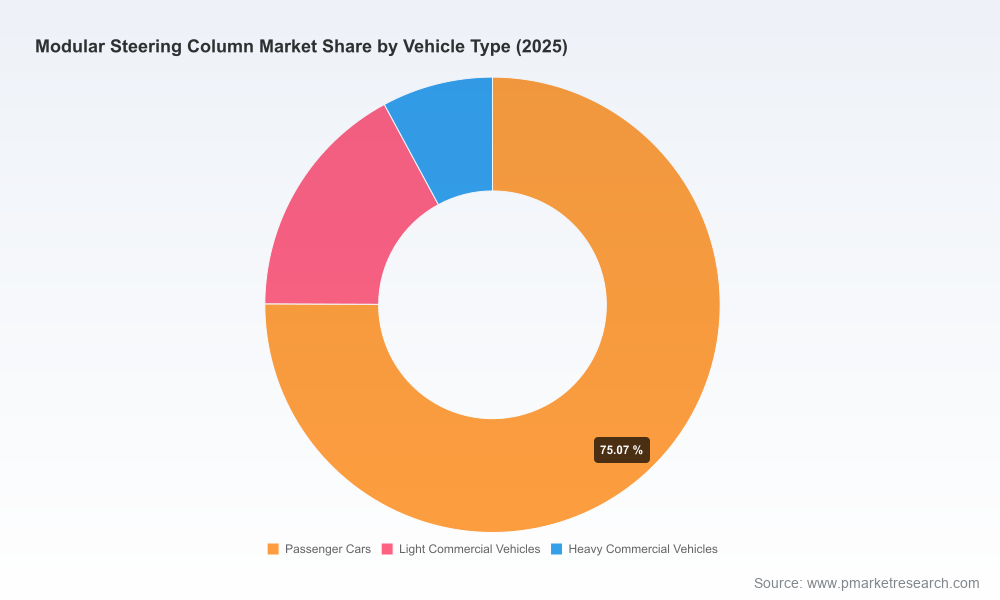

Modular Steering Column Market — Strategic Briefing for 2026 Decision-Makers

Executive summary

PW Consulting’s latest market study on the Modular Steering Column market positions buyers, OEM program teams, and tier‑1 strategists to make decisive moves in 2026. Built on a 2025 base year and a 2026–2032 forecast horizon, the report quantifies the market’s multi-year momentum and projects a compounded annual growth rate of 5.96% across the forecast window. Our scenario modelling shows continued expansion driven by electronic integration, lightweighting and regulatory safety requirements — trends that will reshape supplier capabilities, design roadmaps and sourcing strategies through the end of the decade.

Modular Steering Column Market

Why this matters in 2026

2026 is a pivot year for vehicle architecture choices. Electrification programs are moving from pilot to volume, OEMs are standardizing domain controllers and electrical architectures, and safety and functional‑safety compliance (ISO 26262) is being embedded earlier in product development. For steering columns — a component traditionally defined by mechanical form and adjustability — 2026 will be the year where modular electronic functionality, weight optimization and supplier integration determine who captures program wins.

Modular Steering Column Market

What PW Consulting’s report delivers (practical, decision‑ready content)

- Market sizing and topline forecasts (base year 2025) with scenario bands for conservative, base and aggressive adoption through 2032, enabling CAPEX and purchasing planning aligned to likely program volumes.

- Demand drivers analysis linking vehicle electrification, interior ergonomics, and regulatory safety standards to steering column content per vehicle and total addressable market evolution.

- Detailed supplier intelligence: comparative capability maps, manufacturing footprints, cost‑to‑serve heat maps, and integration risk scoring for the leading global suppliers.

- Technology and materials playbook: assessment of electric adjustment systems, tilt/telescope integration approaches, and lightweight materials (magnesium, aluminum, engineered plastics) with guidance on tradeoffs for mass, cost and crash performance.

- Functional‑safety and compliance checklist: practical steps to ensure ISO 26262 alignment for electronic control modules and to meet FMVSS crash energy absorption requirements.

- M&A and partnership screening toolkit: criteria to evaluate bolt‑on acquisitions or JV candidates to accelerate modular architecture capabilities.

- Procurement levers and supply‑chain resilience models: commodity exposure analysis, hedging strategies for light‑metal inputs, and near‑sourcing vs global sourcing tradeoffs.

- Appendices with primary research transcripts, test protocols, and a catalogue of OEM program launch windows (note: full segmentation tables and granular regional/application revenue splits are available in the full report).

Market dynamics at a glance

The market’s steady growth reflects a confluence of forces: increased content per vehicle as electronic locking, motorized tilt/telescope and integrated controls become standard; material substitution to meet weight targets; and supplier consolidation where system-level capabilities are prioritized over commodity components. Concentration metrics indicate a market where the top three suppliers control a meaningful share, and the top five capture solid majority positioning — a structure that favors large tier‑1s able to offer system integration, crash performance verification and global program support.

