High Barrier MDO-PE Film Market — Strategic Insights for 2026 Decisions

Executive summary

PW Consulting’s new market research briefing on the High Barrier MDO-PE Film market delivers a forward-looking playbook for C-suite and commercial leaders preparing decisions in 2026. The market has shown a sustained acceleration from a modest base in the early 2020s to a robust mid‑2020s scale, and our base-year analysis (2025) positions the segment for continued rapid expansion through 2032 at a projected CAGR of 14.5%. This growth trajectory creates a narrow window in 2026 to secure supplier capacity, validate product roadmaps for mono‑material conversion, and align commercial models with evolving regulatory demand for recyclable, contact‑sensitive packaging.

High Barrier Mdo Pe Film Market

Market trajectory — what the headline numbers mean for strategy

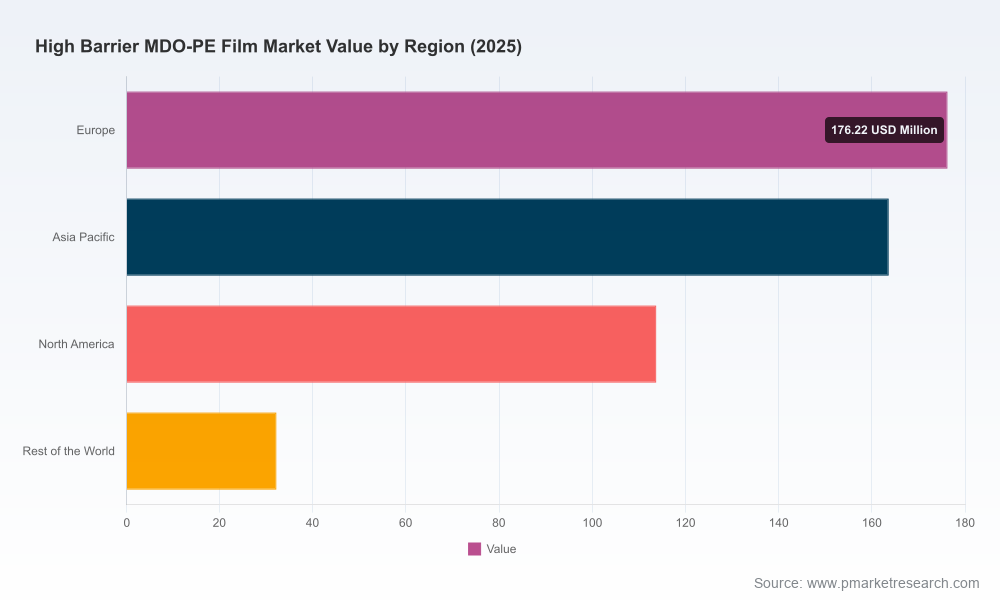

PW Consulting’s historical dataset (2020–2025) shows the market roughly doubling in size over five years as manufacturers, brand owners and converters accelerated development of oriented polyethylene (MDO‑PE) films with integrated or coated high‑barrier properties. The 2025 market level (our base year) provides the most recent benchmark for investment sizing and commercial prioritization. By the end of our forecast horizon (2032) the market is forecast to more than double again, reflecting broad adoption across food, personal care, pharmaceutical and selected industrial uses.

High Barrier Mdo Pe Film Market

For decision makers this implies three immediate imperatives for 2026: (1) convert product pipelines now to take advantage of capacity that will be constrained as adoption scales, (2) lock pricing and feedstock strategies to manage near‑term volatility, and (3) prioritize regulatory‑driven product features (recycled content and mono‑material recyclability) that will determine shelf space and procurement contracts after 2027.

High Barrier Mdo Pe Film Market

What’s included in the PW Consulting report — operationally focused deliverables

- Market model and scenarios: transparent base model with historical verification (2020–2025) and scenario outputs across 2026–2032 incorporating feedstock, adoption curves, and regulatory pathways.

- Financial playbooks: unit economics, margin sensitivity to polymer and coating input costs, and break‑even templates for thin‑gauge and downgauged film production.

- Commercial go‑to‑market frameworks: customer segmentation, value propositions for mono‑material conversion, channel strategies for brand engagement, and pricing tactics for early adopters vs. commodity buyers.

- Supplier and technology scorecards: comparative analysis of extrusion vs. coating technologies, barrier performance tiers, recyclability implications, and procurement checklists for risk mitigation.

- Regulatory & sustainability roadmaps: practical compliance checklists and product specifications to meet upcoming recycled‑content mandates and How2Recycle/collection requirements.

- Implementation assets: sourcing RFP templates, sample technical specifications for contract manufacturing, due‑diligence checklists for M&A or JV targets, and a prioritized list of commercial pilots to accelerate adoption.

- Interactive datasets and model workbook: the full report package includes downloadable models and scenario switches so teams can run bespoke sensitivity analyses—note that segmentation tables and unit‑level models are available in the full report package and intentionally excluded from this press release to preserve client value.

