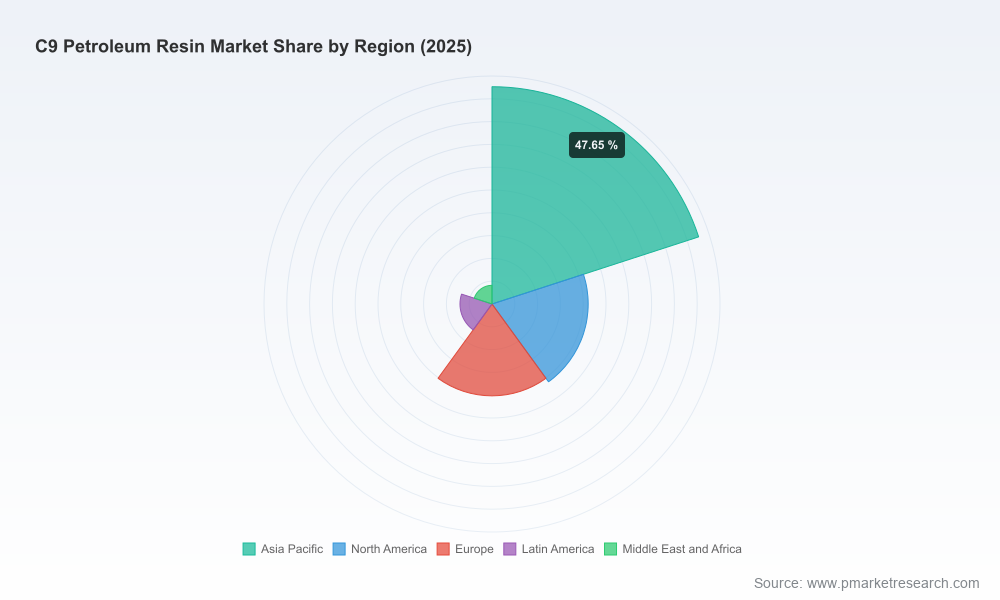

The global C9 petroleum resin market has reached a material scale headed into 2026, with the 2025 base estimated at approximately USD 1.72 billion and a forecast compound annual growth rate (CAGR) of 4.85% through our 2026–2032 projection horizon. By 2032, our baseline scenario anticipates the market to be in the order of mid‑single billions (USD 2.40+ billion under the base forecast).

C9 Petroleum Resin Market

Growth is supported by structural demand from adhesives, paints & coatings, printing inks and rubber compounding, while supply economics remain tightly correlated with the C9 aromatic fraction availability from ethylene crackers and naphtha feedstock cycles.

C9 Petroleum Resin Market

Competitive balance is mixed: a handful of globally integrated and regionally strong producers coexist with sizeable China‑based capacity. The top three and top five suppliers account for a meaningful but not dominant share of industry revenue, leaving room for strategic consolidation, niche premium positioning and regional onshoring plays.

For 2026 strategy, three interacting forces should frame executive decisions: feedstock & upstream integration, product and application differentiation, and geopolitical/regulatory pressures.

Feedstock dependency and volatility — C9 resins are produced from the aromatic C9 fraction, a byproduct of steam cracking. Shifts in global cracker configurations (notably the move toward ethane cracking in some regions) materially reduce C9 byproduct yields versus naphtha cracking, tightening merchant supply and amplifying price sensitivity. Procurement teams should treat C9 availability as a function of regional cracker economics and not merely of installed resin capacity.

Product migration and premiumisation — demand is bifurcating between standard aromatic resins and higher‑value hydrogenated grades or specialty chemistries (e.g., crosslinkable hydrocarbon resins). Applications such as pressure‑sensitive adhesives and high‑performance coatings are increasingly sourced for performance attributes (colour, odour, compatibility) that hydrogenation and tailored polymerisation routes deliver.

Regulation and market access — hydrocarbon resins, including C9 grades, have been assessed as low hazard in recent regulatory reviews and can qualify for certain polymer reporting exemptions under frameworks such as the US EPA TSCA. This reduces near‑term regulatory barriers; however, sustainability expectations and downstream chemical disclosure are rising among major end users, creating a de‑facto market requirement for traceability and lower life‑cycle impacts.

Our full C9 Petroleum Resin Market report is designed for immediate application by strategy, commercial, procurement and M&A teams. Key operational deliverables include:

Market sizing and baseline/alternative scenarios through 2032, including feedstock‑price sensitivity models and margin impact analysis.

Competitive benchmarking with strategic profiles and capability maps for major producers, highlighting relative strengths in feedstock integration, product portfolios and specialty grades.

