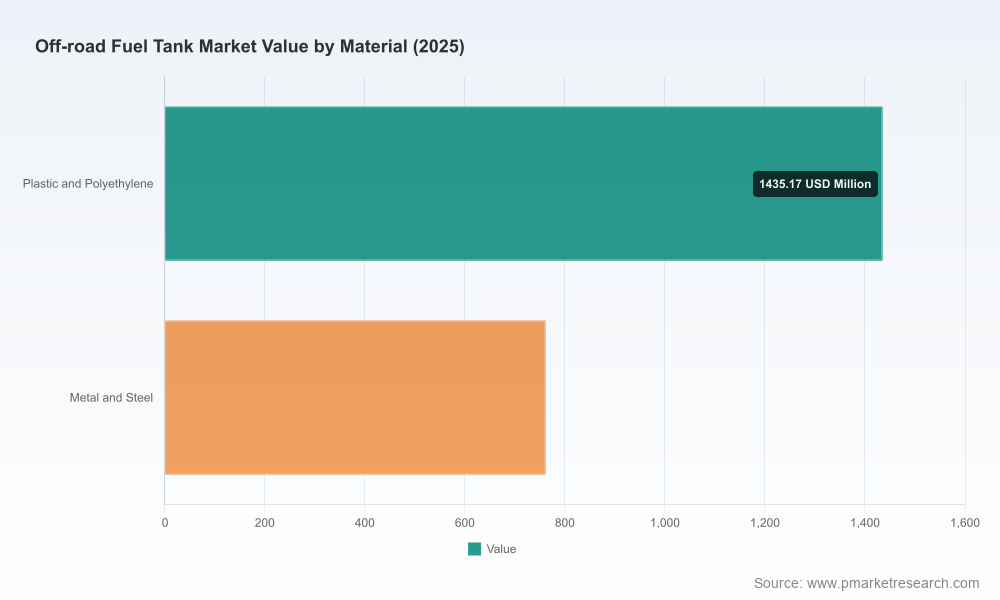

PW Consulting: Off‑Road Fuel Tank Market Set to Reach USD 3,191.34 Million by 2032, Expanding at a 5.48% CAGR (2026–2032)