Competitive landscape — who’s shaping the market and how

The competitive map is evolving from a technology‑led, fragmented set of players toward an oligopolistic structure where scale, product breadth and sustainability credentials determine partner selection. Market concentration metrics indicate a market with several strong regional players and a rising cohort of global challengers; this creates both acquisition targets and strategic supplier choices for brand owners seeking regional redundancy.

- RKW Group (Mannheim, Germany) — Positioning a commercial catalogue around integrated EVOH solutions that enable mono‑material recyclable PE packaging. RKW’s Horizon® line is illustrative of the strategic trend: delivering comparable barrier performance to multi‑material laminates while simplifying recycling streams and reducing complexity for brand packaging conversions.

- Polifilm (Germany) — Focuses on product lines designed to substitute PET/OPP/OPA laminates and to act as high‑performance print substrates, marrying stiffness and optical quality with recyclability. Their portfolio is aligned to customers seeking direct OPP/PET replacement paths without sacrificing print and machinability.

- CloudFilm (Qingdao, China) — A supplier emphasizing AlOx‑coated and high‑barrier MDO‑PE grades for food, pet food and pharmaceutical laminates, targeting full‑PE recyclable structures for large packaged‑food customers in APAC and export markets.

- TOPESOL New Materials (Guangdong, China) — Competes on high‑barrier grades that approach foil‑equivalent aroma and oxygen protection, enabling single‑material PE concepts for aroma‑sensitive and long‑shelf‑life goods.

- Longdapac, Novel Packaging, Silvalac, ISOFlex Packaging — These players collectively enhance global capacity options with differentiated value propositions: cost‑competitive commodity grades, higher rigidity single‑material films, and conversion services from BOPP/PET to MDO‑PE laminates.

Two recent events underscore the pace of development: RKW’s product launch in mid‑2025 introduced integrated EVOH solutions with sustainability claims targeted at replacing multi‑material laminates, and a strategic partnership announced in late 2025 between a major polymer producer and a film equipment supplier advanced downgauged, unlaminated cast MDO‑PE film for deep‑freeze applications. These events indicate increasing cross‑industry collaboration and rapid commercialization of downgauged and unlaminated formats for specific end uses.

Strategic implications for 2026 planning

- Procurement & hedging — lock multi‑year feedstock contracts or flexible tolling arrangements now to mitigate the impact of feedstock price swings and regional polymer tightness observed in 2025.

- Product roadmaps — accelerate pilot conversions of high‑value SKUs (coffee, pet food, medical) where barrier parity with multi‑material laminates can command premium pricing and rapid retailer acceptance.

- Partnerships & M&A — prioritize bolt‑on acquisitions that close technology gaps (coating capabilities, EVOH handling) or add regional capacity where lead times could meaningfully delay market entry.

- Regulatory alignment — integrate recycled‑content targets into spec sheets, and plan for contact‑sensitive approval processes so commercial launches in 2027+ are not delayed.

- Portfolio optimization — for converters, maintain a dual‑track strategy of offering downgauged unlaminated MDO‑PE for low‑temperature and shorter shelf‑life SKUs while retaining laminate offerings for highest‑barrier needs, phasing migration as recycling streams mature.

Key risks & sensitivities to monitor

- Feedstock volatility — polymer pricing and availability swings materially affect unit economics; procurement strategy needs to be stress‑tested across multiple price regimes.

- Technology risk — coated vs. co‑extruded barrier strategies present different recycling implications and scale economics; choosing the wrong technical path can create stranded assets.

- Regulatory and standardization timing — evolving EU recycled‑content mandates and collection/labeling standards will continue to shape adoption. Early compliance confers commercial advantage, but standards may tighten or shift timelines.

- Supply concentration — moderate market concentration creates supplier leverage in specific geographies; securing alternate supply or tolling can prevent production disruptions.

How PW Consulting helps clients convert insight into action

Our advisory support for 2026 clients includes rapid deployment packages: a 6‑week commercial due‑diligence for potential acquisitions, a 12‑week supplier sourcing and hedging program, and a tailored product rollout plan (including pilot KPIs and converter selection). The full report package provides the data tables, regional & application split matrices, ranked supplier scorecards, and downloadable scenario models that underpin these advisory products. We intentionally withhold those granular subsegment tables in this press release to preserve the work product — access to the full dataset and model is available through our report landing page.

Call to action

If your 2026 strategic plan depends on timely, executable choices in high‑barrier MDO‑PE films — supplier selection, product transfer, pricing strategy, or M&A — the PW Consulting report and accompanying modeling toolkit are designed to make those decisions evidence‑based and actionable. For access to the complete report, detailed subsegment data, supplier rankings, and the interactive financial model, please visit our report page or contact our advisory team to schedule a briefing and scenario workshop.

For detailed analysis of this topic, please visit the official page:High Barrier Mdo Pe Film Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com