Holiday Home Market Latest Trend, Growth, Size, Application & Forecast by 2031

Other |

2026-02-26 06:43:16

As a specialized, high-impact niche within respiratory and transplant medicine, the Bronchiolitis Obliterans Syndrome (BOS) market is entering a pivotal commercial and clinical inflection between 2026 and 2032. Our report (base year 2025; historical window 2020–2025; forecast 2026–2032) projects steady expansion at a compound annual growth rate (CAGR) of 6.5%. Measured in USD (Million), the global market is estimated at USD 385.0 Million in 2025 and is modeled to grow to approximately USD 410.03 Million in 2026, reaching USD 598.31 Million by 2032 under the central-case scenario.

Bronchiolitis Obliterans Syndrome Market

This briefing highlights why the PW Consulting Bronchiolitis Obliterans Syndrome Market report is an essential strategic input for executive teams, corporate development, pipeline portfolio managers and payers planning decisions in 2026. It demonstrates the timing and nature of near-term value-creating events, the levers that will determine adoption of novel BOS therapies, and the pragmatic commercial strategies that will separate winners from laggards—without revealing the confidential subsegment matrices contained in the full report.

Bronchiolitis Obliterans Syndrome Market

Timing of clinical readouts and corporate moves: The BOS landscape in 2026 is defined by Phase 2–3 activity and targeted corporate transactions that materially alter risk/return profiles for emerging therapies. Our report synthesizes clinical timelines with financing and M&A events to indicate where value will crystallize over 12–24 months.

Bronchiolitis Obliterans Syndrome Market

Regulatory and reimbursement tension: There are currently no FDA-approved therapies specifically for BOS, and several leading pipeline candidates hold Orphan Drug / Fast Track designations. That regulatory backdrop creates both accelerated pathways and payer negotiation risk—nuances we model across multiple reimbursement scenarios.

Evidence-driven commercialization: Given the relatively modest overall market scale today but durable growth potential, the path to commercial success hinges on differentiating clinical benefit (lung function, exacerbation reduction, tolerability) and on early payer engagement. The report provides playbooks for evidence generation and value demonstration tailored to BOS’s unique economics.

Clinical pipeline convergence. Several programs approaching/entering late stages are positioned to change the therapeutic standard for BOS post-transplant. Of particular note are inhaled-localized immunomodulatory approaches and oral small molecules targeting inflammatory and fibrotic pathways. The full report maps each candidate to expected readouts, regulatory designations and commercial milestones.

Notable corporate catalysts. Recent and near-term events matter materially:

Zambon’s inhaled liposomal cyclosporine A (L-CsA-i) advanced through pivotal Phase 3 BOSTON trials and remains the most mature inhaled program for BOS post-lung transplant.

Quince Therapeutics completed a transformational step in May 2026 by acquiring OrphAI Therapeutics and securing up to $187M to accelerate LAM-001 (inhaled sirolimus) Phase 2 development; top-line/expanded data are expected in Q1 2027.

Incyte has published Phase 2 multicenter data demonstrating lung function improvements with ruxolitinib in BOS after allogeneic hematopoietic cell transplant (HCT), underscoring the clinical relevance of JAK inhibition in this indication.

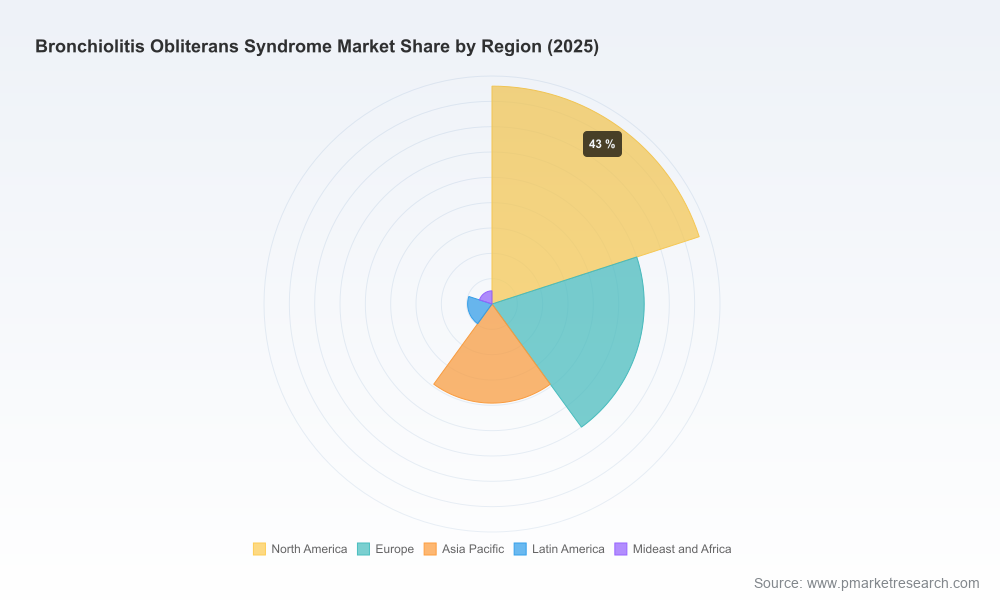

Unmet need and patient flow. BOS continues to affect a substantial share of lung transplant recipients within five years post-transplant, sustaining baseline demand tied to annual transplant volumes in high-income markets. The lifetime clinical and economic burden for affected patients is high, which can support premium pricing for truly disease-modifying therapies—if value is convincingly demonstrated.

