Middle East and Africa Remote Patient Monitoring and Care Market Latest Report: Industry Analysis & Growth Forecast

Health |

2026-05-04 12:20:56

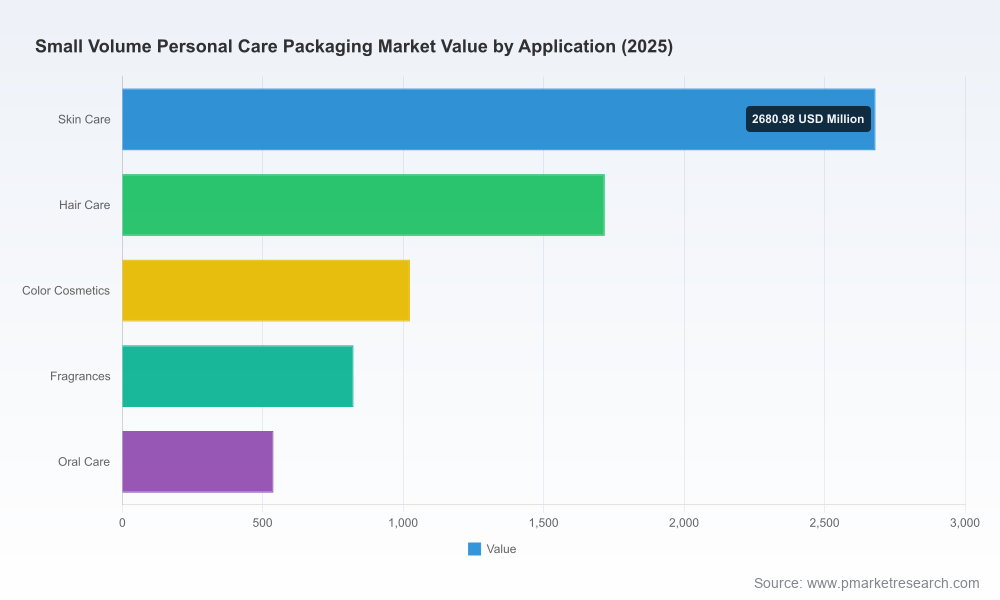

PW Consulting’s new market brief on Small Volume Personal Care Packaging (base year 2025) delivers an executive-grade roadmap for commercial and supply-chain leaders preparing to make critical decisions in 2026. The market reached roughly USD 6.8 billion in 2025 and, under the baseline scenario, is positioned to grow at a mid-single-digit pace (4.4% CAGR) through our 2026–2032 forecast horizon. That growth obscures sharp pockets of opportunity and risk that will determine winners and laggards next year — and this briefing explains where to look and what to do first.

Small Volume Personal Care Packaging Market

Regulatory compression and compliance timelines: Multiple U.S. states have accelerated requirements for post‑consumer recycled (PCR) content and expanded producer responsibility schemes. These changes are not theoretical — they impose discrete timing and cost implications for product design, materials sourcing and labeling across the small‑volume spectrum.

Small Volume Personal Care Packaging Market

Input-cost volatility: Early‑2026 increases in key feedstocks (PE and PP) have re‑ridden packaging cost curves. For manufacturers and brands operating on thin SKU economics in travel, sample and prestige minis, cost swings quickly erode margin and undermine launch plans unless hedging and design flexibility are in place.

Small Volume Personal Care Packaging Market

Channel and consumer shifts: Evolving trial and sampling behavior (subscription boxes, direct-to-consumer sampling, travel and premium gifting) continues to favour compact, differentiated formats — but only for products that marry form, function and sustainability claims credibly.

Market structure: The small‑volume segment remains fragmented — the leading firms hold a modest combined share, leaving space for agile specialists and co‑development partnerships. This fragmentation creates arbitrage for brands seeking bundled offerings (design + filling + sustainable feedstock) from a limited set of preferred partners.

We structured the report to be prescriptive and operational. Buyers, brand teams and M&A strategists will find templates and playbooks rather than high‑level theory. Key deliverables include:

Decision trees and scenario models: Interactive-ready frameworks that translate material price moves, PCR compliance milestones and packaging-format choices into P&L and working-capital outcomes for sample SKUs and mass small-volume SKUs.

Sourcing playbook: A staged supplier engagement plan (pilot → scale) with negotiation playbooks, sample RFP language, and contingency clauses for feedstock scarcity and price escalation.

Sustainability roadmap: A stepwise PCR adoption and recyclability checklist aligned to U.S. state targets and likely near-term EPR obligations — including prioritization guidance by product strategy and channel.

Packaging selection matrix: A decision matrix that maps product viscosity, fill process, marketing intent (trial vs prestige vs travel), and sustainability profile into recommended format families and cap/closure technologies.

Commercialization quick-start: Retail and DTC launch templates tailored for small-volume SKUs — merchandising, sampling economics, unit economics for third‑party fulfilment and launch KPIs to watch in the first 90 days.

Supplier shortlist & capability heatmap: A curated set of potential partners mapped by technical strengths, sustainability credentials and small-MOQ capability. (Note: the full shortlist and scoring rubric are reserved for subscribers.)