Supply chain maps and supplier scorecards that rank counterparty risk (feedstock exposure, geographic concentration, contract structures) and identify near‑term pinch points.

M&A and partnership heatmaps that flag targets for bolt‑on acquisitions, tolling arrangements and JV opportunities by region and technology focus.

Commercial playbooks: value‑based pricing frameworks, channel and end‑user segmentation, and negotiation levers for long‑term offtake and tolling contracts.

Capex decision tools and an optimal capacity expansion matrix that balance demand growth, feedstock access and permitting timelines.

Regulatory and sustainability appendices with recommended compliance and disclosure pathways to meet large‑buyer procurement policies.

The C9 resin competitive set comprises integrated global producers, specialty chemical firms, and large regional manufacturers. The market’s structure (top‑three and top‑five concentration in the high‑tens to low‑fifties percentile range) indicates room for strategic consolidation alongside continued competition at the regional level.

Kolon Industries, Inc. (South Korea) — a domestic leader with proprietary crosslinkable hydrocarbon resins and a focus on adhesives, coatings and rubber. Notable for commercialised specialty HCR grades that support higher value applications.

Neville Chemical Company (USA) — an established North American manufacturer of C9 aromatic resins with a long history supplying coatings and adhesives, positioned as a secure domestic supplier for US customers seeking shorter supply chains.

Eastman Chemical Company (USA) — part of a diversified chemicals portfolio; supplies C9 resins among broader hydrocarbon resin offerings and benefits from integrated downstream customer relationships.

Cray Valley (TotalEnergies subsidiary) — global footprint and ongoing investment in resin capabilities, with a strong focus on inks, adhesives and coatings markets.

Exxon Mobil Corporation — integrated producer advantage through captive cracking feedstock, enabling flexible commercial offers and margin management in volatile cycles.

China‑based manufacturers — a group of regional producers supplying competitive standard grades for adhesives, rubber and coatings; these players are important to watch for pricing and contract supply dynamics in Asia and export markets.

Specialised regional players (e.g., Arakawa, Henan producers, ECOPOWER Chem) — offer differentiated grade depth and localised commercial agility.

Companies should craft a multi‑track strategy that balances short‑term resilience and medium‑term value capture. Priority actions for 2026:

Underwrite feedstock access: negotiate tolling and long‑term offtake linked to cracker schedules; evaluate partial vertical integration where feasible to insulate margins from C9 aromatic swings.

Pursue premiumisation: accelerate R&D and commercialisation of hydrogenated and specialty resins (e.g., crosslinkable chemistries) targeted at adhesives and high‑end coatings where higher margins are accessible.

Secure domestic supply solutions: for end‑users in regulated or politically sensitive markets, present onshore or near‑shore supply packages (inventory, guaranteed capacity, emergency allocation) as a differentiator.

Deploy a targeted capex & M&A roadmap: prioritise bolt‑on acquisitions that add specialty grades or increase access to C9 fraction, and consider JVs with cracker operators to stabilise feedstock.

Commercial sophistication: migrate pricing models to value‑based and multi‑year indexed contracts that share upstream volatility with customers while protecting margins.

Operational improvements: implement yield optimisation, feedstock substitution trials and digital forecasting at the plant level to reduce production variance and improve on‑time delivery.

Sustainability & disclosure: prepare supply‑chain transparency assets (LCA snapshots, polymer reporting dossiers) to meet expectations from large downstream buyers despite the current low‑hazard regulatory position.

Risk & scenario planning: run specific scenarios where ethane cracking adoption accelerates or where naphtha shocks cause sharp C9 premium cycles; use these to stress test contracts, inventories and capex phasing.

The report is structured to support four common 2026 decision gates:

Investment Committees — provide the capex sensitivity templates, project NPV under three feedstock scenarios, and a ranked list of expansion projects by strategic fit and payback.

M&A Teams — use the target heatmaps and integration playbooks to accelerate diligence and to size synergies from feedstock access and product portfolio rationalisation.

Commercial & Procurement — deploy the supplier scorecards, contract templates and pricing ladders to renegotiate supplier contracts and to establish customer indexation mechanisms.

R&D and Product Marketing — extract the application demand matrices and priority feature sets to roadmap hydrogenated and crosslinkable grades aligned with end‑user specifications.

PW Consulting’s full C9 Petroleum Resin Market report provides the proprietary segment datasets, supply maps and executable templates referenced in this briefing. For teams setting strategy in 2026 — whether pursuing growth, protecting margins or preparing for M&A — the complete intelligence pack delivers the transaction‑ready detail you will need. To access the full dataset, scenario workbooks and supplier scorecards, please visit our website or contact your PW Consulting account lead.

For detailed analysis of this topic, please visit the official page:C9 Petroleum Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com