North America Mobile Solar Systems Market to Reach $1.4 Billion by 2031 as Demand for Portable Clean Energy Surges

Other |

2026-05-26 06:10:28

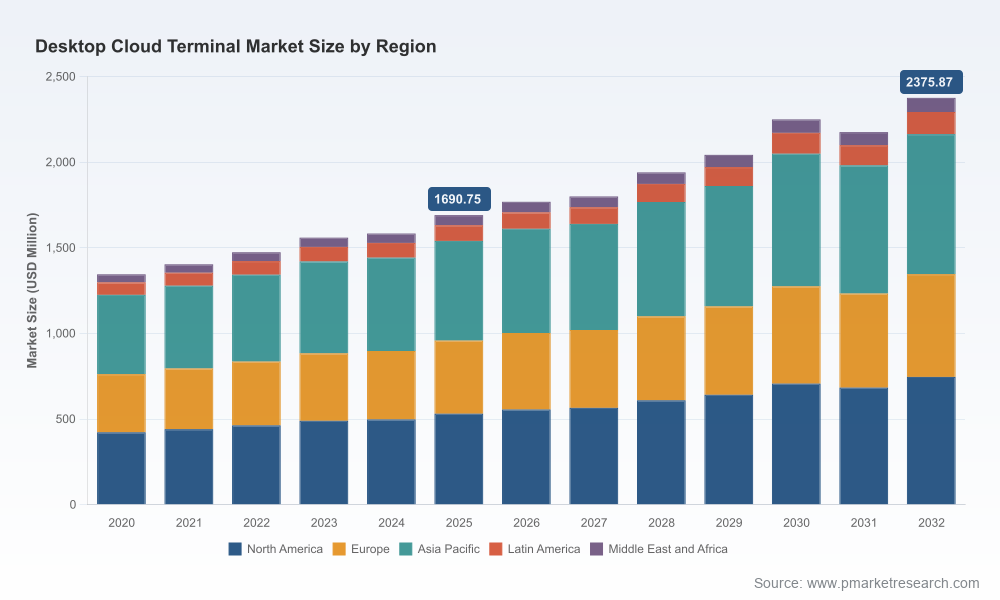

PW Consulting’s latest Desktop Cloud Terminal Market study (base year 2025, forecast 2026–2032) reframes how CIOs, procurement leaders, and security architects should think about endpoint modernization entering 2026. The global market reached roughly USD 1.69 billion in 2025 and is projected to grow at a steady 4.98% CAGR through our forecast window — a trajectory that underwrites continued vendor investment, product innovation, and accelerating enterprise migration from traditional PCs to cloud-delivered desktops. Our analysis combines macro sizing, vendor competitive mapping, regulatory and infrastructure dynamics, and practical deployment playbooks designed to convert strategic intent into measurable outcomes.

Desktop Cloud Terminal Market

Budget windows: The market’s steady growth validates multi-year procurement strategies that shift spend from capex-heavy refresh cycles toward cloud-enabled, lifecycle-managed endpoints.

Desktop Cloud Terminal Market

Security posture: With regulatory pressure (notably EU Data Governance rules and CISA’s Zero Trust guidance) and Fortune 500 adoption trends moving away from on-prem desktops, endpoint architecture is now a frontline security decision, not an IT convenience.

Desktop Cloud Terminal Market

Operational resilience: Rising data-center energy costs and geopolitical constraints on high-performance hardware mean enterprises must balance performance, cost, and supply-chain risk when selecting cloud terminals and delivery arrangements.

PW Consulting’s brief is structured to bridge strategy and execution. We deliver a single-source playbook that includes:

Validated market sizing and scenario modelling — near-term (2026–2028) and strategic (2029–2032) scenarios that stress-test demand under different macro and technology inflection points.

Vendor scorecards and competitive positioning — objective assessments of product fidelity, protocol support, management tooling, and go-to-market strategy across incumbent OEMs and emerging vendors.

Procurement and TCO frameworks — practical templates to compare capex, lifecycle management, DaaS options, network and data-center costs, and the impact of energy pricing on hosting economics.

Security and compliance playbooks — mapped controls to CISA Zero Trust principles, controls for data sovereignty (as shaped by EU rules), and operational checklists for secure VDI/DaaS rollouts.

Architecture decision trees — guidance for hybrid deployments (local processing vs. thin/zero clients, ARM-based endpoints, GPU offload), latency budgeting, and multi-cloud vs. private-cloud tradeoffs.

Supply-chain risk matrix — mitigation tactics for export-control exposure, component shortages, and regional sourcing alternatives.

Industry use-case templates — sector-specific deployment models for enterprise, education, healthcare, and government, with measurable KPIs for cost, security, and user experience.

The desktop cloud terminal market shows moderate concentration. The top three vendors account for a meaningful portion of market activity, and the top five consolidate a clear majority — a structure that influences negotiation dynamics, OEM roadmaps, and partner ecosystems.

Dell Technologies — Dell’s Wyse family continues to be a reference point for large-scale virtualization rollouts, particularly where multi-monitor support and deep integrations with Windows 365 Cloud PC matter. Recent product refreshes reinforce Dell’s edge in environments prioritizing broad enterprise integrations and ISV certifications.

