Oil and Gas Storage and Transportation Market — Strategic Preview for 2026 Decision-Makers

As global energy markets enter a period of elevated volatility and structural transition, storage and transportation assets are being re‑rated as both critical resilience mechanisms and strategic leverage points for energy companies, governments, and institutional investors. PW Consulting’s new Oil and Gas Storage and Transportation Market report (base year 2025) synthesizes five years of historical performance (2020–2025) with a robust forecast through 2032 to deliver actionable guidance for leadership teams planning capital allocation, M&A, and operational transformation in 2026.

Oil And Gas Storage And Transportation Market

Market context at a glance

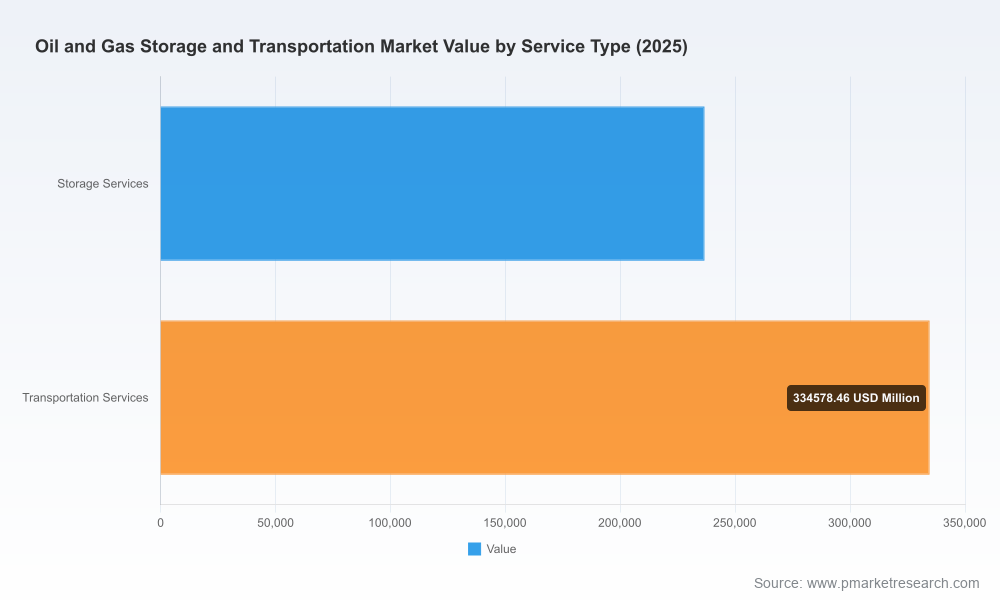

The sector achieved significant scale by 2025, with our market model estimating a global industry value in the range of hundreds of billions (USD Million basis) and a projected compound annual growth rate (CAGR) of 5.28% over the 2026–2032 forecast window. Under our baseline outlook, the market continues to expand steadily through 2032, reflecting sustained demand for logistics capacity, the monetization of new midstream projects, and strategic stockholding behaviours by both private and public actors.

Oil And Gas Storage And Transportation Market

Consolidation remains modest: the three‑player and five‑player concentration ratios sit below thresholds seen in many other infrastructure sectors, underlining a fragmented competitive landscape where both global terminal operators and regional midstream champions continue to find niche advantages.

Oil And Gas Storage And Transportation Market

Why this matters for 2026 strategic planning

- Capital allocation and project prioritization: With steady market expansion and selective pockets of acceleration (e.g., liquefaction-linked storage, strategic SPR exchanges, and petrochemical logistics), CFOs must reconcile medium‑term growth opportunities with near‑term cash preservation mandates. The report provides investment prioritization frameworks tailored to different corporate profiles — cash‑rich majors, asset‑light traders, and regional infrastructure owners.

- M&A and partnership playbooks: Fragmentation opens diverse entry points for scale, vertical integration, or capability enhancement. Our due diligence templates and valuation sensitivity matrices help identify targets whose upside is driven by operational synergies and contract re‑profiling rather than pure volume growth.

- Operational resilience and inventory strategy: Elevated observed oil stocks and episodic draws — including the IEA‑reported peak levels in early 2026 and monthly swings of tens of millions of barrels — mean storage strategy is now a dynamic portfolio decision. Operators who link real‑time market signals to flexible contracting and fast‑cycle berth management capture superior margin uplift.

- Regulatory and emissions risk management: With transportation sector energy use and emissions trajectories under pressure from tighter standards, asset owners must model regulatory scenarios into throughput planning and consider decarbonization capex (electrification of pumping, low‑carbon fuels, and CCUS readiness) as core to long‑term license to operate.

Key practical deliverables in the report

PW Consulting’s report is designed as an operational playbook as much as a market study. It contains:

- Scenario‑based financial models (base, upside, downside) with transparent assumptions for throughput, tariff curves, and utilization dynamics, delivered in spreadsheet form for client customization.