Other |

2026-07-01 09:48:10

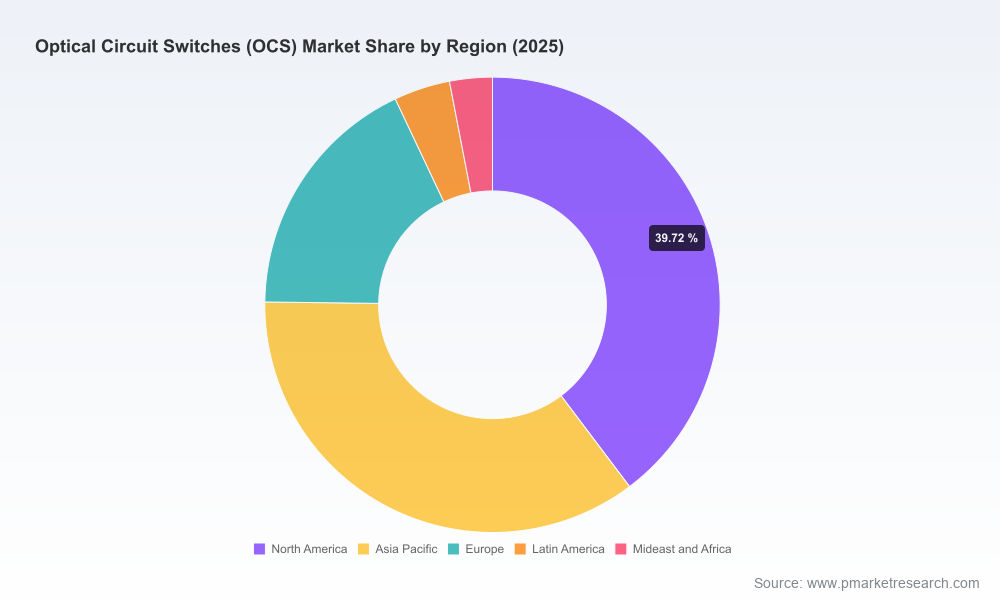

Optical Circuit Switching (OCS) is transitioning from specialist testbeds to strategic infrastructure in AI-scale data centers, hyperscale cloud fabrics and next-generation carrier networks. PW Consulting’s latest market assessment — based on a 2025 base year and covering the 2020–2025 historical window with a 2026–2032 forecast — quantifies an accelerated adoption curve. The addressable market reached a substantial multi-hundred million USD scale by 2025 and, with a compound annual growth rate (CAGR) of 20.5% in our forecast horizon, is projected to expand materially through 2032. For executives building 2026 investment priorities, this report highlights where OCS shifts from experimental to mission-critical and how this timing should influence architecture, procurement and partner strategies.

Optical Circuit Switches Ocs Market

AI-driven traffic patterns. Generative AI and large-model training place unique demands on east-west bandwidth and low-latency interconnects. OCS enables high-radix, low-power optical fabrics that address these demands in ways electrical switching cannot economically match at scale.

Optical Circuit Switches Ocs Market

Energy and operating-cost pressure. Large data centers allocate a major share of operating budgets to electricity; industry analyses show data center electricity demand and costs climbing as AI workloads expand. OCS delivers a path to lower interconnect power draw and operating expenditure when deployed strategically at rack and pod aggregation layers.

Optical Circuit Switches Ocs Market

Standards and interoperability momentum. Initiatives such as the Open Compute Project’s OCS sub-project are reducing integration friction and accelerating production adoption by clarifying interfaces, control-plane expectations and test methodologies — turning proof-of-concept wins into repeatable deployments.

PW Consulting’s modeling — anchored to a 2025 base year and a 20.5% CAGR across the forecast period — shows the OCS market scaling rapidly from a niche equipment category to a core fabric technology in selected high-performance environments. The growth rate reflects a compound effect of accelerating AI workloads, vendor product maturation (higher radix, lower insertion loss, improved reliability), and infrastructure operators’ desire to cap energy and cabling complexity. For corporate strategy teams, the headline implication is clear: capital planning cycles that ignore OCS as a viable chassis-level alternative risk missing a cost and performance lever that will be material to TCO by 2028–2030.

Data center topology optimization. Organizations must re-evaluate rack-to-rack and pod-to-pod topologies with OCS capabilities in mind. In early adopter deployments, hybrid electrical/optical fabrics are the pragmatic near-term posture — reserving OCS for high-bandwidth, latency-sensitive clusters while maintaining electrical switching for control and low-utilization traffic.

CapEx vs. OpEx trade-offs. While OCS introduces incremental capital expense and integration complexity up front, the medium-term operational savings — driven by lower power, reduced cooling load and simplified high-density cabling — can materially alter lifecycle economics for AI-heavy workloads. Procurement teams should adopt total-cost-of-ownership (TCO) modeling that includes power, space and expected utilization profiles over 5–7 years.

Procurement and vendor selection posture. With market concentration indicative of an emerging oligopoly among specialist OCS vendors and established optical suppliers, buyers should pursue multi-vendor proofs-of-concept (PoCs) and insist on interoperability validations (OCP profiles, control-plane APIs) as part of RFx processes.

Operational readiness and skills. Successful OCS rollouts require cross-disciplinary capabilities: optical-layer engineering, automation and orchestration, and systems integration. Organizations should invest in pilot programs and staff upskilling in 2026 to avoid schedule slippage when scaling in 2027–2028.

The OCS supplier ecosystem is a mix of established photonics incumbents and nimble specialists. Key vendors highlighted in our analysis demonstrate differentiated approaches and clear strategic positioning:

Lumentum Holdings: Focused on high-radix MEMS-based platforms optimized for AI and cloud fabrics, partnering across the optics stack to deliver low-power, rack-level solutions.

Coherent: Leveraging liquid-crystal and LCoS techniques with an emphasis on low-latency, high-reliability systems for AI data center architectures.

Molex: Pursuing high-port-count MEMS platforms with engineering roadmaps that target very large, reconfigurable fabrics designed for GPU cluster scaling.

DiCon Fiberoptics and others: Delivering value-focused MEMS solutions that emphasize proven reliability and competitive economics for data center deployments.