HP Inc. — HP’s thin- and zero-client lines emphasize compatibility and certification with major VDI platforms. HP’s recent certification upgrades signal continued investment in platform validation, which reduces integration risk for buyers standardizing on Citrix, VMware, or Microsoft stacks.

Lenovo Group — Lenovo’s approach blends endpoint diversity with channel-led distribution and engineering focus on low-power compute profiles. Updates that leverage modern processors indicate Lenovo’s intent to capture workloads that require more local processing without forfeiting the benefits of centralization.

IGEL Technology — IGEL’s thin clients and OS-led strategy bring security-first features and protocol parity across clouds, which is attractive for organizations prioritizing zero-trust and device lifecycle management as core differentiators.

10ZiG Technology — As a specialized provider of zero and thin clients, 10ZiG emphasizes protocol performance and focused VDI compatibility — a compelling option for performance-sensitive virtual desktop deployments.

Huawei Technologies — Huawei’s portfolio couples cloud desktop compatibility with a regional channel presence. Buyers evaluating multi-regional deployments should explicitly account for geopolitical and supply considerations when weighing such platforms.

Acer — Acer positions itself as a cost-competitive alternative with straightforward integration into DaaS and VDI stacks, often favored in education and mid-market deployments where unit economics drive decisions.

Dell’s late-2025 Wyse refresh improves multi-monitor and Cloud PC integration — a timely capability for firms standardizing on desktop-as-a-service.

HP’s Citrix certifications strengthen assurances for enterprises reliant on validated platforms and reduce risk in heterogeneous environments.

IGEL’s OS upgrade introduces native support for newer cloud desktop protocols and zero-trust security features — a sign that software modernization remains a key battleground.

Lenovo’s refreshed thin client line with modern processors signals greater focus on edge-capable endpoints designed for hybrid processing models.

Regulation and sovereignty: EU data-governance requirements and similar national rules are pushing customers to adopt architectures that isolate or localize sensitive workloads. This is not purely a cloud vs. on-prem debate — it changes procurement screening, contractual SLAs, and vendor network architectures.

Zero-trust acceleration: CISA’s Zero Trust guidance has become an operational requirement for public-sector procurements and a strong preference for regulated industries. Endpoint management, attestation, and secure boot become evaluation priorities.

Energy and hosting economics: With data-center energy costs rising due to AI-driven demand, small differences in endpoint efficiency and centralized hosting models now translate into measurable TCO divergence.

Supply-chain and geopolitical risk: Export controls and component flow restrictions require procurement teams to stress-test vendor roadmaps and maintain alternative sourcing strategies for critical deployments.

Adopt a phased migration approach: Use quick-win DaaS pilots to validate user experience and cost assumptions, then scale into mission-critical tiers with hardened security controls.

Prioritize endpoint manageability: Select vendors providing robust lifecycle management, remote troubleshooting, and telemetry to minimize field interventions and reduce total operational cost.

Factor regulatory constraints into architecture: Map data flows and design regional service enclaves to comply with sovereignty requirements without fragmenting the overall desktop strategy.

Quantify energy exposure: Model hosting scenarios against a range of energy-cost assumptions and include sensitivity analyses in procurement negotiations.

Build supply-chain contingencies: Negotiate multi-supplier arrangements and include clauses for continuity of supply, forecasting, and component substitution where feasible.

Use vendor scorecards and scenario tests: Insist on live interoperability trials for critical workloads (real multimedia, GPU, or compliance-driven applications) before large-scale commits.

The report is intentionally built as a decision-support tool. We couple market-level projections (including the market’s current base size and our 4.98% CAGR outlook) with hands-on assets: procurement checklists, security control mappings, vendor RFP templates, and live-test scripts. For 2026 planning cycles, these deliverables shorten evaluation timelines, reduce procurement risk, and create a defensible evidence base for multi-year platform choices.

Concentration measures indicate that a small set of vendors captures a notable share of the market — a dynamic that favors those suppliers but also creates negotiating leverage for consolidated buyers. Our report provides negotiation playbooks that translate market concentration data into sourcing strategies, including pooling demand, staged rollouts, and enterprise licensing models designed to secure preferential pricing and service-level guarantees.

This briefing is designed as a strategic preview: it surfaces the essential market signals, competitive posture, and practical imperatives that should shape 2026 desktop-cloud decisions. The full PW Consulting report contains the granular segmentation, vendor scorecards, downloadable TCO models, and scenario workbooks necessary to operationalize these recommendations. For procurement teams, architecture leads, and security officers preparing FY26 budgets and deployment plans, the underlying datasets and playbooks will materially accelerate decision quality and reduce implementation risk.

Access the full report and companion toolkits on the PW Consulting website to obtain the complete vendor evaluations, downloadable templates, and our detailed regional and vertical segmentation analyses. If you would like a tailored briefing for your organization, schedule a consult with one of our sector specialists to map these insights to your specific operational, regulatory, and budgetary constraints.

For detailed analysis of this topic, please visit the official page:Desktop Cloud Terminal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com