Market structure and concentration. Market concentration is meaningful but not monopolistic; incumbent advantages exist in clinical relationships, transplant center networks, and inhalation-device expertise. The report’s competitive chapter combines concentration metrics with qualitative capability maps to help buyers and sellers size opportunity and defensibility.

Reimbursement and access risk. High treatment costs and unclear reimbursement pathways for innovative BOS therapies will drive heterogeneity in adoption across geographies. The report includes payer-scenario models and HTA risk matrices to quantify how coverage decisions and indication-limited approvals could re-shape near-term revenue trajectories.

Zambon (Milan, Italy) — Advancing L-CsA-i (liposomal cyclosporine A for inhalation) in Phase 3 (BOSTON-1/2) and extension trials as a potential first approved inhaled therapy for BOS post-lung transplant. Its clinical maturity and regulatory designations make it a reference case for inhaled local therapies.

Quince Therapeutics (South San Francisco, CA, USA) — Through the May 2026 OrphAI acquisition and associated financing, Quince is advancing LAM-001 (inhaled sirolimus) in Phase 2 with data anticipated in early 2027; this program reshapes comparative positioning for inhaled mTOR inhibition.

Incyte Corporation (Wilmington, DE, USA) — Ruxolitinib’s Phase 2 signals in post-HCT BOS establish a credible systemic therapy pathway, particularly for non–lung-transplant BOS populations and combination strategies.

Genentech (Roche) and GlaxoSmithKline (GSK) — Both incumbents maintain respiratory and immunomodulatory R&D efforts that could be strategically redirected into BOS-relevant combinations or platform support (e.g., anti-fibrotic/anti-inflammatory modalities), creating potential for licensing or co-development plays.

Implication for partners and acquirers: Buyers should prioritize assets with differentiated delivery (inhalation), a clear clinical differentiation vs. standard-of-care, and a realistic payer dossier. The report’s M&A decision framework scores targets on clinical readout timing, regulatory optionality, payer risk and manufacturing readiness.

Bottom-up market sizing and scenario-based forecasts for 2026–2032 (currency: USD, revenue unit: Million), with sensitivity tests for conservative, base and upside cases aligned to clinical-event calendars.

Clinical trial tracker and product-by-product value map that align mechanisms, routes of administration and pivotal readouts to commercialization risk and estimated time-to-peak revenue.

Regulatory pathway analysis (including orphan and expedited pathways), submission playbooks and recommended meeting strategies for FDA/EMA interactions.

Payer and HTA playbooks with modular evidence packages, real-world evidence (RWE) generation plans, and pricing/reimbursement scenario modelling for major markets.

Commercial go-to-market templates by payer archetype and transplant center ecosystem: prioritized account lists, captive center engagement sequencing, and sample contracting structures.

Corporate strategy tools: M&A target screens, licensing scorecards, and post-merger integration considerations specific to inhalation formulation scale‑up and specialist-clinic channel roll-out.

Risk matrices and mitigation playbooks covering clinical, regulatory, manufacturing and reimbursement failure modes, and tactical mitigation options for each.

Allocate capital to late‑stage inhalation platforms with rapid path-to-market and clear differentiation versus systemic therapy—while preserving optionality for combination approaches.

De-risk launch plans by building payer-facing evidence packages before pivotal readouts; invest in RWE partnerships at high‑volume transplant centers to shorten time-to-reimbursement.

Use event-driven investment gates: prioritize deals and expenditures around key clinical readouts (e.g., 2026–2027 window) and structured milestone-based financing to preserve upside while limiting downside.

Prepare commercial operations for specialty-channel launches (transplant center networks, post‑transplant clinics), including device supply chains and training programs for inhaled therapies.

For investors and M&A teams: target assets with one or more of the following—near-term clinical readout, favorable regulatory designations, scalable manufacturing for inhaled formulations, and a credible payer dossier ready for rapid submission.

This briefing is intentionally selective: it highlights the structural drivers, the tactical windows and the corporate implications you need to orient 2026 strategy, while reserving detailed segment tables, regional splits and transaction-level financial modeling for the full report. The PW Consulting Bronchiolitis Obliterans Syndrome Market report contains the granular data, modeled scenarios and downloadable tools (forecast spreadsheets, HTA scorecards, trial timelines) that your team can operationalize immediately.

For a tailored executive briefing, model walkthrough, or to license the full report and data pack, contact PW Consulting’s Life Sciences Strategy practice. We will map the market intelligence to your portfolio, run bespoke payer-scenario simulations, and deliver a decision-ready plan aligned to your 2026 priorities.

For detailed analysis of this topic, please visit the official page:Bronchiolitis Obliterans Syndrome Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com