Modular Steering Column Market

Competitive landscape — what the leading players are positioning for

Our industry mapping identifies distinct strategic postures among the market leaders:

- Nexteer Automotive — Leveraging a broad portfolio and recent launches (including high‑output column‑assist electric power steering showcased at Auto Shanghai in 2025), Nexteer is doubling down on scalable EPS modules designed for flexible vehicle integration. Their strength: modular EPS architectures that can be tuned across vehicle segments.

- thyssenkrupp AG — Focused on adaptive crash behavior and premium segment requirements, thyssenkrupp’s modular columns emphasize differentiated energy absorption and integration with restraint systems for safety‑sensitive platforms.

- Kongsberg Automotive — A niche leader for off‑highway and commercial applications, Kongsberg builds bespoke tilt/telescope modules from modular platforms with strong in‑house validation capabilities that appeal to commercial OEMs with demanding duty cycles.

- Merit Automotive — Plays to a complexity reduction strategy, integrating security and convenience features across modular variants to simplify wiring and manufacturability for high‑variant programs.

- NSK Ltd., Robert Bosch, ZF, JTEKT, Hyundai Mobis and Mando — Each pursues variants of systems integration: NSK with lightweight plastic impact solutions; Bosch and ZF with lightweight and maintenance‑free concepts for commercial vehicles; JTEKT integrating columns into broader EPS/HPS portfolios; Hyundai Mobis and Mando emphasizing platform supply to global OEMs with integrated chassis and safety systems.

Collectively, these firms illustrate two clear competitive paths: volume suppliers who optimize cost and modularity for passenger platforms, and specialized suppliers who prioritize certification, crash behavior and durability for commercial and luxury segments.

Regulation, materials and technical constraints

Two regulatory pillars shape product and program decisions: historic crash performance standards requiring controlled energy absorption and rearward column displacement mitigation, and functional‑safety standards governing electronic control modules and signal routing. These rules raise the bar on validation timelines and design verification, favoring suppliers that can demonstrate robust crash test evidence and ISO 26262 processes early in the bid phase.

On materials, industry technical literature and supplier disclosures underscore a clear shift toward magnesium and aluminum alloys, combined with engineered plastics, to reduce mass while preserving crash performance. Magnesium’s favorable strength‑to‑weight ratio enables substitution of heavier ferrous parts in targeted subcomponents, but introduces supplier concentration and cost volatility risks that procurement teams must actively manage.

Strategic implications and recommended actions for 2026

- Embed modularity in early architecture choices: Require modular column interfaces in platform architecture reviews for 2026 program bids. This reduces late‑stage redesign and shortens supplier qualification timelines.

- Prioritize suppliers with integrated validation capability: When evaluating tier‑1 partners, weight certification history, in‑house crash test facilities and ISO 26262 evidence more heavily than unit price for long‑lead safety systems.

- Lock material supply for light‑metal inputs: Implement dual‑sourcing and material hedging strategies for magnesium/aluminum to stabilize cost and delivery; consider strategic contracts with metal fabricators that can provide alloy consistency and processing expertise.

- Accelerate electronic integration roadmaps: For programs where steering columns become part of domain control, require suppliers to demonstrate software partitioning, secure over‑the‑air update pathways and functional‑safety traceability.

- Use CR‑based benchmarking in supplier selection: Given the market concentration, structure RFPs to differentiate between global system integrators and regional specialists; construct margin models that account for system integration premiums.

- Prepare for consolidation and partnership plays: Evaluate M&A or JV opportunities with specialist suppliers to acquire validation capabilities or niche product lines that shorten time‑to‑market for new architectures.

How to use the full PW Consulting report

This briefing highlights the strategic contours you need to act in 2026. The full report contains the detailed supporting evidence you will require to operationalize these recommendations: program‑level demand models, supplier cost‑to‑serve matrices, verification timelines aligned with FMVSS/ISO milestones, and scenario spreadsheets you can adapt to your specific program mix. To maintain the “trailer” integrity of this briefing, we have withheld granular regional and application revenue tables and the complete segmentation datasets; those are included in the full report package available on our release page.

Next steps

- Request the report package to access the segmentation appendices, supplier scorecards and the Excel modelling toolkit.

- Schedule a strategy workshop with PW Consulting to translate the findings into a 90‑day action plan for your 2026 program portfolio.

- Engage our supplier due‑diligence team for rapid validation of shortlisted partners against crash, functional‑safety and manufacturing readiness criteria.

PW Consulting’s Modular Steering Column Market report is crafted to be an operational playbook for 2026 decisions: it translates market momentum and regulatory pressures into concrete procurement, engineering and corporate development moves. For program teams and executive sponsors, the value is immediate — clearer supplier choices, defensible investment timing, and a roadmap for integrating emerging materials and electronics without compromising safety or time‑to‑market.

For detailed analysis of this topic, please visit the official page:Modular Steering Column Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com