The competitive field is diverse: global converters with beauty roots, flexible-pack leaders, specialist unit-dose providers, and dispensing innovators. Strategic implications for 2026 center on partner selection, co‑development and capability stacking.

Albéa Group (France) — A leading beauty-packaging specialist with a clear focus on low‑MOQ, travel and mini formats. Albéa’s strength is in combining prestige aesthetic options with increasingly recycled-content resins; they are a logical partner for brands that require differentiated design and small test runs.

Aptar Beauty (United States) — A technology-first supplier known for dispensing solutions optimised for small volumes (airless, pocket pumps and micro dispensers). Recent innovations underline Aptar’s role where dosing precision, hygiene and premium delivery matter.

Silgan Dispensing (United States) — Concentrates on travel-size and sampler formats, offering airless and spray miniaturized systems. Silgan is a practical choice for brands looking to scale sampler programs and travel assortments quickly.

Berry Global (United States) — Offers an expanding range of compact sizes and recycled-content options; Berry is positioned where scale, circular product lines and refillable stick formats intersect with large CPG needs.

HCP Packaging (United Kingdom) — Specialist in compacts, palettes and pocket formats for color cosmetics — valuable for brands that need integrated decorative finishing and small-batch color customization.

Amcor (Switzerland) — A flexible-pack leader providing sachets, pouches and paper-based alternatives. Amcor’s capabilities are especially relevant to sampling and engineering paper-backed solutions that meet curbside recyclability goals.

Gerresheimer (Germany) — A glass and specialty plastic producer with lightweighting capabilities suitable for small-volume serums and fragrances where perceived value is tied to glass finishes.

Unit Pack and JP Packaging (United States) — Unit‑dose and sachet specialists who serve trials, medical-adjacent personal care and single-use formats. Their value is speed-to-market and minimal capital commitment for filling trials.

Together, these players make clear that there is no single “one-size-fits-all” supply route. Our analysis shows top-three and top-five market concentration metrics that confirm the category’s fragmentation: leaders hold modest cumulative shares, which stresses the importance of strategic partnering for scale or differentiation.

PCR mandates and EPR timelines require brands to map reformulation and packaging updates onto product roadmaps now — not in late 2026. Several U.S. states have adopted staged PCR content requirements, and producer responsibility schemes are expanding; compliance calendars should be a formal input to SKU roadmaps.

Material-price pressure in early 2026 — particularly PE/PP — underscores the need for contract hedging, multi-sourcing and rapid design-for-substitution playbooks (e.g., switching to recycled feedstock blends or alternative substrates where feasible).

Claims and recyclability: “Recyclable” and PCR claims will be scrutinized by both regulators and consumers. Brands must document chain-of-custody and end-of-life outcomes to protect claims and avoid costly rework.

Institute a packaging compliance calendar: Convert legal timelines (PCR targets, EPR enrollments, reporting start dates) into procurement milestones and contractual trigger points for packaging contracts and reformulation windows.

Pilot a “PCR first” SKU suite: Select high-visibility SKUs (travel, sample, prestige minis) to pilot increased PCR content alongside a consumer‑facing sustainability narrative. Use controlled A/B testing to measure perception and return on marketing spend.

Adopt modular sourcing: Negotiate framework agreements that enable low-MOQ design runs with clear escalation terms. This preserves agility while locking in price floors or cap structures against feedstock volatility.

Co‑develop dispensing intelligence: For high‑value serums and dermocosmetics, prioritize supplier partners with micro‑airless or precision dispense tech to protect product integrity and justify premium price points.

Run a focused M&A and partnership screen: Given the market’s fragmentation, acquisitions of niche converters or long‑term co‑development partnerships can shorten time-to-market for novel materials and differentiated formats.

Our research product is designed as a blended intelligence and execution package. Subscribers receive the full dataset, a supplier short list with qualification scores, editable scenario models, and a 90‑day implementation playbook for packaging pilots. We keep the granular segmentation and supplier‑level scoring behind the paywall so that decision‑grade work products remain an exclusive tool for our clients and subscribers.

For procurement, R&D, brand and investor teams planning 2026 initiatives, this report converts regulatory calendars, material-cost scenarios and supplier capabilities into a single prioritized action plan. The result: faster, lower‑risk SKU launches and a defensible cost/sustainability roadmap.

Download the full report to access the complete segmentation tables, supplier scoring, detailed price decks and the executable sample RFPs that we reference here.

Schedule a 45‑minute advisory session with PW Consulting to map the report’s findings directly onto your 2026 SKU roadmap and supplier negotiations.

PW Consulting’s Small Volume Personal Care Packaging brief is intentionally tactical — designed to inform immediate procurement decisions and to shape 2026 product and portfolio moves. The macro trajectory is positive, but success next year will favor teams that combine regulatory foresight, supplier co‑development and disciplined cost management. Our report gives you the framework and the tools to be one of them.

For detailed analysis of this topic, please visit the official page:Small Volume Personal Care Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com