- Asset‑level risk heatmaps prioritizing geopolitical, regulatory, environmental, and technical exposure to inform divestiture or reinforcement decisions.

- M&A screening tools and synergy calculators calibrated to midstream and terminal economics to accelerate deal triage and integration planning.

- Contracting and commercial playbooks for storage leases, spot versus term allocations, and shipping/berth scheduling to optimize cash generation under volatility.

- Decarbonization pathways and repurposing options — including pipeline conversion for CO2 transport and integration of renewables for terminal electrification — with CAPEX/OPEX tradeoffs and IRR sensitivity tables.

- Short‑lead operational measures for 2026 (inventory choreography, force majeure contingency plans, labor and maintenance strategies) to protect margins during market stress.

Competitive landscape: what the incumbents are signaling

The market is shaped by a mix of global independent terminal operators, integrated midstream groups, national oil companies, and regionally dominant players. Leading firms include long‑standing tank storage specialists and pipeline giants headquartered across Europe, North America, the Middle East, and Asia. These incumbents are pursuing divergent strategies — portfolio optimization and disciplined brownfield expansion for some, aggressive new‑build programs and downstream integration for others.

- Global terminal operators are optimizing footprint and digitizing operations to raise utilization and reduce per‑barrel handling costs.

- Large midstream and pipeline players are leveraging scale to secure long‑dated contracts and to cross‑sell storage and logistics solutions to industrial customers.

- National oil companies are investing in integrated storage hubs as part of supply security and export expansion strategies.

Our competitive benchmarking evaluates corporate positioning across six dimensions — asset quality, contract mix, commercial agility, balance sheet flexibility, decarbonization readiness, and geopolitical exposure — to highlight where each firm can reasonably expect to win or defend value through 2026–2032.

Recent market developments and strategic implications

- Strategic stock movements and policy actions: In early 2026, government exchanges from strategic reserves and large tactical draws and replenishments have altered near‑term flows and created arbitrage opportunities for storage and shipping operators. Firms that can provide rapid physical handling and flexible contractual terms are capturing incremental margins.

- Large project awards and long‑term contracts: Ongoing large‑scale EPCI and project awards tied to major upstream and midstream programs continue to underpin demand for associated storage and pipeline capacity — a reminder that new upstream output often spurs parallel downstream and logistics investment needs.

- Infrastructure repurposing for low‑carbon solutions: National plans and industry programs point to growing opportunities to leverage existing pipeline and storage corridors for CO2 transport and sequestration, with public and private investment cases emerging around scalable multi‑user hubs targeting tens of millions of tonnes per annum in the next decade.

- Offshore and cross‑border pipelines: New offshore pipeline systems expected around 2026 shift basin connectivity and export profiles; owners of export terminals and nearby storage should reassess throughput forecasts and contractual exposure accordingly.

How executives should use this report in 2026

- Use the scenario financial models in capital allocation cycles to stress test development projects against a range of demand and regulatory outcomes.

- Prioritize shortlists for M&A based on our synergy calculators rather than headline capacity metrics; look for targets where commercial re‑profiling can unlock latent value.

- Deploy the contract playbook to renegotiate or re‑structure storage and shipping agreements, improving optionality and downside protection.

- Accelerate low‑cost decarbonization pilot projects at high‑impact terminals to de‑risk larger capex and to position assets for future carbon‑constrained markets.

- Leverage the asset‑level risk heatmaps when negotiating insurance, EPC guarantees, and community‑engagement programs to reduce time‑to‑operational readiness.

What we deliberately withhold here — and why

This market preview demonstrates the depth of PW Consulting’s analytical framework and the practical value embedded in our models. To preserve commercial integrity and maximize the utility of our decision support tools, we have intentionally not disclosed detailed segment allocations, regional share tables, or the granular financials behind our valuations in this public summary. Those elements — including terminal‑level throughput curves, counterparty exposure matrices, and full sensitivity runs — are available in the complete report and accompanying data pack on our website.

Bottom line for 2026

Storage and transportation will remain strategic assets across energy cycle management, supply security, and the energy transition. For leaders planning in 2026, the right questions are no longer only “where to build?” but “how to optimize existing footprints, monetize flexibility, and plan for a decarbonized throughput profile.” PW Consulting’s report supplies the market intelligence, commercial tools, and scenario models you need to make those decisions with clarity and confidence.

Next steps

- Download the full report and data pack to access our modeling templates, detailed competitive dashboards, and recommended action roadmaps.

- Book a 60‑minute strategy session with PW Consulting to review bespoke implications for your asset portfolio, and to prioritize a 12–24 month implementation plan.

For access to the full report and to schedule a briefing, please visit PW Consulting’s research portal. Our team stands ready to help translate the market outlook into defensible, executable strategy for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Oil And Gas Storage And Transportation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com