HUBER+SUHNER Polatis, Telescent, Calient, iPronics, Omnitron Sensors: Each brings a distinct technological axis — beam steering, robotic fibre switching, silicon photonics, and advanced MEMS mirror tech — creating a competitive landscape where architectural fit and integration breadth matter as much as raw component specs.

Recent market activity reinforces this competitive dynamism: new product launches and demonstrations of integrated rack-level solutions have accelerated in early 2026, and partnerships to scale PIC manufacturing suggest supply-chain momentum toward production volumes. For procurement teams, the immediate implication is two-fold: (1) prioritize vendors that demonstrate system-level maturity and partner ecosystems; (2) design PoCs that exercise not only switch performance but orchestration, monitoring and failure-mode behavior.

Grid and energy policy will shape deployment geographies. Jurisdictional rules around renewable sourcing and grid capacity — for example, recent national and regional measures that tie data-center permitting or operation to renewable procurement — will influence where OCS-enabled expansion delivers the best ROI.

Standards activity reduces integration risk. Ongoing workstreams in standards bodies and projects such as the Open Compute Project’s OCS effort are lowering barriers to multi-vendor integration and creating common control-plane expectations. Organizations should align pilot APIs and telemetry plans to these community standards to future-proof integrations.

Scope selection: target high-utilization AI clusters or cross-pod training fabrics where bandwidth demands and power costs make the OCS value proposition most visible.

Measurement framework: baseline power, latency, utilization and orchestration overhead pre-deployment and track these against a multi-month window. Include failure injection to quantify operational impact of optical-layer faults.

Integration: validate control-plane APIs, telemetry export and orchestration compatibility with existing NFV/SDN systems. Insist on vendor support for automated provisioning and rollback in the PoC contract.

Procurement clauses: include milestones tied to interoperability tests, performance SLAs and spare-part logistics to mitigate early-adopter supply risks.

Our full report is organized to support immediate 2026 decision-making with a mix of strategic analysis and hands-on tools:

Market sizing and scenario models calibrated to workload trajectories and energy cost assumptions, enabling TCO comparisons between electrical, hybrid and full-optical interconnect designs.

Vendor profiles and a comparative framework that evaluates suppliers on architecture fit, roadmap maturity, integration readiness and support models — including recent product and partnership developments through early 2026.

Deployment playbooks: step-by-step guidance for PoC design, measurement metrics, operational readiness checklists, and contract negotiation templates tailored to different buyer archetypes (hyperscaler, cloud operator, large enterprise, research campus).

Risk registers and mitigation strategies covering supply chain, standards evolution, energy/regulatory shifts and operational failure modes.

To preserve competitive value for purchasers and partners, the report intentionally withholds certain granular regional and application revenue splits in public summaries; subscribers receive full segmentation tables and scenario workbooks to model specific deployment plans.

Prioritize targeted PoCs this year. Begin with limited-scope pilots in clusters with clear bandwidth and energy stress to produce measurable TCO evidence within 6–12 months.

Insist on standards alignment. Make OCP and open API conformance a must-have in vendor selection to reduce lock-in and integration timeline risk.

Use TCO models that extend to 7 years and include power, space and expected scaling. Short-cycle procurement decisions based purely on upfront CAPEX will misstate the economic benefits of OCS.

Build cross-functional squads. Combine data-center ops, network engineering and automation teams to own pilot outcomes and to accelerate ramp if results validate expectations.

OCS is no longer an experimental sidebar in the optics literature; it is emerging as a strategic lever for organizations grappling with exploding east-west traffic patterns and rising energy costs. With market momentum quantified by a double-digit CAGR from the 2025 base and a wave of product and manufacturing developments through early 2026, senior leaders should treat OCS readiness as a discrete planning line in 2026 budgets. Those who begin disciplined, standards-aligned pilots this year will have the integration experience and data to make high-confidence scale decisions as the market matures through the close of the decade.

For a complete set of segmentation tables, vendor scorecards, PoC templates and the full scenario models referenced in this briefing, visit the PW Consulting report page or contact our advisory team. Our subscribers receive the full dataset and customizable workbooks needed to convert the strategic conclusions above into operational roadmaps tailored to their facilities and workloads.

For detailed analysis of this topic, please visit the official page:Optical Circuit Switches Ocs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com